Can Cash Secured Puts Be Assigned Early? How to Roll

Can cash secured puts be assigned early? Yes—American-style options can be exercised at any time before expiration, especially when deep in-the-money near ex-dividend dates. Early assignment forces share purchase at the strike price. Rolling lets you close the current put and sell a new one later, but only when the credit covers costs and your thesis still holds.

But what happens as expiration approaches and you're facing a rolling decision?

This guide shows you exactly how to roll cash-secured puts at every DTE stage—and when rolling makes sense versus accepting assignment. For the foundational CSP strategy (strike selection, DTE optimization, capital management), start with our complete CSP playbook.

Assignment Stress Test

Test your position under adverse market scenarios to understand assignment risk and potential losses.

Base Assignment Probability

30%

Premium Collected

$250

Maximum Loss

$43,750

Scenario Analysis

| Price Move | Final Price | Assignment Prob | P/L | Status |

|---|---|---|---|---|

| Current | $450.00 | 15% | $250 | Safe |

| -5% | $427.50 | 32.9% | $-1,000 | At Risk |

| -10% | $405.00 | 38.6% | $-3,250 | At Risk |

| -20% | $360.00 | 52.2% | $-7,750 | At Risk |

Break-even: $437.50 • Blue row shows current price scenario

Find real options with similar parameters

Find your next roll target and track adjustments: Use our Strategy Analyzer to compare CSP premiums across different strikes and expirations. Once you roll, track your adjusted positions using the portfolio tracking methodology that works for covered calls—same principles apply. For stock selection and initial strike entry, see best stocks for selling cash-secured puts.

Rolling Fundamentals: What You Need to Know

What is a CSP Roll?

A CSP roll closes your current short put and opens a new short put at a later expiration date.

The Mechanics:

Original Position:

Sold 1 XYZ $50 put 30 DTE, collected $2.00 premium

At 14 DTE, you decide to roll:

Step 1: Buy to close $50 put @ current bid ($2.30)

Cost: -$230

Step 2: Sell to open new $48 put at 30 DTE for $1.80

Credit: +$180

Net: -$50 debit to extend position

New Position:

Short $48 put, 30 days to expiration

Original $2.00 + New $1.80 = $3.80 total collected

Extended expiration by ~30 days

Why Roll a CSP?

| Reason | Situation | Outcome |

|---|---|---|

| Collect more premium | Stock hasn't moved much; you want income extension | Extend position, compound premiums |

| Avoid assignment | Stock approaching strike; you want to defer assignment | Extend 30+ more days, keep waiting |

| Adjust for price movement | Stock fell; you want new strike below | Roll down to lower strike |

| Reset for income | Stock is stable; you want next month's premium | Roll to next monthly expiration |

When NOT to Roll

| Situation | Reason | Better Action |

|---|---|---|

| Stock is way below strike | Rolling down is expensive (you're chasing losses) | Accept assignment or close |

| You've already rolled 3+ times | You're just delaying the inevitable | Accept assignment or take loss |

| You're down 75%+ of max loss | Rolling costs aren't worth remaining premium | Close and move on |

| Fundamentals have deteriorated | Company news is negative; expect further declines | Don't extend; accept assignment |

| You're happy with assignment | Stock has moved to your target (below strike) | Let it expire; take assignment |

DTE-Specific Rolling Strategies

Phase 1: 45-30 DTE (Early Management Window)

What's Happening:

- Your position is typically profitable or at break-even

- Theta decay is moderate (stock needs to move significantly to breach)

Roll decision analyzer tool showing assignment probability and timing across DTE stages

Roll decision analyzer tool showing assignment probability and timing across DTE stages

- Rolling costs are reasonable (both sides still have time value)

- You have flexibility to plan

Rolling Decision:

Scenario 1: Stock well above your strike (up 10%+ since entry)

Original: Sold $50 put, received $2.00, stock was $52

Now: Stock at $57, 40 DTE remaining

Put is worth $0.60 (decayed significantly)

Decision: Don't roll

Why? Stock is clearly not going to your strike

Action: Let it expire worthless

Result: Keep full $2.00 premium, no cost

Alternative: Sell new CSP on different stock

Use freed capital to start new position

Compound your income stream

Scenario 2: Stock is near your strike (±2%)

Original: Sold $50 put, received $2.00, stock was $52

Now: Stock at $51, 40 DTE remaining

Put is worth $1.50 (in the money, but DTE helps)

