Understand Delta, Gamma, Theta & Vega Instantly

Confused by options Greeks? Don't understand what delta, gamma, theta, and vega actually mean? Our calculator shows you exactly how each Greek impacts your trade—instantly, for any stock price, any expiration date.

Tap to view full size

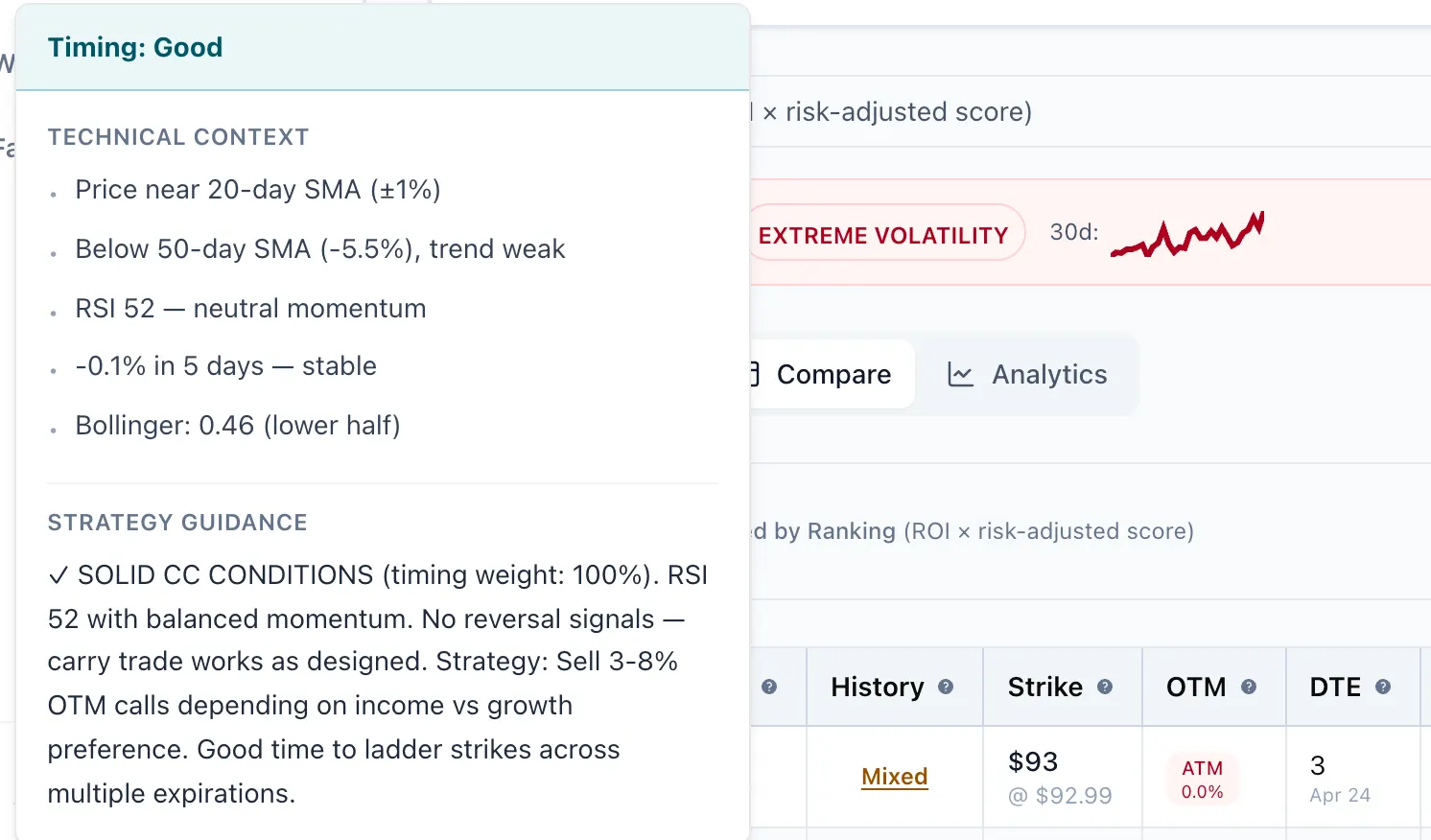

Four Different Greeks, Four Different Impacts — Hard to track mentally

Greeks Are Constantly Changing — What matters today changes tomorrow

Multi-Leg Positions Are Impossible to Calculate Manually — Spreads multiply complexity

You Can't See Scenarios Without Real-Time Calculation — What if stock moves 10%? What if IV spikes?

