Distinct Strategies for 0DTE Options: A Complete Hour-by-Hour Guide

In the world of options trading, having a unique and effective approach to 0DTE options can make a significant impact. This comprehensive guide explores distinctive strategies for navigating the complexities of same-day options, focusing on detailed hour-by-hour execution.

This page has a deliberately narrow job inside our 0DTE cluster. 0DTE Options: The Complete Guide covers mechanics and beginner questions. 0DTE Theta Acceleration explains why decay goes exponential and sorts sellers into three archetypes. 0DTE Strategy Radar is a mechanical reversal-scalping system for directional intraday entries. Here you get the execution layer for premium sellers: the hour-by-hour decay table, the entry and exit clock, a full SPY cash-secured-put walkthrough, and how to size 0DTE inside a weekly income portfolio so one gap day cannot erase a month of theta.

The promise of 0DTE: capture 3-5 days' worth of theta decay in a single session. The risk: early assignment, gap moves, and liquidity crunches can hand those profits back just as fast — your position can swing 10% in minutes. If you are new to zero-days-to-expiration trading, start with the complete 0DTE guide first, then return here when you are ready to execute.

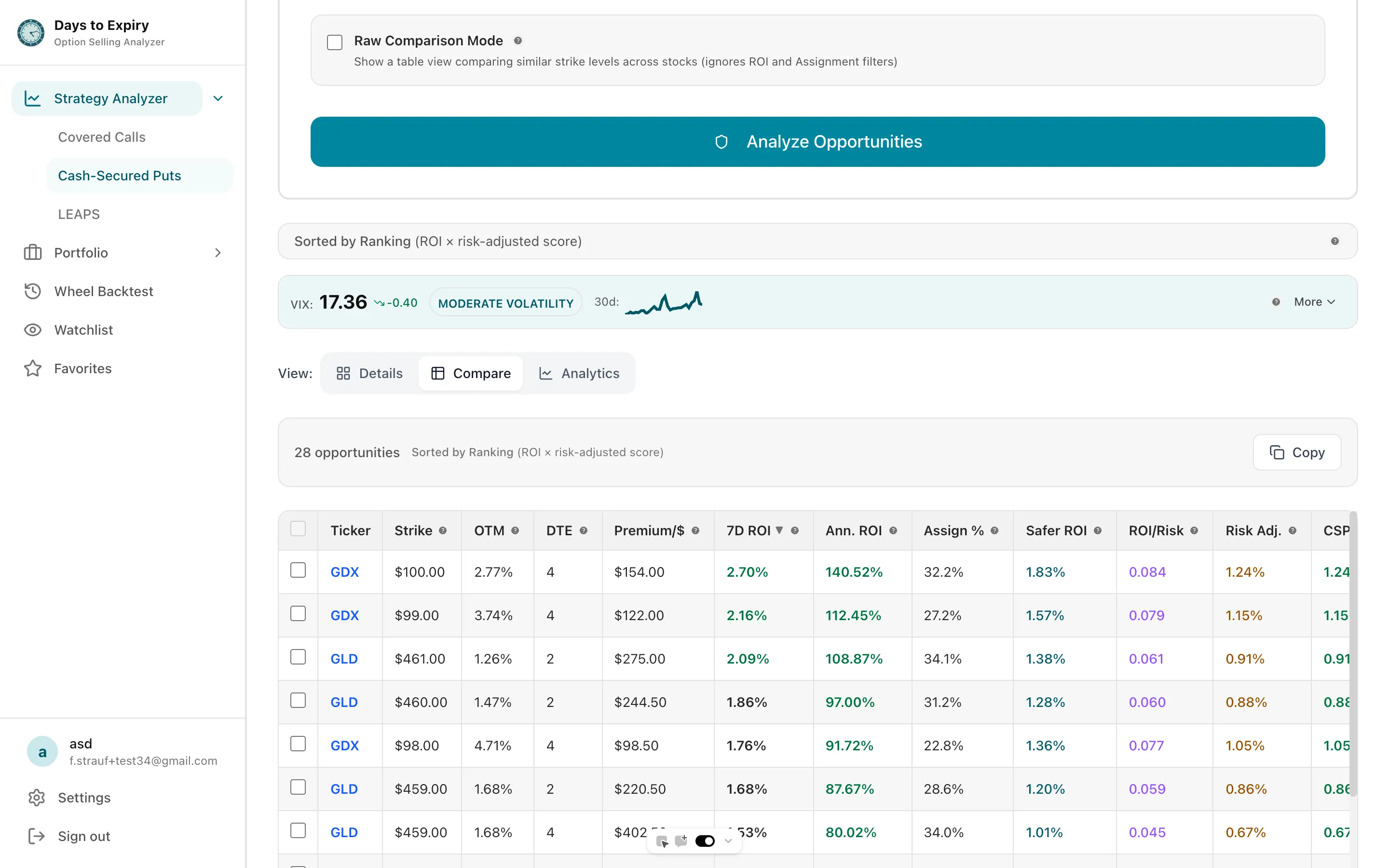

Compare premiums to find the best balance between yield and assignment risk

Compare premiums to find the best balance between yield and assignment risk

Prefer longer DTE? If 0DTE feels too aggressive, use our Strategy Analyzer to find cash-secured puts and covered calls with 7-45 DTE—capturing theta decay at a more manageable pace.

The 0DTE Theta Decay Curve, Hour by Hour

Theta decay over an option's full life is exponential — a 45 DTE put might lose $0.02 per day, a 7 DTE put $0.08-0.12, a 1 DTE put $0.40-0.60. The theta acceleration guide covers that DTE-level math in depth. What matters for execution is the intraday curve: how expiration day itself decays hour by hour.

Typical intraday decay curve: ATM SPY option worth $0.60 at the open