Decision: Consider rolling down

Roll down (sell $48 put):

Buy to close $50 put @ $1.50 = -$150

Sell new $48 put for $1.10 = +$110

Net debit: -$40 (extends, but costs money)

Alternative: Do nothing and let it ride

Stock might recover over next 40 days

If assigned, you buy at $50 (acceptable price)

Recommendation: Only roll if stock momentum is negative

Otherwise, let it play out

Scenario 3: Stock is well below strike (down 10%+)

Original: Sold $50 put, received $2.00, stock was $52

Now: Stock at $47, 40 DTE remaining

Put is worth $3.50 (deep ITM)

Decision: Accept assignment likely, but don't roll

Why? Rolling down to $45 would cost:

Buy $50 put @ $3.50 = -$350

Sell $45 put @ $2.00 = +$200

Net debit: -$150 (huge cost!)

Better options:

A) Accept assignment at $50 (you get stock at discount)

B) Close position now (buy $50 put @ $3.50, take loss)

C) Wait 30 more days (see if stock recovers)

Recommendation: Option A usually best

You get stock at $50 (discount to original $52)

You collected $2.00 premium upfront

Cost basis: $48/share ($50 - $2 premium)

Best Practice at 45-30 DTE:

- Only roll if stock is within 1% of your strike

- Roll up if you want higher profit target (rare)

- Roll down only if stock momentum is strongly negative

- In most cases, let it play out

Phase 2: 30-21 DTE (Decision Window Opens)

What's Happening:

- Theta is accelerating (1.5-2% daily decay)

- Your current put is eroding in value

- New puts 30-45 DTE have richest premiums

- Assignment is becoming likely if ITM

Rolling Decision Tree:

Is your put ITM (stock below strike)?

YES (Stock below strike):

├─ Assignment is likely

├─ Decision: Roll down or accept?

│

├─ Roll down IF:

│ - Stock momentum is negative but you still like it

│ - You want to defer buying for 30 more days

│ - You're okay with even lower strike

│

└─ Accept assignment IF:

- You're happy to own stock at that price

- You've collected good premium (profit target hit)

- Stock fundamentals are sound

NO (Stock above strike):

├─ Assignment unlikely

├─ Decision: Roll to next month or let expire?

│

├─ Roll IF:

│ - Stock is stable/slightly declining

│ - You want to compound premium income

│ - New premium justifies rolling cost

│

└─ Let expire IF:

- Stock is rallying (will be worthless)

- You've already hit profit targets

- You want to redeploy capital elsewhere

Example: Rolling Down (Stock Declining)

Original: Sold $50 put for $2.00, stock was $52

Now: Stock at $48, 25 DTE

Original put value: $2.50 (ITM, but DTE helps)

Scenario A: Let it ride (assignment likely)

Stock probably stays $45-50 range

Assigned at $50 cost basis

You own stock, can sell covered calls next

Scenario B: Roll down (if bullish on stock long-term)

Buy to close $50 put @ $2.50 = -$250

Sell to open $48 put for $1.80 = +$180

Net debit: -$70

New position: Short $48 put

Total collected: $2.00 + $1.80 = $3.80

New cost basis if assigned: $48 - $3.80 = $44.20

Result:

If stock recovers: Great! Collected $3.80 on lower strike

If stock keeps falling: Assigned at $48 (lower than $50)

Recommendation: Roll down if stock is decent company that's temporarily down

Don't roll if fundamentals are broken

Example: Rolling (Stock Stable)

Original: Sold $50 put for $2.00, stock was $52

Now: Stock at $51, 25 DTE

Original put value: $0.80 (OTM, still worth money)

Your choice: Roll or let expire?

Roll option:

Buy to close $50 put @ $0.80 = -$80

Sell new $49 put (next month) for $1.50 = +$150

Net credit: +$70 (you PROFIT on the roll!)

Total collected: $2.00 + $1.50 = $3.50

New cost basis if assigned: $49 - $3.50 = $45.50

Benefit: Extended position, collected additional premium (+$70)

Result: At next expiration, repeat process

Let expire option:

Keep your $0.80 profit (put expires worthless)

Total collected: $2.00

Move to new stock/position

Comparison:

Roll: $3.50 total over 60 days = 5.8% return on $50 required capital

No roll: $2.00 total over 30 days = 4% return on $50 required capital

Recommendation: Roll if premium justifies (net credit > $0.30)

Phase 3: 21-14 DTE (Last Good Roll Window)

What's Happening:

- Theta is extreme (2-3% daily decay)

- Current put is nearly worthless (if OTM) or deeply ITM (if ITM)

- Rolling spreads widen (liquidity thins)

- Assignment decision must be made

Rolling Considerations:

If OTM (Stock Above Strike):

Example: Sold $50 put, stock at $52, put worth $0.30

Should you roll?

