Wash Sale Rules for Options Traders: The Complete Guide helps you understand whether options with different expirations are substantially identical under IRS rules. While expiration dates alone usually don't trigger wash sales, deep in-the-money options with the same strike may be treated as substantially identical to the stock if repurchased within 30 days.

Wash Sale Rules for Options Traders: The Complete Guide

Options with different expiration dates are generally not considered substantially identical for wash sale purposes because the IRS evaluates whether securities are identical in all material respects, and varying expirations create different economic rights and obligations. However, deep in-the-money options with near-identical strike prices and very close expirations may still trigger wash sale rules depending on specific circumstances.

This guide explains exactly how wash sale rules apply to options traders, with real examples, IRS guidance interpretation, and practical strategies to stay compliant while maximizing your tax efficiency.

Here's the basic rule:

If you sell a security at a loss, you can't deduct that loss if you buy the same (or substantially identical) security within 30 days before or 30 days after the loss.

For options traders, this creates a minefield. Selling cash-secured puts, rolling positions, and harvesting losses all trigger wash sale risks. Unlike stock investors who might harvest a loss once per year, active options traders can inadvertently trigger wash sales weekly through rolling, assignment, and rapid re-entry. Understanding the specific mechanics for options is essential because broker 1099-B reporting often misses nuanced options scenarios, leaving you to reconcile discrepancies at tax time.

Why Options Traders Face Unique Wash Sale Complexity

Stock investors typically worry about wash sales when tax-loss harvesting in December. Options traders face a continuous compliance challenge because:

- Rolling positions involves closing a losing short option and opening a new one, sometimes on the same underlying within days

- Put assignments create purchase events that start the 30-day clock before you even realize a loss

- Spread adjustments can trigger wash sales on individual legs even when the overall strategy is profitable

- Multiple expiration cycles mean you may close a March position at a loss and open an April position within the wash sale window without recognizing the risk

The IRS applies the same "substantially identical" standard to options as it does to stocks, but the analysis is more complex because options have multiple dimensions: underlying, strike, expiration, and option type (call vs. put). Two options on the same stock are not automatically substantially identical, but the closer they are in strike and expiration, the more likely the IRS would treat them as such.

Turn Tax Rules Into A Review Workflow

Spot wash sale risk in assignments, exits, and replacement trades before tax time.

Dive deep into all trades of your IBKR portfolio with detailed transaction analysis

Dive deep into all trades of your IBKR portfolio with detailed transaction analysis

This guide walks through real scenarios and shows you exactly how to avoid the trap.

The Wash Sale Rule: Basic Mechanics

The wash sale rule applies to sales at a loss. It doesn't apply to gains.

The 61-day window:

- 30 days before the loss sale

- The loss sale date

- 30 days after the loss sale

Within this window, you can't buy substantially identical securities.

If you do:

- The loss is disallowed (you can't deduct it)

- Your basis in the new shares is increased by the disallowed loss

- The loss is deferred until you sell the new shares

Real Example: Simple Wash Sale

- 1/15/2025: Buy 100 SPY at $420/share (cost: $42,000)

- 2/20/2025: Sell 100 SPY at $400/share (loss: -$2,000)

- 2/21/2025: Buy 100 SPY at $395/share (cost: $39,500)

Analysis:

| Date | Action | Days from Loss Sale |

|---|---|---|

| 1/15 | Buy 100 SPY @ $420 | -36 days (within 30-day window) |

| 2/20 | Sell 100 SPY @ $400 (LOSS) | 0 |

| 2/21 | Buy 100 SPY @ $395 | +1 day (within 30-day window) |

Wash sale triggers:

- You sold at a loss (2/20)

- You bought within 30 days after (2/21)

- The -$2,000 loss is disallowed

Tax consequences:

- Your new basis in the 100 shares: $39,500 + $2,000 (disallowed loss) = $41,500

- You've deferred the loss until you sell these shares

- If you sell the new shares at $395, you realize only -$1,500 loss (the $2,000 is deferred)

When Wash Sale Rules Apply to Options Traders

Options traders hit wash sale rules in three main scenarios:

Scenario 1: Selling Puts and Buying Stock

You sell a cash-secured put expecting it to expire worthless. It gets assigned (you buy stock at the strike price). Later, you sell that stock at a loss.

Example:

- 1/15/2025: Sell 100 SPY $400 puts for $2.00 premium

- 1/20/2025: Assigned; you buy 100 SPY at $400/share

- 1/21/2025: SPY drops; you sell the stock at $390/share (loss: -$1,000)

- 1/22/2025 - 2/20/2025: You decide to buy 100 SPY again at a better entry point

Wash sale analysis:

The loss sale (1/21) is within 30 days of:

- Put sale (1/15) = before the sale

- Put assignment (1/20) = before the sale

When you buy again after 1/21, you're within the 30-day window.

Result: Your -$1,000 loss is disallowed. Your new cost basis is increased by $1,000.