| Time (ET) | Hours left | Option value | Decay in prior hour | Decay rate |

|---|---|---|---|---|

| 9:30 AM | 6.5 | $0.60 | — | — |

| 10:30 AM | 5.5 | $0.48 | $0.12 | ~20%/hr |

| 11:30 AM | 4.5 | $0.38 | $0.10 | ~21%/hr |

| 12:30 PM | 3.5 | $0.30 | $0.08 | ~21%/hr |

| 1:30 PM | 2.5 | $0.23 | $0.07 | ~23%/hr |

| 2:30 PM | 1.5 | $0.15 | $0.08 | ~35%/hr |

| 3:30 PM | 0.5 | $0.05 | $0.10 | ~67%/hr |

| 4:00 PM | 0 | $0.00 | $0.05 | ~100%/hr |

Three execution-relevant facts fall out of this curve:

- The opening hour delivers the fastest dollar decay on slightly OTM strikes because overnight IV deflates right after the bell — this is why the 9:35-10:00 AM entry window exists.

- The 11 AM-2 PM stretch is the highest-quality harvesting window: decay is steady, gamma is manageable, and liquidity is at its best.

- After 2 PM the curve goes vertical — decay per hour roughly doubles, but so does gamma. Selling into the final two hours is the Hawk's game from the theta acceleration playbook, not an income seller's.

Here's the same curve on a real strike. Say you sell a cash-secured put on SPY at a $420 strike with 1 day to expiration:

- At market open (6.5 hours of trading left): The option is worth $0.30

- At 12:00 PM: The option is worth $0.15

- At 2:30 PM (90 minutes to close): The option is worth $0.05

- At 3:59 PM: The option is worth $0.01

That's $0.29 in profit captured in a single day. The decay isn't faster per se; it's that all remaining time value is concentrated in those final hours.

The 0DTE edge: You're not betting on directional movement. You're betting on time value disappearing faster than implied volatility increases.

The 0DTE Trading Window: When Opportunities Emerge

Timing is everything in 0DTE trading. The same strike can yield wildly different outcomes depending on whether you enter at 9:35 AM or 2:00 PM. The key is matching your entry window to the current volatility regime and your personal risk tolerance.

0DTE traders don't wait for expiration week. They trade on expiration day itself.