Buy to close @ $0.30 = -$30

Sell new $50 put for $0.80 = +$80

Net credit: +$50

Total premium collected: $2.00 + $0.80 = $2.80

Days held so far: 16 days

Return per 16 days: $2.80 / $50 = 5.6%

Annualized: 130% (incredible!)

BUT: Rolling at 14 DTE means assignment is imminent next cycle

Better to just let it expire:

Keep $0.30 decay profit

Free up capital for new position

Don't create management burden

Recommendation: DON'T roll at 14 DTE if OTM

Let expire, move to new stock

If ITM (Stock Below Strike):

Example: Sold $50 put, stock at $47, put worth $3.20

Should you roll down?

Buy to close @ $3.20 = -$320

Sell new $46 put for $2.20 = +$220

Net debit: -$100

Cost to extend: $100

Remaining premium on new put: $2.20

Total premium if rolls: $2.00 + $2.20 = $4.20

Is it worth $100 to extend?

Only if:

A) You strongly believe stock will bounce back

B) You want to defer buying until later

C) The company has strong fundamentals

Recommendation: At 14 DTE, usually accept assignment

Let the put go ITM, get assigned

Own stock at $50 (cost basis $48 after premium)

Move on to next position

Don't throw more money after a losing trade

Best Practice at 21-14 DTE:

- If OTM: Let expire, don't roll (keep capital)

- If ITM: Usually accept assignment (rolling costs justify it)

- Only roll if you strongly believe in the stock long-term

- Rolling at 14 DTE only extends your management burden by 14 more days

Phase 4: 14-7 DTE (Final Stretch)

What's Happening:

- Assignment is essentially certain if ITM

- Rolling is rarely beneficial (not enough time value left)

- Your decision is binary: take assignment or close

At 14-7 DTE, Rolling is Usually a Bad Idea

Why?

Your put is 1-2 weeks from expiration

If OTM:

Roll costs your remaining decay profit ($0.20-0.30)

New position only has 14-30 days

Not worth the complexity

If ITM:

Rolling down costs significant money ($150-300+)

New position still faces assignment risk

Better to just accept assignment now

In both cases: Just let it expire or accept assignment

Don't keep rolling, extending, and extending

Exception: Major Reversal Signal

Stock crashed 20% over 2 weeks due to earnings

Now recovering sharply

ITM put that was worth $3.00 is now worth $1.50

Stock appears to have bottomed

Option: Roll down to lock in assignment price

Buy to close deep put @ $1.50

Sell new slightly lower put @ $1.00

Net debit: $50 (small cost)

Reasoning:

You believe stock has bottomed

Assignment at new lower strike is acceptable

One more roll captures upside reversal

Recommendation: Rare, but acceptable if conviction is high

Best Practice at 14-7 DTE:

- Don't roll unless stock has reversed sharply

- Accept assignment and move on

- Use freed capital for new positions

- Rolling at this stage extends stress without benefit

Cost Basis Management When Rolling

Rolling affects your cost basis if you eventually take assignment.

Example: Two CSP Rolls

Trade Sequence:

Month 1 (30 DTE):

Sell $50 put for $2.00

Collect: $200

At 15 DTE:

Buy to close $50 put @ $1.50 = -$150

Sell new $50 put for $1.60 = +$160

Net credit: +$10 (small profit on roll!)

Total premium collected: $2.00 + $1.60 = $3.60

Month 2 (30 DTE new expiration):

Stock at $49, still holding short put

Let it expire, assigned at $50

Assignment Result:

You buy 100 shares at $50 strike

But you collected $3.60 in premiums

Effective cost basis: $50 - $3.60 = $46.40 per share

On $5,000 stock purchase:

Actual cost: $5,000

Premium collected: $360

Net cost: $4,640

Savings: $360 (7.2% discount!)