Scenario 2: Rolling Positions

You sell a call spread at a loss. You immediately buy back the spread and open a new one.

Roll decision analyzer tool showing assignment probability and timing across DTE stages

Roll decision analyzer tool showing assignment probability and timing across DTE stages

Example:

- 1/1/2025: Sell a call spread (short $450 call, long $460 call) for $1.00 credit

- 1/15/2025: Stock drops; spread is worth $0.20. You buy back for a loss: $1.00 sold, $0.20 closed = -$0.80 loss (-$80)

- 1/16/2025: You sell a new call spread (short $445 call, long $455 call) for $0.90 credit

Wash sale analysis:

Is the new spread "substantially identical" to the old spread?

No. Spreads with different strikes are considered different securities. So wash sale rules don't apply here.

But: If you sold a call spread (short $450 call) at a loss and bought back the exact same $450 call at a loss, then immediately sold the same $450 call again, wash sale might trigger.

Key distinction:

- Different strikes = No wash sale

- Same strike, same expiration, bought and immediately resold = Possible wash sale

Scenario 3: Tax Loss Harvesting in a Stock Position

You own 100 shares of a stock at a loss. You want to harvest the loss for taxes but keep market exposure.

Example:

- 1/15/2025: Buy 100 AAPL at $200/share

- 1/31/2025: AAPL is at $180/share; you sell at loss (-$2,000)

- 2/1/2025: You sell a call spread on AAPL to maintain exposure (instead of buying stock)

- 2/15/2025: You reconsider and buy 100 AAPL at $175/share

Wash sale analysis:

- Sold at loss: 1/31

- Bought AAPL calls within 30 days after: 2/1

- Bought AAPL stock within 30 days after: 2/15

Question: Do call options trigger wash sale rules?

IRS position: Selling calls (not buying) does NOT trigger wash sale. But buying calls within 30 days of selling stock at a loss might.

The IRS has stated that buying call options (even out-of-the-money) can trigger wash sale rules because they provide downside protection similar to still owning the stock.

Conservative rule: If you sell a stock at a loss, don't buy calls or buy stock within 30 days before or after.

Options and Wash Sales: The Gray Area

The IRS has issued mixed guidance on whether options trigger wash sale rules.

Official Guidance (and Common Misunderstandings)

IRS Notice 2008-70 addressed wash sale rules and options, stating:

- Buying calls to replace a sold stock: Can trigger wash sale if calls provide substantial downside protection

- Selling calls: Does NOT trigger wash sale (you're not replacing the position)

- Selling puts: Might trigger wash sale if you buy stock within 30 days (the assignment counts as a purchase)

In practice:

- Buying protective puts: Likely triggers wash sale (you're insuring against loss)

- Selling puts: Triggers wash sale IF assigned and you later sell the stock at a loss

- Selling calls: Does NOT trigger wash sale

Real Example: Buying Protective Puts

- 1/15/2025: Buy 100 AAPL at $200/share

- 2/1/2025: AAPL drops to $180/share

- 2/1/2025: You realize you should have sold, but instead buy a $180 protective put

- 2/10/2025: You decide to sell the 100 AAPL at $180 (loss: -$2,000)

- 2/11/2025: AAPL drops further; you regret selling and buy 100 AAPL at $170

Analysis:

When you bought the protective put (2/1), you replaced the sold position with a synthetic long position (stock + put = protected long).

Wash sale question: Does buying the put trigger wash sale on the later stock loss?

IRS answer: Possibly. The put provides downside protection equivalent to still owning the stock. The wash sale rule's intent is to prevent people from selling losses and immediately re-acquiring "substantially identical" positions. Buying a protective put is arguably re-acquiring economic exposure.

Practical result: The IRS would likely disallow the -$2,000 loss.

Real Example: Selling Puts at a Loss

- 1/1/2025: Sell 1 SPY $410 put for $2.00 (credit: $200)

- 1/31/2025: SPY drops to $390; put is worth $20 (intrinsic value $20 + time value $0)

- 2/1/2025: You buy back the put for $20 (loss: $2.00 - $0.20 = $1.80, or -$180)

- 2/2/2025: You sell the same $410 put again for $1.50 credit

Analysis:

You sold a put at a loss ($180 loss) and immediately sold the same put again at a similar strike.

Wash sale question: Does this trigger wash sale?

IRS answer: No, probably not. You're selling (not buying) the same instrument. Wash sale rules apply to disallowed losses, not to re-entering the same trade.

But: The IRS might argue that the $180 loss is premature (the position wasn't truly closed; you immediately re-entered it). This is more of a "substance over form" argument than wash sale.