The optimal 0DTE window opens when:

- Market has been relatively stable (low realized volatility) → IV doesn't spike → theta decay is pure profit

- Implied volatility is higher than recent realized volatility → You're getting paid for volatility that may not materialize → perfect for premium selling

- The underlying is 1-2% away from your strike → Assignment probability is manageable, but premium is still juicy

- You have time to monitor the position → 0DTE requires active management, not set-and-forget

Typical 0DTE opportunities:

- 9:35-10:00 AM ET: First 30 minutes post-open. IV is highest because traders are repricing overnight gaps and news. Sell here, close 2-3 hours later.

- 2:00-3:30 PM ET: Mid-afternoon window. Morning volatility has settled, but enough time remains for theta to matter. Close 45 minutes before market close.

- NOT 3:50-4:00 PM: Too late. Illiquidity spikes, bid-ask spreads widen, and a $0.01 position becomes hard to close cleanly.

The 0DTE Risk Matrix: Assignment and Gap Risk

0DTE strategies generate rapid income, but they also concentrate risk into a few hours. Understanding assignment probability, gap risk, and liquidity dynamics before you trade is non-negotiable. Experienced traders treat risk management as the primary strategy and premium collection as the secondary outcome.

Here's where 0DTE gets dangerous.

Early Assignment Risk on 0DTE

By definition, 0DTE options are deep in-the-money (ITM) or right at-the-money (ATM). That means assignment probability is high.

If you sell a 0DTE cash-secured put and the underlying drops through your strike at 2:00 PM:

Scenario 1: Dividend payment today

- Your put gets assigned immediately (brokers assign ITM options before ex-dividend cutoff)

- You own 100 shares of a stock you didn't expect to own until tomorrow

- You must immediately sell covered calls or exit the position

Scenario 2: No dividend, but deep ITM

- Assignment probability is 80%+ by afternoon

- You can close the position before assignment, but liquidity might be thin

- Bid-ask spread might be $0.01 or more (on a $0.05 position, that's 20% of your profit)

The fix: Accept that 0DTE positions have 50-70% assignment probability. Plan for ownership.

Gap Risk: The Overnight Killer

0DTE is a daytime strategy. But markets don't respect the 4 PM close.

If you sell a cash-secured put at 3:45 PM (closing time):

- Market is open for 15 minutes

- News hits after close: Fed announcement, earnings miss, geopolitical event

- Tomorrow: gap down 2-3%

- Your $420 put is now worth $2.00 instead of $0.05

- Your $0.30 profit just became a $1.70 loss

The fix: Never hold 0DTE positions overnight, even if you think you'll close them at open. Gaps happen. If you want to trade overnight theta decay, move to 1-2 DTE positions in pre-open 0DTE (yes, this exists; you can trade tomorrow's 0DTE today).

Liquidity Risk: Bid-Ask Spread Explosion

0DTE positions are dramatically less liquid than 1-7 DTE, and the spread widens as a percentage of the position size as the close approaches. A SPY $420 put that trades $0.22/$0.24 at 1 DTE might sit at $0.02/$0.05 with two hours left on expiration day — a $0.03 spread on a $0.05 position. Sell a $0.20 premium into that and friction alone can eat 20-30% of your theoretical theta profit. The theta acceleration guide publishes a full hour-by-hour bid-ask widening table; the practical rules for this playbook are simple:

- Plan to close at the bid (don't try to time the ask)

- Budget 20-30% of theoretical theta profits as friction loss

- Use limit orders only; never market orders on 0DTE

0DTE Position Sizing: The Conservative Framework

Position sizing separates surviving traders from blown-up accounts. Because 0DTE can swing 20-30% in minutes, allocating too much capital to a single expiration-day trade is the most common cause of permanent account damage. The conservative framework below is designed to keep you in the game long enough to compound edge.

Because 0DTE has higher assignment and gap risk, position sizing matters more than in 1-7 DTE trading.

Rule: 0DTE positions should represent no more than 20-30% of your weekly theta target.

Here's why:

Say you typically earn $500/week from 1-7 DTE covered calls and cash-secured puts. A bad 0DTE day (gap at open, liquidity crash, unexpected assignment) can wipe $300-500. That's 1-2 weeks of income gone.