Tax Implications of Rolls

When you roll, you realize a gain/loss on the closed put:

In example above:

Sold $50 put: $2.00 premium

Closed $50 put: $1.50 cost

Gain: $0.50 per share = $50 short-term capital gain

Then: Sold new $50 put for $1.60

Gain: $1.60 per share (if expires worthless)

Tax result (37% bracket):

$50 gain: $18.50 tax

$160 gain: $59.20 tax

Total: $77.70 tax on $360 profit

Net after-tax: $282.30

Best Practice:

- Track each roll separately for tax purposes

- In Roth IRA: No tax on rolls (huge benefit)

- In traditional account: Expect ordinary income tax on premiums

When to Stop Rolling and Accept Assignment

Rolling can become addictive. You keep rolling to extend positions indefinitely.

Stop Rolling When:

| Signal | Meaning | Action |

|---|---|---|

| You've rolled 3+ times | Original position is "dead" | Accept assignment, move on |

| Stock down 30%+ from strike | Fundamentals have broken | Close position, take loss |

| You're down 75%+ of max loss | Risk/reward is terrible | Close position, preserve capital |

| Fundamentals deteriorated | Earnings miss, bad news, guidance down | Don't extend; accept assignment |

| You keep adding capital to roll | You're throwing good money after bad | STOP. Accept assignment. |

| You've held position 6+ months | You've collected full premium cycles | Assign and move to new stock |

The 3-Roll Rule:

After 3 rolls on the same stock, accept assignment. Here's why:

Original: Sold $50 put for $2.00

Roll 1 (15 DTE): Sell new put for $1.60, cost -$0.50 net

Roll 2 (15 DTE): Sell new put for $1.40, cost -$0.60 net

Roll 3 (15 DTE): Sell new put for $1.20, cost -$0.70 net

Total premium: $2.00 + $1.60 + $1.40 + $1.20 = $6.20

Total rolling costs: -$0.50 - $0.60 - $0.70 = -$1.80

Net premium: $6.20 - $1.80 = $4.40

Time elapsed: ~4.5 months (3 × 45-day cycles)

Return: $4.40 / $50 = 8.8% over 4.5 months = 23% annualized

This is excellent! So why stop?

Because:

A) You've already captured the income

B) Assignment risk compounds (stock keeps declining)

C) Management complexity increases (4+ positions)

D) Better opportunities elsewhere (fresh CSPs on rising stocks)

Real Example: Complete CSP Rolling Scenario

The Setup:

November 2025: Stock XYZ at $100

Sell 1 XYZ $95 put, 45 DTE

Collect: $2.50 premium

Thesis: XYZ is strong; willing to own at $95

Month 1 (30 DTE decision point):

Stock is at $98 (minor decline)

Put is worth $1.80

Decision: Roll or hold?

Analysis:

Stock is still strong (only -2%)

New 30-DTE $95 put trades for $1.80

Rolling would cost: Buy @ $1.80, sell @ $1.80 = Neutral cost

Decision: ROLL (neutral cost, extend income)

Buy to close $95 put @ $1.80 = -$180

Sell new $95 put for $1.80 = +$180

Net: $0 (breakeven on the roll)

Total premium collected: $2.50 + $1.80 = $4.30

New position: Short $95 put, 30 DTE

Month 2 (15 DTE decision point):

Stock is at $97 (recovering!)

Put is worth $0.60

Decision: Roll or let expire?

Analysis:

Stock has recovered; $95 is now too low

Put will expire worthless

Remaining decay: $0.60

Rolling option:

Buy @ $0.60, sell new $95 put for $0.80 = $20 credit

But adds another 30-day management period

Decision: DON'T ROLL (let expire)

Keep the $0.60 decay

Free up capital

Move to new CSP on different stock

Total premium on XYZ: $2.50 + $1.80 + $0.60 = $4.90

Time held: 60 days

Return: $4.90 / $95 = 5.2% = 31% annualized

Result: Excellent trade! Move on.

Alternative Month 2 (if stock had crashed):

Stock is at $92 (crashed!)

Put is worth $3.20 (deep ITM)

Decision: Roll down or accept assignment?

Analysis:

Stock crashed 8% - something might be broken

Rolling down to $90 would cost: Buy @ $3.20, sell @ $2.40 = -$80 debit

Not worth extending

Decision: ACCEPT ASSIGNMENT

You get 100 XYZ at $95

Effective cost basis: $95 - $4.30 = $90.70

Market price: $92 (underwater by $2.70)

But: You collected $430 premium

Stock only needs to recover to $92.70 to profit

Already getting close

Result: Own XYZ at good basis, plan to sell covered calls next

Premium Income After Every Roll

How credits and debits stack up month by month in a real options income portfolio.