Real Example: Assigned Puts and Later Sale at Loss

- 1/1/2025: Sell 1 SPY $410 put for $2.00 (credit: $200)

- 1/15/2025: Assigned; you buy 100 SPY at $410/share (cost: $41,000)

- 2/1/2025: SPY is at $400; you sell 100 SPY for loss (-$1,000)

- 2/2/2025: SPY drops further; you buy 100 SPY at $395/share

Wash sale analysis:

- Sold at loss: 2/1

- Bought substantially identical: 2/2 (within 30 days)

- Previous buy (assignment): 1/15 (within 30 days BEFORE the loss sale)

Wash sale triggers:

- The assignment (1/15) is within 30 days before the loss sale (2/1)

- The new purchase (2/2) is within 30 days after

- Your -$1,000 loss is disallowed

The -$1,000 loss is added to the cost basis of the shares purchased on 2/2. Your new basis: $39,500 + $1,000 = $40,500.

How to Avoid Wash Sale Problems

Understand put assignment risk and how it triggers wash sales. The most effective prevention combines clear record-keeping, conservative timing, and understanding which strategies legitimately bypass the rule entirely. The following rules are ordered by practical impact—start with tracking the 61-day window, then layer in the more advanced techniques.

Assignment Stress Test

Test your position under adverse market scenarios to understand assignment risk and potential losses.

Base Assignment Probability

30%

Premium Collected

$250

Maximum Loss

$43,750

Scenario Analysis

| Price Move | Final Price | Assignment Prob | P/L | Status |

|---|---|---|---|---|

| Current | $450.00 | 15% | $250 | Safe |

| -5% | $427.50 | 32.9% | $-1,000 | At Risk |

| -10% | $405.00 | 38.6% | $-3,250 | At Risk |

| -20% | $360.00 | 52.2% | $-7,750 | At Risk |

Break-even: $437.50 • Blue row shows current price scenario

Find real options with similar parameters

Rule 1: Track the 61-Day Window Carefully

Create a spreadsheet:

| Date | Action | Notes |

|---|---|---|

| 1/15 | Sell AAPL 100 @ $180 (loss: -$2,000) | Loss sale date |

| 1/16-2/14 | Can't buy AAPL or call options | 30 days after = 2/14 |

| 2/15 | Earliest date to buy AAPL | 31 days after = 2/15 |

Be conservative: Many traders use 31 days after (not 30) to be safe.

Rule 2: Don't Use Protective Puts After a Loss

If you're going to harvest a tax loss, don't buy protective puts to stay in the trade.

Instead:

- Sell the stock at a loss

- Wait 31 days

- Buy the stock back (or protective puts)

- Then you've reset the clock

Rule 3: After Selling at a Loss, Avoid Related Options

After selling a stock at a loss:

| Action | Within 30 Days After Loss Sale? | Wash Sale Risk? |

|---|---|---|

| Buy call options on same stock | Within window | HIGH RISK (downside protection) |

| Buy protective puts on same stock | Within window | HIGH RISK |

| Sell covered calls on same stock | Within window | LOW RISK (but avoid if re-buying soon) |

| Trade options on different stock | Within window | NO RISK |

| Roll uncovered calls | Within window | LOW RISK (unless you're re-acquiring stock) |

Conservative approach: After a loss sale, wait 31 days before trading options on the same underlying.

- Options Tax & Compliance: Trader's Complete Guide

- Free Trading Journal: Best Tools, Templates & Setup Guide

Rule 4: Track Put Assignments Carefully

If you sell puts and get assigned, you've bought stock at the strike price. If you later sell that stock at a loss, wash sale rules apply to all buys within 30 days before and after the loss sale.

Example to avoid:

- 1/1/2025: Sell puts, assigned 1/10/2025 (stock cost: $410)

- 1/25/2025: Sell stock at $400 (loss: -$1,000)

- 1/26/2025: DON'T buy the stock again

- 2/15/2025: NOW you can buy

When to break this rule:

- If you didn't know wash sale rules (defer compliance)

- If the loss is small enough that deferral is acceptable

- If the IRS is unlikely to audit you

Using Losses Strategically (While Respecting Wash Sales)

Plan your loss harvesting strategy and understand the tax impact:

Tax-Aware Net Income Calculator

Calculate your true take-home income after taxes and fees. Understand the real yield on your option strategies.

Total premium collected before taxes/fees

Total capital securing positions

Short-term rate: 24% (most option premiums)

Transaction Fees

Fee impact: 0.7% of gross income

Gross Income

$1,000

2% yield

Fees

-$7

Taxes (24%)

-$238

Net Income

$755

1.51% net yield

Tax Bracket Sensitivity Analysis

| Tax Region | Tax Rate | Net Income | Net Yield |

|---|---|---|---|

| Federal (22%) | 22% | $775 | 1.55% |

| Federal (24%)(Current) | 24% | $755 | 1.51% |

| TX/FL (No State) | 24% | $755 | 1.51% |

| Federal (32%) | 32% | $676 | 1.35% |

| Federal (35%) | 35% | $646 | 1.29% |

| NY (High) | 35% | $646 | 1.29% |

| CA (High) | 37% | $626 | 1.25% |

Shows how your net income changes across different tax jurisdictions

Tax Disclaimer: This calculator provides illustrative estimates only. Tax treatment varies by jurisdiction, income level, and individual circumstances. Consult a qualified tax professional for personalized advice. Options premiums are typically taxed as short-term capital gains in the US.