Conservative 0DTE sizing:

- Use 50-75% of your normal cash-secured put capital

- Only trade the highest-liquidity underlyings (SPY, QQQ, IWM, individual mega-caps)

- Set a hard stop loss: If assignment happens and your underlying moves 2% against you, close it immediately

Aggressive 0DTE sizing:

- Use 100% of capital on high-confidence setups

- Trade more obscure underlyings (more premium, less liquidity)

- Accept that 10-20% of 0DTE plays end in assignment + forced exit

The 0DTE Setup: Entry and Timing

Best Markets for 0DTE

Not all market conditions favor 0DTE strategies. Here's when to be aggressive vs. defensive:

Aggressive 0DTE (sell more premium):

- IV percentile > 70% (implied vol is elevated relative to historical vol)

- Realized volatility (last 5-10 days) is lower than implied vol → market is pricing in risk that won't materialize

- Market is directionless → no strong trend, just ranging

- 30-60 minutes post-market open → maximum IV, less time-value decay pricing

Defensive 0DTE (reduce size, tighten strikes):

- IV percentile < 20% (vol is cheap; won't decay much)

- Earnings announced today or tomorrow → binary risk

- Fed announcement, jobs report, or geopolitical risk → unpredictable gap risk

- Market is trending hard (up or down) → assignment probability is extreme

The 0DTE Selling Framework

Step 1: Pick your underlying

- Highest daily volume (SPY, QQQ, IWM, or mega-cap stocks: AAPL, MSFT, TSLA)

- At least 1,000+ contracts on your strike (ensures exit liquidity)

Step 2: Select your strike

- Cash-secured puts: Sell 0.30-0.50 delta (these are closer to ATM, higher premium, higher assignment risk)

- Covered calls: Sell 0.20-0.40 delta (lower assignment risk, but less premium)

- Spreads: Sell spreads 1-2% OTM, use wider widths than usual (e.g., $5 wide vs $2 wide for 1 DTE)

Step 3: Set your entry trigger

- Enter 30-45 minutes after market open (IV is highest post-open, theta decay is starting)

- Wait for a 0.5-1% pullback if you're selling puts (better entry premium)

- Place limit orders, don't market order (you'll overpay for entry)

Step 4: Set your exit trigger

- Exit when: Position reaches 50% max profit OR 1.5 hours before close (whichever comes first)

- Use mental stop loss: -20% of capital on the trade

- Close all 0DTE positions by 3:00 PM ET (avoid final hour chaos)

Real Example: 0DTE SPY Cash-Secured Put

Setup:

- Date: November 3, 2025 (expiration day)

- SPY is trading at $423.50

- Sell the $423 put

Timeline:

| Time | SPY Price | $423 Put Price | Your P&L | Action |

|---|---|---|---|---|

| 9:40 AM | $423.20 | $0.45 | -$0.45 | Sell (limit order at $0.45) |

| 10:15 AM | $423.10 | $0.32 | +$0.13 | Monitoring |

| 11:00 AM | $424.00 | $0.18 | +$0.27 | Still holding |

| 12:30 PM | $423.80 | $0.08 | +$0.37 | Getting close to max profit |

| 1:15 PM | $424.20 | $0.03 | +$0.42 | Exit at bid ($0.02-0.03 spread) |

| Result: | +$0.42 profit on $0.45 premium | 93% max profit captured |

What just happened:

- You captured $0.42 in decay in ~4 hours

- You avoided the final 3 hours (which might have seen a news event, gap risk, assignment)

- You closed early at 93% max profit, forgoing the last $0.03 to eliminate overnight risk

- You freed up capital to run another 0DTE in the same day if the setup improves

Combining 0DTE with Your Weekly Income Strategy

0DTE shouldn't replace your primary income strategy—it should supplement it.