Income Calendar

Option cash in/out by the month each fill settled

Connect your broker and see your own income calendar — every credit and buyback, month by month.

The Bottom Line: CSP Rolling Strategy

Master These Rules:

✅ Roll only 30-45 DTE (best risk/reward)

✅ Roll only if net credit > $0.30 (worth the complexity)

✅ Don't roll if fundamentals deteriorated (accept loss)

✅ Accept assignment after 3 rolls (capitalize on gains)

✅ Let OTM puts expire at 14 DTE (no point rolling)

✅ Plan cost basis management (track for taxes)

Rolling compounds CSP income efficiently—but only when done strategically. Random rolling = extended stress with minimal additional profit.

Use rolling to extend income-generating positions on solid companies. Avoid rolling to chase losses or avoid decisions.

Next Steps

Ready to master CSP rolling?

First: Paper trade 3 complete CSP cycles (sell, hold, expire or roll).

Second: Track your rolling decisions—when they worked, when they didn't.

Third: Build your personal rolling rules based on your risk tolerance.

Fourth: Go live and compound premium income through strategic rolling.

Rolling done right turns CSP positions into long-term income machines. Roll discipline done wrong turns them into endless management nightmares.

Choose discipline. Let the compounding work for you.

Frequently Asked Questions

When is the best time to roll a cash-secured put?

The best time to roll is 21-30 DTE when theta is accelerating and new option premiums are still attractive. At 45 DTE it's too early (you're giving up time value). At 14 DTE it's often too late (spreads widen, assignment is imminent).

Should I roll for a credit or debit?

Always aim for a net credit or breakeven roll. Rolling for a debit extends your risk and increases your cost basis. If you can't roll for at least breakeven, consider accepting assignment instead of throwing good money after bad.

How many times should I roll the same position?

Follow the 3-Roll Rule: after 3 rolls, accept assignment. Rolling more than 3 times usually means you're avoiding a decision or the stock has fundamentally changed. Take assignment and redeploy capital to better opportunities.

What's better: rolling down or accepting assignment?

Accept assignment if the stock has dropped significantly (>15% from strike) or if fundamentals have deteriorated. Only roll down if you strongly believe in a near-term recovery and can collect meaningful additional premium.

How do rolls affect my cost basis for taxes?

Each roll is a taxable event. When you buy to close the original put, you realize a gain or loss. The new put starts fresh. Track each leg separately for tax purposes. In an IRA, rolls have no tax consequences.

Can I roll a put that's already in-the-money?

Yes, but carefully. Rolling an ITM put extends your position and can lower your effective strike price. Calculate your new breakeven: Original Strike - Total Premium Collected - Roll Credit. Make sure the new position still makes sense.

Related Articles

- Best DTE for Cash Secured Puts Wheel Strategy 2026

- IBKR Cash Secured Puts

- Cash Secured Puts

- Cash-Secured Puts Playbook: DTE Optimization & Assignment Risk

- Best Stocks for Selling Cash-Secured Puts: 2025 Screening Guide

- Best Stocks for Selling Cash-Secured Puts in 2026 — 2026 sector picks and DTE-optimized entries

Expertise: This article is written by the Days to Expiry Trading Team, Options Strategy Specialists with 10+ years of trading experience. For detailed author credentials and regulatory status, see our author page. This content is educational only and does not constitute financial advice.

Use our Strategy Analyzer to compare CSP premiums across strikes and expirations, then track your adjusted positions with the portfolio tracking methodology that works for covered calls.

- Cash Secured Put Strategy: A Complete Guide to Income Generation

- Selling Cash Secured Puts: The Complete Beginner's Guide to Income

- Sell Put Option Example: A Real AAPL Walkthrough from Strike Selection to Assignment

Expertise: Written by an Options Strategy Specialist with 10+ years of active trading experience. Cited sources: CBOE educational materials on options assignment and FINRA investor education on early exercise.

Ready to manage assignment risk? Apply these rolling rules to your next cash-secured put trade and track your adjusted cost basis carefully.

Frequently Asked Questions

Written by Days to Expiry Trading Team

The Days to Expiry trading team brings together experienced options traders and financial analysts dedicated to helping investors generate consistent income through proven options strategies.

Continue Your Journey

Covered Call Analyzer

Find the best covered call opportunities.