Discover real options to generate tax-efficient income

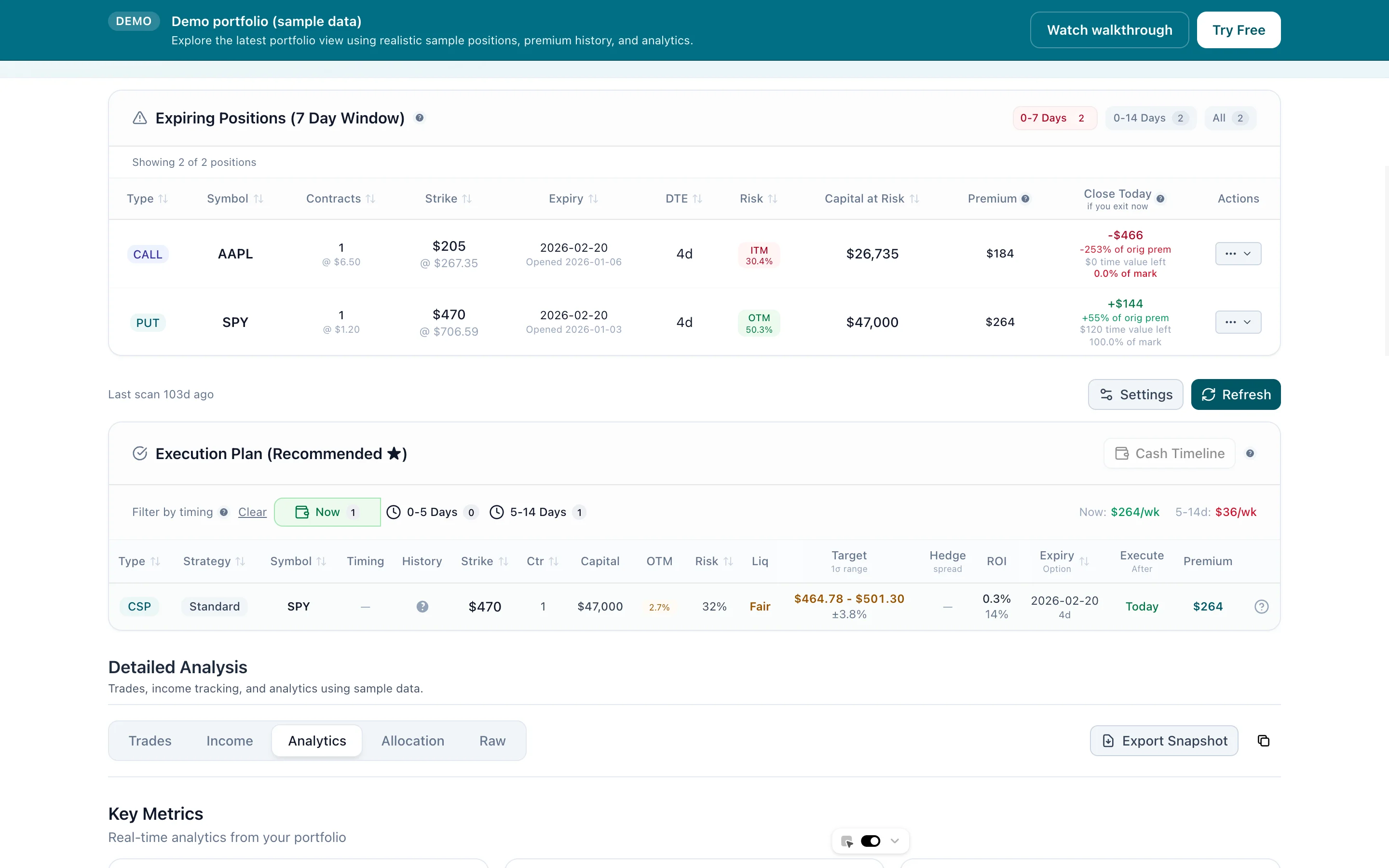

How Days to Expiry Helps You Review Wash Sale Risk

Wash sale issues usually come from activity patterns, not one isolated trade. Assignment, loss realization, and re-entry often happen across multiple sessions, which is exactly why they get missed.