Here's how to integrate 0DTE into a balanced portfolio:

Scenario 1: Mostly Weekly CSPs + Monthly CCs + 0DTE

Your baseline strategy:

- Monday-Friday: Sell 7-DTE cash-secured puts, close at 50% profit (2-3 business days later)

- Monday-Friday: Sell 30-DTE covered calls on held stock, roll at 50% profit

- 2-3x per week: Sell 0DTE CSPs on high-IV days (supplement income on quiet days)

Capital allocation:

- 60% to 1-7 DTE positions (consistent, predictable income)

- 20% to 30+ DTE positions (wheel strategy, long-term income)

- 20% to 0DTE positions (high-frequency theta capture)

Why this works:

- 1-7 DTE positions generate $500-750/week (stable)

- 0DTE positions add $100-200/week (opportunistic boosts)

- Monthly CCs generate $300-500/month (passive income during hold)

- Total: $2,000-2,500/month on $50k capital

Scenario 2: Aggressive 0DTE Scalping

Your baseline strategy:

- 80% of capital in 0DTE CSPs/CCs, traded 2-4x per day on high-volume days

- 20% reserved for 1-7 DTE positions as a hedge

Entry/Exit:

- Morning 0DTE (9:35-11:30 AM): Sell CSPs, close at 50-75% profit

- Afternoon 0DTE (1:00-2:30 PM): Sell CSPs/CCs, close at 50-75% profit

- Late afternoon: Don't hold anything

Capital needs: This requires $10-20k minimum (to absorb 1-2 bad days) and active monitoring.

Realistic returns: $50-100/day on $50k capital = $1,000-2,000/month if you execute 250 trading days/year. But requires 4-6 hours of active trading daily.

Risk Management: The 0DTE Adjustment Playbook

Even with perfect entry/exit timing, 0DTE positions can blow up. Here's your playbook for damage control.

Adjustment 1: The Early Assignment Trap

Scenario: You sell a 0DTE cash-secured put, it gets assigned at 1:00 PM. You now own 100 shares.

Your options:

- Immediately sell covered calls (same strike or higher) to lock in profit and create a wheel cycle

- Exit the position by selling the shares (cap your loss/profit)

- Hold and manage it as a position (only if you wanted to own the stock anyway)

The math:

- Sell $420 put for $0.50 (get assigned) → own 100 shares at effective cost of $419.50

- SPY drops to $418 in the last hour

- Your shares are down $150

- Sell $420 call for $0.15 → lock in net $0.35 profit despite the price drop

Adjustment 2: The Gap-at-Open Hedge

Scenario: You sell a 0DTE put for $0.40 at 3:45 PM. Overnight, gap down 2%. Tomorrow's 0 DTE put is worth $2.50.

Prevention (not adjustment, but critical):

- Never sell 0DTE positions in the final 10 minutes of trading

- Avoid selling 0DTE before earnings, Fed announcements, or major economic data

- Place hard stops: If your position is down 30% by 3:00 PM, just close it

Adjustment (if you get caught):

- At market open, immediately sell a call spread to hedge downside (e.g., sell $418 call, buy $416 call)

- This caps your loss while you close the put position

- Your net might be -$0.50 instead of -$2.10

Adjustment 3: The Liquidity Crunch

Scenario: It's 3:55 PM, your 0DTE position is worth $0.02, and the bid-ask spread is $0.01-$0.04. You can't exit cleanly.

Your moves:

- Place an aggressive limit order (at the bid, not midpoint) and cancel it at 3:59:45 PM if unfilled

- Use spreads to exit (buy back at ask price in a spread format, sell a call at higher strike to offset)

- Let it expire (only if you're ok with assignment; if it's a put and you have cash, assignment is fine)

Lesson: Don't get here. Close positions by 3:00 PM ET on 0DTE days.

0DTE on Different Underlyings: Strategy Variations

Not all underlyings behave the same on expiration day. Index options like SPY and QQQ offer liquidity and tighter spreads, while individual stocks provide higher premiums at the cost of gap risk. Choosing the right underlying for your 0DTE strategy is as important as choosing the right strike.