Cash-Secured Put Calculator

Calculate put selling returns.

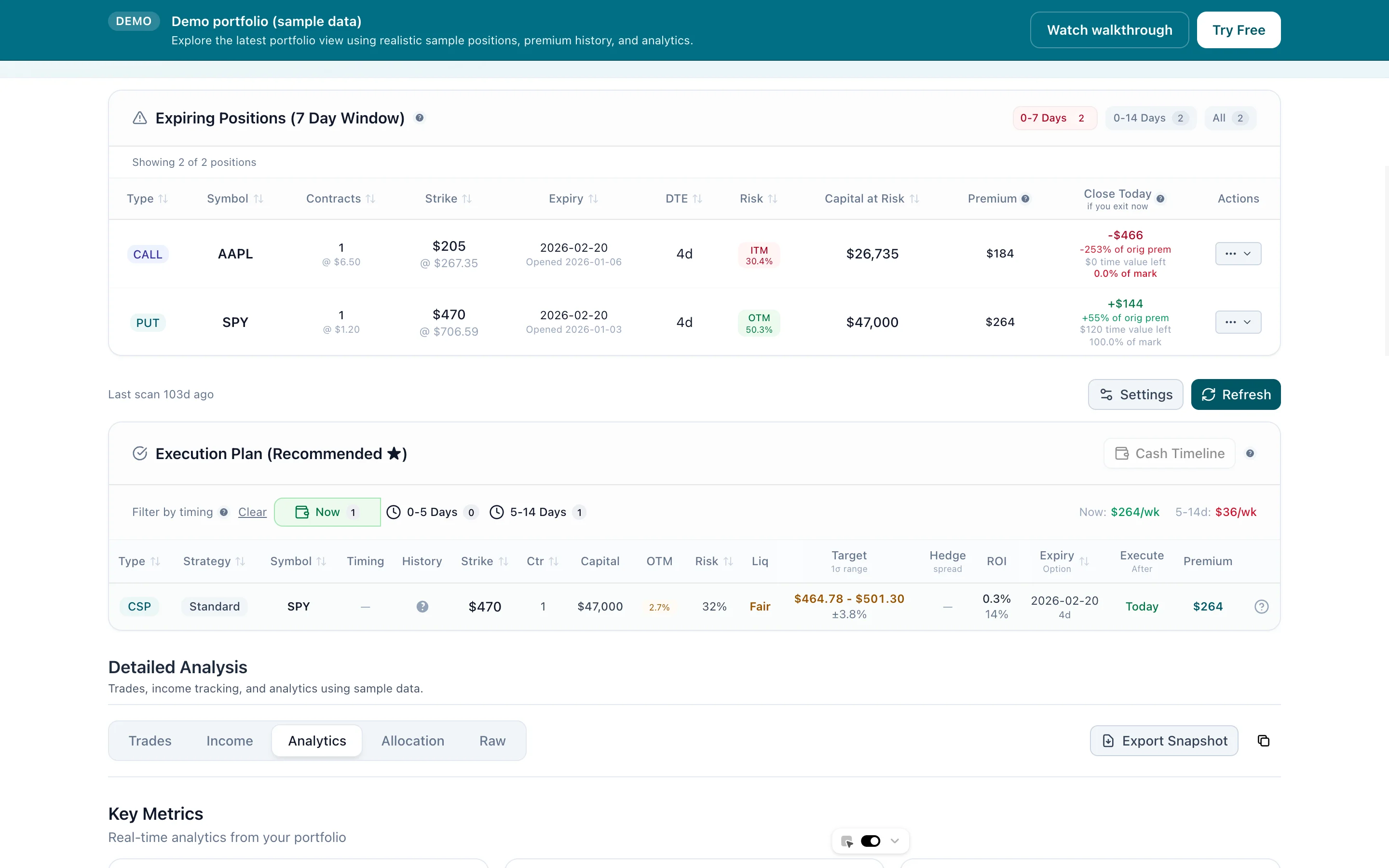

Demo Portfolio

Explore a sample portfolio with positions and strategy insights — no login required.

Wheel Strategy Calculator

Plan your wheel trades.

Free trial

Start free — then keep the full workflow

- Multi‑stock covered call and cash‑secured put scans

- Strategy backtesting for covered calls and puts

- Full wheel backtesting with buy‑and‑hold comparison

- AI Portfolio Scanner for advanced recommendations