That is where Days to Expiry is useful:

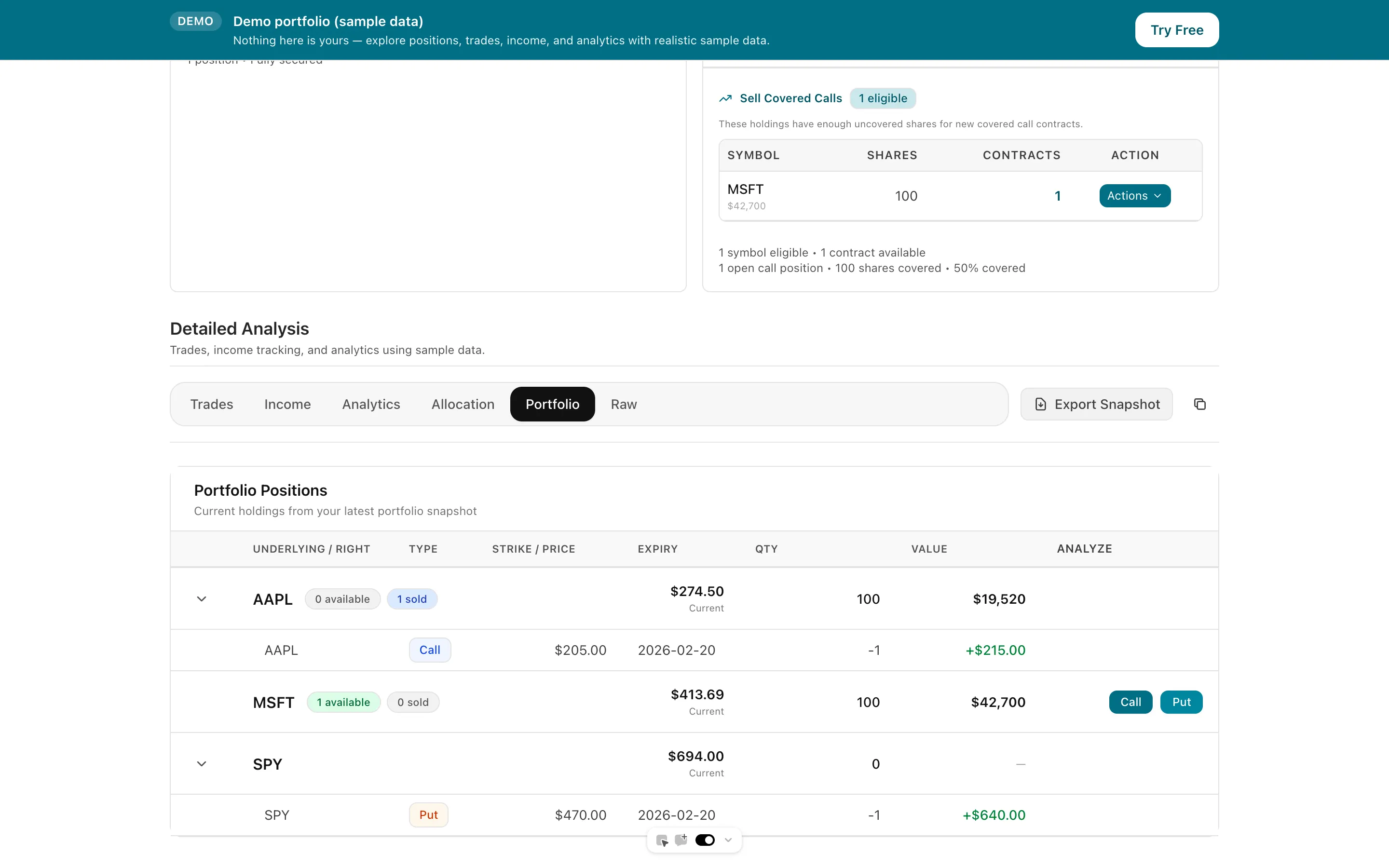

- Use Portfolio View to review the underlying sequence of assignments, exits, and re-entries instead of relying on memory.

- Use Interactive Brokers Options if your trade history lives in IBKR and you need a cleaner path from broker records to review.

- Use the tax concepts in this guide as a checklist for what to investigate, not as a substitute for portfolio-level visibility or tax advice.

Practical next step: Review any underlying where you were assigned, sold at a loss, and re-entered quickly. If you cannot reconstruct that sequence confidently from your broker screens, that is already a signal that your recordkeeping needs improvement.

Strategy 1: Harvest Losses, Then Wait 31 Days

- 1/15: Sell a losing position

- 1/16-2/14: Don't buy back (avoid wash sale)

- 2/15: Buy back with full loss deduction taken for 2024 taxes

- Can use loss to offset gains or reduce income by $3,000 (or carry forward)

Build a diversified portfolio while respecting the 31-day window:

Portfolio Income Calculator

Diversify income across multiple stocks for steady monthly cash flow

Strategy 2: Use Loss Harvesting to Offset Gains

If you have a profitable call spread and a losing stock position:

- Sell the stock at a loss (harvest: -$2,000)

- Use the loss to offset call spread gain of +$2,000

- Net: $0 taxable gain (no capital gains tax)

- Don't re-buy the stock for 31 days

Strategy 3: Use Different Securities to Stay in the Trade

If you sell SPY at a loss and want to stay exposed to the S&P 500:

- Sell 100 SPY at a loss (harvest: -$2,000)

- Wait 31 days

- Buy 100 IVV or VOO (similar S&P 500 ETF)

- Not a wash sale (different securities; SPY and IVV are not "substantially identical")

But: Some tax professionals argue that buying a different S&P 500 ETF might still be considered "substantially identical" for wash sale purposes.

