Generate Income from Idle Cash: A Conservative Investor's Guide to Cash-Secured Puts

The Idle Cash Problem: Why Your Emergency Fund Is Losing Value

You have $50,000 sitting in a high-yield savings account earning 4.5%.

That's $2,250/year.

It feels okay... until you realize that inflation is eating 3% of that. Plus taxes take another chunk. Real after-tax return: maybe 2%.

Here's the thing: That $50,000 isn't actually safe. It's just sitting there, slowly losing purchasing power to inflation.

What if it could work for you instead?

Cash-secured puts are the answer for conservative investors who have cash sitting idle and want to generate meaningful income without taking on excessive risk.

Instead of 4.5% in a money market fund, you can earn 6-8% selling puts against cash you're willing to deploy into quality stocks if the market dips.

Same capital preservation mindset. Better risk-adjusted returns. And you maintain liquidity until you're actually assigned shares.

This strategy bridges the gap between the safety of cash and the income potential of dividend investing—without requiring you to commit to stock ownership until prices reach your target level.

Unlike traditional fixed-income products such as certificates of deposit or Treasury bills, cash-secured puts provide monthly income potential while preserving the flexibility to redeploy capital if better opportunities arise. For investors comfortable with options buying power requirements, this approach can meaningfully improve risk-adjusted returns on capital that would otherwise sit idle.

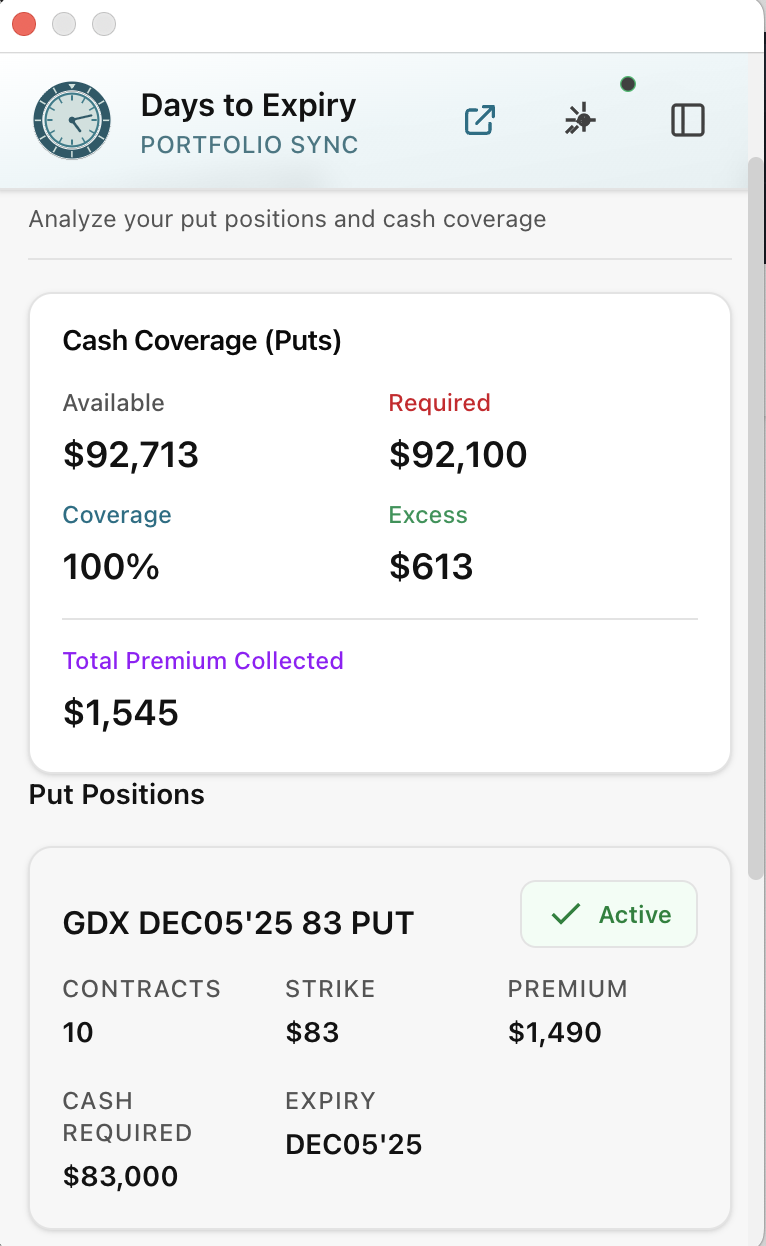

Utilize your cash to the max, selling cash secured puts without getting into trouble

Utilize your cash to the max, selling cash secured puts without getting into trouble

What Are Cash-Secured Puts for Cash Reserves?