0DTE on SPY/QQQ (Easiest)

- Highest liquidity

- Widest bid-ask spreads are still reasonable ($0.01-0.02)

- Highest IV, most consistent premium

- Best for: Beginners learning 0DTE

- Position size: Start with 1-2 contracts

0DTE on Individual Stocks (Higher Risk, Higher Reward)

AAPL, MSFT, TSLA:

- Premium is 2-3x higher than SPY on same delta

- Liquidity is decent, but bid-ask spreads widen more on 0DTE

- Single stock gaps are more frequent than index gaps

- Best for: Experienced traders with tight risk management

- Position size: 1 contract only; use spreads instead of naked positions

0DTE on Earnings Dates (Avoid)

- IV is artificially inflated (priced for binary move)

- Realized volatility will spike or drop based on earnings result

- Not suitable for pure theta decay plays (you're really trading direction)

- Only consider if: You have a directional thesis (put spreads on stocks you think will beat)

0DTE on Quiet / Low-Volatility Days (Best Risk/Reward)

- IV is low relative to normal (less premium upfront)

- But realized vol is also low (less likely to gap against you)

- This is your sweet spot: theta decay > directional moves

- Action: Sell 0DTE on Mondays-Wednesdays when markets are calm

Combining 0DTE with the Wheel Strategy

If you run a wheel strategy (CSP → assignment → covered call → repeat), 0DTE fits perfectly as a supplement.

Weekly wheel cycle:

- Monday: Sell 7-DTE CSP, target 50% profit in 3-5 days

- Thursday-Friday: If CSP is closed at profit, sell new 7-DTE CSP OR jump to 0DTE if IV spikes

- Friday: Sell 30-DTE covered call on assigned stock

- Daily: On quiet/high-IV days, sell 1-2 0DTE CSPs for quick income bursts

The math:

- CSP + CC per week: $150-250

- 0DTE boosts (2-3 per week): $50-100

- Total: $200-350 per week = $10,400-18,200 per year on $50k capital

This is how Days to Expiry platform helps: track your 0DTE entry/exit points, monitor assignment probability in real-time, and measure 0DTE vs. traditional theta income side-by-side.

0DTE Mistakes to Avoid

Even experienced traders make costly errors on expiration day — the compressed timeline leaves little room for recovery. The theta acceleration guide and the strategy radar playbook each cover generic 0DTE traps in depth; these four are the ones that specifically destroy income sellers running the playbook above:

- Over-sizing because "it decays so fast." One bad gap wipes out a week of 0DTE profits. Cap 0DTE at 20-30% of your weekly income target, per the sizing framework above.

- Fighting assignment instead of planning for it. 0DTE CSPs carry 50-70% assignment probability. Trying to close mid-day to dodge assignment burns profits to slippage. Decide your assignment response before entry: roll into a covered call, wheel the shares, or exit.

- Selling into low IV just to stay busy. Premium is thin, gaps are unpredictable, and theta barely outruns friction. Only sell 0DTE when IV percentile is above 50%.

- Letting winners ride past 3:00 PM. The final hour inverts the risk/reward — liquidity crashes and gamma takes over. Exit by 3:00 PM ET as a hard rule, even when the position "only has $0.03 left."

0DTE Platform Tools: What to Look For

If you're using Days to Expiry or similar platforms to track 0DTE:

Essential features:

- Real-time theta visualization: See decay curve for 0DTE positions

- Assignment probability tracking: Know your odds minute-by-minute

- IV percentile alerts: Get notified when IV crosses thresholds (sell above 60%, buy below 40%)

- Position P&L by date: Measure 0DTE income separately from 1-30 DTE income

- Liquidity analysis: See bid-ask spreads and expected slippage before entry

Premium features:

- 0DTE scanner: Automatically find high-IV, high-liquidity 0DTE opportunities

- Expiration calendar: Visual tracking of which underlyings expire each day

- Gap risk alerts: Notifications for upcoming earnings, economic data, news events

The Bottom Line: Is 0DTE Right for You?

0DTE is not a strategy you graduate into after reading one article. It is a high-frequency, high-stakes income tool that demands active monitoring, strict risk rules, and emotional discipline. Before committing capital, honestly assess your availability, experience level, and ability to follow predetermined exit rules without hesitation.