Conservative approach: Wait 31 days and buy the same security back, or use a different asset class entirely.

Strategy 4: Use Call Spreads to Replace a Sold Position

If you sell a stock at a loss and want market exposure:

- Sell stock at loss (harvest: -$2,000)

- Sell call spreads on the same stock (short $450 call, long $460 call)

- Wait 31 days

- Buy stock back if you want

Is this a wash sale?

Selling calls (not buying) does NOT create a wash sale. You're not re-acquiring the position immediately.

But some tax professionals would argue that selling call spreads (especially if sold for a net credit and structured as a synthetic long) might trigger wash sale.

Conservative approach: Wait 31 days if possible. The tax savings aren't worth the audit risk.

Tracking Wash Sales on Your Tax Return

If Wash Sale Happens (and is disallowed by IRS)

You'll see a wash sale adjustment on your 1099-B from your broker:

Box 3 on 1099-B: "Wash sale loss disallowed"

The IRS will also send you a notice of the disallowance.

How to Handle It on Form 8949

When filing taxes, you report the wash sale loss disallowance on Form 8949:

- List the loss sale

- Box "Wash sale loss disallowed": Enter the disallowed amount

- The disallowed loss is added to the cost basis of the new purchase

How to Adjust Your Basis in Tax Software

TurboTax:

- Go to Investment Income → 1099-B Sales

- Import your 1099-B data

- For each wash sale entry, TurboTax will ask if you made a wash sale purchase

- Adjust basis accordingly

H&R Block: Similar process through Investment Income → 1099-B Data

Common Wash Sale Mistakes

Mistake 1: Selling a Call Spread at a Loss, Then Buying Back the Short Call

- Sell $450/$460 call spread for $1.00 (net credit: $100)

- Stock drops; spread is now worth $0.30 (you could close for -$0.70 loss = -$70)

- You buy back the short $450 call at $0.50 (loss: $1.00 sold, $0.50 closed = gain $0.50, not a loss)

- BUT your long call is still open

Wash sale analysis:

- You haven't realized a loss on the spread (the net P&L is a loss, but buying back only half the spread doesn't lock in a loss)

- No wash sale trigger

But if you buy back the entire spread at a loss and immediately sell it again at a similar price:

- Possible wash sale (you're reselling the same spread immediately)

Mistake 2: Selling Stock at a Loss, Then Opening a Buy-Write (Stock + Call)

- 1/15: Sell 100 AAPL at $180 (loss: -$2,000)

- 1/16: Open a buy-write: Buy 100 AAPL at $175 + sell $180 call for $2.00

Wash sale analysis:

You bought back AAPL within 30 days of selling at a loss = WASH SALE TRIGGERED.

The short call (sold for $2.00) doesn't exempt you from wash sale. You've re-acquired the stock.

Correct approach:

- Sell stock at loss (1/15)

- Wait 31 days (until 2/15)

- Open buy-write (2/15)

Mistake 3: Forgetting About Put Assignments in Your 30-Day Count

- 1/1: Sell puts; assigned 1/5 (buy 100 shares)

- 1/20: Sell shares at loss

- 1/21: Buy shares again

Wash sale analysis:

- Assignment date (1/5) is within 30 days before the loss sale (1/20)

- New purchase (1/21) is within 30 days after

- WASH SALE TRIGGERED

All three events (assignment, loss sale, re-purchase) are within the 61-day window.

Wash Sales and Multiple Positions

If you own multiple positions in the same stock at different cost bases, wash sale rules track separately for each cost lot.

Example:

- Lot A: 100 AAPL bought at $200/share (Jan)

- Lot B: 100 AAPL bought at $190/share (Feb)

- 2/15: Sell Lot A at $185 (loss: -$1,500)

- 2/16: Buy 100 AAPL at $180 (within 30 days)

Analysis:

- Loss: -$1,500 on Lot A

- New purchase: 100 shares on 2/16

- Wash sale applies to the new purchase: Cost basis becomes $180 + $1,500 (deferred loss) = $1,680 per share

The new shares are treated as a replacement for Lot A.

Legal Ways to Avoid or Reduce Wash Sale Impact

The wash sale rule isn't absolute. Two legitimate strategies can eliminate or reduce its impact: Section 1256 contracts and Mark-to-Market (MTM) trader status.

Section 1256 Contracts: Wash Sale Exempt

Section 1256 contracts are exempt from wash sale rules entirely. Under IRC §1256, these contracts are marked to market at year-end—all positions are treated as if sold on December 31, regardless of whether you actually closed them.