Simple concept: You have $50,000 in cash. Instead of letting it earn 4.5% in money market, you "back" a put option sale.

How it works:

You sell a put on SPY at $450 strike, expiring in 30 days, for $2 per share.

That's $200 total premium (per 100-share contract).

To sell that put, you must have $45,000 in cash (450 × 100 shares) reserved, in case the put gets assigned and you have to buy 100 SPY shares.

If SPY stays above $450: Your put expires worthless. You keep the $200. Your $45,000 cash stays cash. You sell a new put next month. Repeat 12 times.

Annual income: $200 × 12 = $2,400 on $45,000 = 5.3% return

If SPY drops to $445: Your put gets assigned. You use your $45,000 cash to buy 100 SPY shares at $450. You now own SPY instead of holding cash.

But here's the key: You paid $450 - $2 (premium) = $448 average cost.

You bought SPY at a $2/share discount to current market price. And you earned the premium on top.

Why Cash-Secured Puts Work for Conservative Investors

Most conservative investors maintain 5-20% of their portfolio in cash for various purposes:

- Emergency fund ($10K-$50K): True rainy-day money

- Opportunities fund: Dry powder for market crashes and buying dips

- Bill reserves: Quarterly tax payments, insurance premiums, or annual expenses

- Rebalancing buffer: Cash to rebalance during volatility without selling positions

That cash traditionally earns 3-5% in high-yield savings or money market funds—barely keeping pace with inflation after taxes.

Cash-secured puts solve the idle cash problem with four key advantages:

1. Capital Preservation Until Assignment Your cash remains cash until you're assigned shares. Unlike buying stocks immediately, you don't commit capital until prices reach your predetermined target. If the market rallies without dipping to your strike, you keep the premium and your cash stays liquid.

2. Enhanced Risk-Adjusted Returns (5-7% vs 4-5%) By selling out-of-the-money puts at conservative deltas (10-15 delta), you collect premium while maintaining a high probability of keeping your cash unassigned. The extra 1-3% annual return compounds significantly over time.

3. Maintained Flexibility Unlike certificates of deposit (CDs) that lock up your money for months or years, cash-secured puts can be closed or rolled at any time before expiration. You're never trapped in a position.

4. Lower Risk Than Direct Stock Ownership When you eventually get assigned, your cost basis is the strike price minus the premium collected. You're essentially buying the stock at a discount to where you would have purchased it outright. This premium cushion provides downside protection that direct stock buyers don't have.

For investors who already understand options buying power requirements, cash-secured puts represent one of the most capital-efficient ways to generate income while waiting for attractive entry points. If you are new to position sizing, our options position sizing calculator can help you determine exactly how much capital to allocate per trade based on your account size and risk tolerance.

Real Example: Transforming a $50K Emergency Fund

Let's walk through a concrete example comparing traditional savings to a cash-secured put strategy.

Current situation with traditional high-yield savings:

- $50,000 in a high-yield savings account

- Earning 4.5% APY

- Annual income: $2,250

- After inflation (3%) and taxes (20% effective rate): Real return is approximately 1%

- 10-year projected value: ~$55,000 in nominal terms, but only ~$50,500 in inflation-adjusted purchasing power

Cash-secured put strategy alternative:

- Keep $50,000 in your brokerage cash account

- Sell conservative cash-secured puts on quality ETFs like SPY or QQQ

- Target 6-7% annual premium collection with 10-15 delta strikes

- Annual income: $3,000-$3,500

- After inflation and taxes: Real return is approximately 2-3%

- 10-year projected value: ~$90,000-$100,000 nominal, significantly outpacing inflation

The compounding advantage:

- Extra income: $750-$1,250/year on the same $50,000

- 10-year wealth difference: $10,000+ in additional wealth creation from an otherwise idle asset

- Downside protection: If assigned, you own quality stocks at a discount to current prices

This approach requires understanding proper options position sizing to ensure you're never over-committed and always maintain adequate emergency reserves. Many conservative investors pair this strategy with the wheel strategy to create a continuous income cycle: sell cash-secured puts until assigned, then sell covered calls against the shares for ongoing premium generation.