0DTE is not for everyone. It's a tactical income booster, not a primary income strategy.

0DTE is right if you:

- Have 2-4 hours of daily availability to monitor positions

- Can stomach 20-30% daily swings on your 0DTE capital

- Already run a successful 1-7 DTE or wheel strategy (0DTE should supplement, not replace)

- Accept that gaps and assignments are part of the game

- Have at least $10k capital (to absorb bad days)

0DTE is NOT right if you:

- Can't actively monitor positions during the trading day

- Need predictable daily income (0DTE is feast-or-famine)

- Are still learning options basics (master 1-7 DTE first)

- Can't emotionally handle rapid theta decay suddenly reversing

My recommendation: Start with 1-2 small 0DTE trades per week once you've mastered 1-7 DTE strategies. Measure the profits (and losses). See if the effort (2 hours of active trading) is worth the extra $50-100/week. For most traders, 1-7 DTE is enough. For active traders seeking maximum income, 0DTE is a powerful supplement.

The edge is real—but the risk is real too. Respect both.

For traders ready to expand beyond same-day expiration, our 21 DTE Rule guide explains why closing positions early often outperforms holding to expiration. And if you want to compare index versus equity 0DTE approaches, the SPY vs SPX comparison provides a decision framework for choosing the right underlying.

Related Articles

Learn more about the strategies that combine with 0DTE:

- Options Greeks Delta Theta Definition

- 0DTE Theta Acceleration

- Theta Decay Accelerates Near Expiration

- 0DTE Options: The Complete Guide – The foundational overview of zero-days-to-expiration mechanics, risks, and beginner considerations

- 0DTE Strategy Radar: High-Probability Intraday Playbook – Advanced 0DTE scalping tactics for active traders

- 0DTE Theta Acceleration: Maximizing Decay on Expiration Day – How theta decay behaves in the final hours before expiration

- Cash-Secured Puts Playbook: DTE Optimization & Assignment Risk – Understand assignment probability frameworks that apply to 0DTE

- Implied Volatility & Days to Expiry: Timing Your Options Entries – IV optimization for 0DTE entries

- Options Greeks Explained: Income Trader's Guide – How delta and theta accelerate at 0DTE

- Theta Decay in Options: DTE Curves & Time Value Optimization – Deep dive into the math behind 0DTE decay

- Pin Risk in Options: Managing Expiration Uncertainty by DTE Phase – Why pin risk spikes in the final hour and how to avoid it

- SPY vs SPX Options: Complete Comparison with Decision Framework – Choose the right underlying for your 0DTE trades

- Gamma Risk Near Expiration: What Every Options Seller Must Know – How gamma explodes on expiration day and how to size around it

- The 21 DTE Rule: When and Why to Close Options Positions Early – The broader DTE management philosophy that also applies to 0DTE exits

- What Is 0DTE Options? A Plain-English Explanation

- What Are 0DTE Options? The Concise Answer for New Traders

- VXX ETF Explained: How the Volatility ETN Works and Why Traders Use It

- Short VIX ETF: How Inverse Volatility Products Work and How Traders Use Them

- Option Omega Review 2026: Backtest, Model & Automate Options Strategies

- Free Trading Journal: Best Tools, Templates & Setup Guide

- SPX Options Tax Treatment: The 60/40 Rule Explained

- Iron Condor Strategy: Neutral Income with DTE Optimization

Frequently Asked Questions

Written by Days to Expiry Trading Team

The Days to Expiry trading team brings together experienced options traders and financial analysts dedicated to helping investors generate consistent income through proven options strategies.

Continue Your Journey

Covered Call Analyzer

Find the best covered call opportunities.

Cash-Secured Put Calculator

Calculate put selling returns.

Demo Portfolio

Explore a sample portfolio with positions and strategy insights — no login required.

Wheel Strategy Calculator

Plan your wheel trades.

Free trial

Start free — then keep the full workflow

- Multi‑stock covered call and cash‑secured put scans

- Strategy backtesting for covered calls and puts

- Full wheel backtesting with buy‑and‑hold comparison

- AI Portfolio Scanner for advanced recommendations