Section 1256 contracts include:

- Broad-based index options (SPX, RUT, NDX, XSP)

- Regulated futures contracts (ES, NQ, /CL)

- Foreign currency contracts

Why wash sales don't apply:

The mark-to-market treatment means every position is deemed closed at year-end. There's no "substantially identical" replacement problem because the tax code recognizes the position as settled annually.

Practical example:

- 12/1: Buy SPX $4500 call for $10.00

- 12/5: Sell SPX $4500 call for $5.00 (loss: -$500)

- 12/6: Buy SPX $4500 call for $5.50

With SPY options, this would trigger a wash sale. With SPX options, no wash sale—Section 1256 contracts are exempt.

Bonus: Section 1256 gains are taxed at the favorable 60/40 rate (60% long-term, 40% short-term), regardless of holding period. For a detailed breakdown, see SPX Options Tax Treatment.

Important limitation: Single-stock options (AAPL, TSLA, etc.) are not Section 1256 contracts. Only broad-based index options and futures qualify.

Mark-to-Market (MTM) Trader Status (Section 475(f))

If you qualify as a trader (not investor) under IRS rules and elect Section 475(f) mark-to-market accounting, wash sale rules do not apply to your trading activity.

How it works:

Under MTM, all positions are treated as if sold at fair market value on the last business day of the year. Because every position is "closed" at year-end:

- Losses are fully deductible (no $3,000 cap)

- Wash sale rules don't apply

- Gains and losses are ordinary income/loss (not capital)

To qualify, you must:

- Trade frequently and regularly (not just a few times a month)

- Seek to profit from short-term price swings (not long-term appreciation)

- Spend substantial time trading (it must be a significant activity)

- File the election by the due date of your prior-year return (for new traders) or by April 15 for existing traders

Filing the election:

- Attach a statement to your tax return stating you're electing Section 475(f) treatment

- The election applies to the following tax year (you can't retroactively elect for the current year)

- Once elected, it applies to all future years unless you revoke it (which requires IRS permission)

Trade-offs:

| Benefit | Drawback |

|---|---|

| No wash sale rules | All gains taxed as ordinary income (no 60/40 or LTCG rates) |

| Unlimited loss deduction (no $3k cap) | Losses are ordinary, not capital (can't offset capital gains from investments) |

| Simplified record-keeping | Must meet strict "trader" qualification |

| Can deduct trading expenses on Schedule C | Self-employment tax may apply |

Who should consider MTM?

- Very active traders making hundreds of trades per year

- Traders who frequently trigger wash sales through rolling and repositioning

- Traders whose wash sale disallowances significantly distort their tax picture

Who should avoid MTM?

- Buy-and-hold investors with some options activity

- Traders who benefit from long-term capital gains rates

- Anyone who can't clearly demonstrate "trader" status to the IRS

Consult a tax professional before electing MTM. The election is difficult to revoke and changes how all your trading gains/losses are taxed.

Vertical Spreads and Wash Sales: The Broker Trap

A common and confusing situation: you partially close a vertical spread for a profit overall, but your broker reports a wash sale on one leg.

The Problem

When you sell a vertical spread (e.g., a put vertical), you have two legs:

- Short put (higher strike) — you sold this

- Long put (lower strike) — you bought this for protection

If you close part of the spread, your broker may split the trade into individual legs. If the short leg closed at a loss—even though the combined spread was profitable—the broker's system may flag it as a wash sale if you still hold other short puts at similar strikes.

Real Example: Partial Close of Put Verticals

- 1/5/2025: Buy 10 SPY $440/$435 put verticals (buy $440 put, sell $435 put) for $1.50 each

- 1/15/2025: Close 2 of 10 verticals for $2.00 each (profit: $0.50 × 2 = $100 total)

- Broker breakdown: Long $440 put gained $1.20, Short $435 put lost -$0.70

- Broker flags the short put leg (-$0.70 × 2 = -$140) as a wash sale because you still hold 8 identical short $435 puts

Why this happens:

Your broker doesn't track spreads as a single unit. It sees individual options. The short $435 put was closed at a loss, and you still hold 8 more short $435 puts that were opened within 30 days. The broker's automated system calls this a wash sale.

Is the broker correct?

Technically, yes—the IRS looks at individual securities, not spread combinations. The short put did close at a loss, and you hold substantially identical positions.