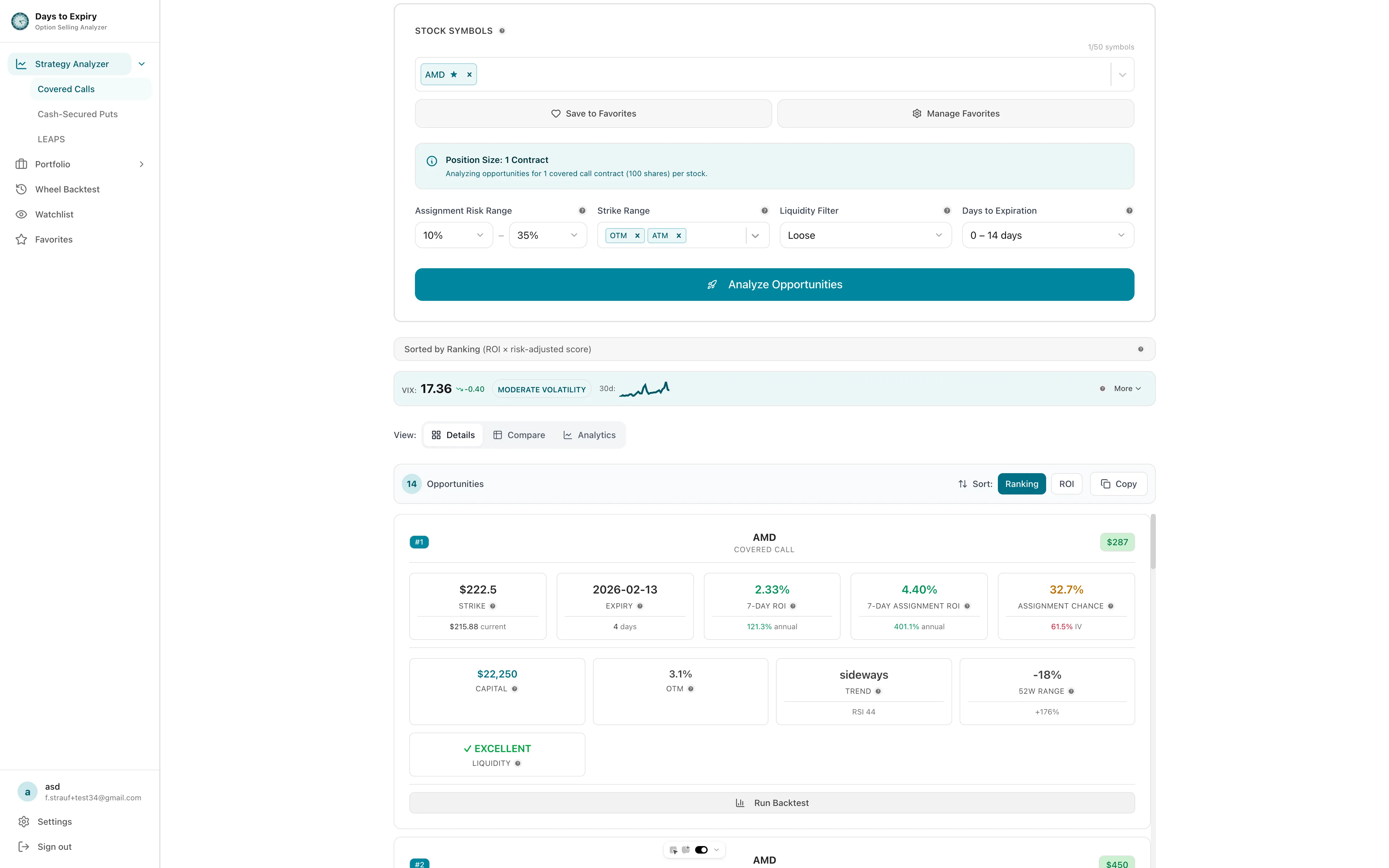

Delta, gamma, theta, vega all calculated

See Greeks at different stock prices

Calculate Greeks for spreads, straddles, etc.

Charts showing delta/gamma/theta/vega impact

What do these numbers actually mean?

Current P&L and breakeven at expiration

Tap to view full size

Deep dive into options Greeks with our comprehensive guides. Learn how delta, gamma, theta, and vega work together to affect your trades.

Beginner-friendly explanation of options Greeks

How Greeks behave at different days to expiration

Practical applications of vanna in options trading

Critical gamma risks every options seller must understand

Understanding theta decay in zero-days-to-expiration trades

When and why to close options positions early

Stock ticker, strike price, expiration date, call or put

Delta, gamma, theta, vega all calculated with real market data

Ask "what if" questions: stock moves to $250? IV spikes 10%? 1 week passes?

Decision: Bullish on AAPL , time decay manageable , IV potential to Buy the call

Delta

0.55

Gamma

0.04

Theta

-$0.08/day

Vega

+$0.18 per 1% IV

Beginner-friendly explanation of options Greeks

How Greeks behave at different days to expiration

Practical applications of vanna in options trading

Critical gamma risks every options seller must understand

Understanding theta decay in zero-days-to-expiration trades

When and why to close options positions early

Everything you need to know about getting started