What actually happens to your taxes:

- The -$140 loss on the 2 short puts is disallowed

- That $140 is added to the basis of your remaining 8 short puts

- When you eventually close those 8 puts, the deferred loss will be recognized

- Net effect: Your total P&L stays the same; it's just a timing difference

How to avoid this:

- Close entire spread positions at once — don't leave orphan legs

- Close all contracts of the same spread simultaneously — don't partial-close

- Use Section 1256 instruments (SPX instead of SPY) where wash sales don't apply

- Wait 31 days between closing and reopening similar positions

- Keep records showing the spread was a single economic position (useful if you dispute a broker's classification)

Bottom Line: Avoiding Wash Sale Trap

Key takeaways:

-

Don't sell at a loss and buy back within 30 days

- The 30 days: Before loss sale and after

- Total: 61-day window

-

Put assignments count as purchases

- If assigned on 1/15 and you later sell at a loss on 1/20, the assignment is within 30 days before

- Don't buy back that stock within 30 days after 1/20

-

Buying calls/puts after a loss sale is risky

- Protective puts: Definitely risky (downside protection)

- Call options: Risky if they replace stock exposure

- Covered calls: Safer (you're not buying back exposure)

-

Use different securities to stay invested

- Sell SPY at a loss

- Wait 31 days

- Buy VTI or VOO (different S&P 500 ETFs)

- Not a wash sale (different securities)

-

Consider Section 1256 contracts

- SPX, RUT, NDX options are exempt from wash sale rules

- Also get favorable 60/40 tax treatment

- Switch from SPY to SPX options for tax-sensitive strategies

-

Know about Mark-to-Market election

- Section 475(f) eliminates wash sales for qualified traders

- Trade-off: All gains become ordinary income

- Consult a tax professional before electing

-

Watch out for broker wash sales on spread legs

- Brokers track individual options, not spread combinations

- Partial closes of verticals can trigger wash sales on losing legs

- Close entire spread positions at once when possible

-

Track wash sales on Form 8949

- Report disallowed loss

- Add to cost basis of new purchase

- This defers the loss until you sell the new position

-

Conservative rule: Wait 31 days after a loss

- If you're unsure, wait

- The tax savings aren't worth an audit

- You can always defer the loss to next year

-

For options traders: Monitor put assignments

- Assignment = purchase at strike price

- If you later sell at a loss, watch the 30-day window before and after assignment

Final Recommendation for Active Options Traders

If you trade options more than occasionally, wash sale compliance should be part of your regular workflow rather than an afterthought at tax time. The complexity of options—multiple expirations, rolling positions, spread adjustments, and assignment scenarios—means that automated broker reporting often captures only part of the picture. Your 1099-B may show wash sale adjustments that make sense mechanically but distort the economic reality of your spread trades.

The most practical approach is to maintain a simple log: date, underlying, action, and whether the action starts or ends a 61-day window. Review this log monthly, not annually. If you discover a potential wash sale before year-end, you can often adjust your positions to avoid permanent loss disallowance. If you only discover it when preparing your tax return, your options are limited.

For traders who consistently trigger wash sales through rolling and repositioning, the Section 475(f) mark-to-market election or a shift toward Section 1256 instruments (SPX, RUT, NDX) may be worth exploring with a tax professional. Both options eliminate wash sale complexity entirely, though each carries trade-offs that must be evaluated against your specific trading style and income situation.

Catch Wash Sale Risk Before Filing Season

Review trade sequences and assignment history while the context is still fresh, not when you are reconciling taxes months later.

The value of this guide is knowing what patterns create trouble. Days to Expiry helps you inspect those patterns inside your portfolio history so you can spot issues earlier and hand cleaner records to a tax professional.

Related Articles

Master the compliance side of options trading:

- The Wheel Options Strategy PDF Guide

- Fix IBKR 1099

- Wash Sale Calculator

- Complete Options Tax Guide – Full framework for understanding how options are taxed

- Covered Call Tax Rules – Specific rules for covered call writing and qualified vs. unqualified positions

- SPX Options Tax Treatment – Tax-advantaged trading with Section 1256 contracts exempt from wash sales

- Form 1099-B Walkthrough – How to read and reconcile your Interactive Brokers tax forms

- Options Tax Calculator – Estimate your tax bill before year-end

- Short Put Strategy Guide – Understanding assignment risk and timing

- Cash Secured Puts – Deep dive into put selling mechanics and assignment scenarios

- Option Assignment – What happens when your options get assigned and how to plan for it

Expertise: This guide was reviewed by a CPA specializing in active trader taxation and is updated for the 2024 tax year.

Download our free Options Trader Tax Checklist to avoid costly wash sale mistakes this year.

Frequently Asked Questions

Written by Days to Expiry Trading Team

The Days to Expiry trading team brings together experienced options traders and financial analysts dedicated to helping investors generate consistent income through proven options strategies.

Continue Your Journey

Covered Call Analyzer

Find the best covered call opportunities.

Cash-Secured Put Calculator

Calculate put selling returns.

Demo Portfolio

Explore a sample portfolio with positions and strategy insights — no login required.

Wheel Strategy Calculator

Plan your wheel trades.

Free trial

Start free — then keep the full workflow

- Multi‑stock covered call and cash‑secured put scans

- Strategy backtesting for covered calls and puts

- Full wheel backtesting with buy‑and‑hold comparison

- AI Portfolio Scanner for advanced recommendations