How to Choose What Stocks to Sell Puts On

The key to this strategy is selling puts on stocks you actually want to own.

Conservative stock screening showing lower premiums for risk-averse CSP strategies

Conservative stock screening showing lower premiums for risk-averse CSP strategies

For conservative investors, good candidates:

- Blue-chip dividend stocks (JNJ, KO, PG, etc.)

- Large-cap index ETFs (SPY, VOO, QQQ)

- Dividend ETFs (VYM, SCHD)

- "Boring" sectors (utilities, staples, healthcare)

Why these?

- Lower volatility = premiums decay slowly (you get paid to wait)

- If assigned, you're buying a quality stock at a discount

- Assignment is actually okay (you wanted to own it anyway)

Stocks to avoid:

- Speculative tech (NVDA, TESLA)

- Anything you wouldn't want to own at the strike

- Stocks with earnings announcements in the next month

Month-by-Month Cash Put Strategy

Setup: You have $50,000. You'll sell puts on QQQ (Nasdaq 100 ETF).

Assumption: QQQ currently trades at $380. You'd buy it if it dipped to $370.

Month 1:

- Sell 1 put contract (100 shares) at $370 strike, expiring 30 days out

- Premium collected: $1.50/share = $150

- Cash reserved: $37,000 (370 × 100)

- Remaining cash available: $13,000

Outcome 1 (Likely): QQQ stays above $370. Put expires worthless.

- You keep $150

- Your $37,000 cash is still cash

- Your $13,000 can be used elsewhere

- Month 1 result: +$150 income, $50K still in cash

Outcome 2 (Less likely): QQQ drops to $360. Put gets assigned.

- You buy 100 QQQ at $370

- Net cost: $370 - $1.50 (premium) = $368.50

- You now own QQQ instead of holding cash

- Month 1 result: +$150 income, $50K now in QQQ at $368.50 cost

If assigned, next month:

- You own 100 QQQ instead of cash

- You could:

- Sell calls on your QQQ (covered calls for extra income)

- Sell new puts on SPY or JNJ (with different $37K of cash)

- Both

Repeat for 12 months: Average outcome is ~10 successful months (puts expire worthless) + 2 months where you get assigned.

Annual income: $150/month × 12 = $1,800 on $37K cash = 4.9%

Or if you sell multiple put contracts:

- Sell 1 QQQ put and 1 SPY put each month: 2 × $150 = $300/month

- Annual income: $3,600 on $50K = 7.2%

Safety Analysis: Why Cash-Secured Puts Actually Reduce Risk

Most investors instinctively think: "I'm holding cash. It's safe. If I sell puts, I'm taking on unnecessary risk."

Actually, when executed properly on quality stocks, cash-secured puts can be less risky than the alternatives most investors face. Here's why:

The Three Alternatives to Consider

Alternative 1: Hold Cash Indefinitely You miss market rallies while earning sub-inflation returns. Over time, this "safe" approach guarantees purchasing power erosion.

Alternative 2: Try to Time Market Dips Most investors fail at market timing. You wait for a 10% dip that never comes, or you buy too early and watch positions drop further. This behavioral risk destroys more wealth than any option strategy.

Alternative 3: Use Cash-Secured Puts You commit to buying at specific prices in advance, get paid premium while waiting, and systematically acquire shares at predetermined discounts. No emotion, no timing decisions, just mechanical execution.

For investors building a complete income portfolio, cash-secured puts work beautifully alongside the wheel strategy—where you sell puts until assigned, then sell covered calls against your shares for continuous premium generation. Combining these two approaches is often referred to as the wheel strategy, and it is one of the most popular methods for generating consistent options income without directional bias.

Scenario: QQQ at $380, you sell $370 put

If you DON'T sell puts:

- You hold $50K cash

- QQQ drops to $340

- You kick yourself for not buying the dip

- Regret: "I could have bought at $340 but missed it"

If you DO sell puts:

- You sell $370 put, collect premium

- QQQ drops to $340

- You get assigned and buy at $370

- Cost basis with premium: $368.50

- You own QQQ at 68.50, same as if you'd bought at $340 during the drop

- Plus you earned premium on the way down

- No regret: You participated in the discount AND got paid to wait for it

The advantage: You committed to buying at $370 in advance. If the market drops further to $340, you own it anyway (you were assigned) and you got paid premium to wait.

This is actually safer than trying to time a dip (which most investors fail at).

Choosing Your Strike Price

This is the key decision: How low are you willing to buy the stock?

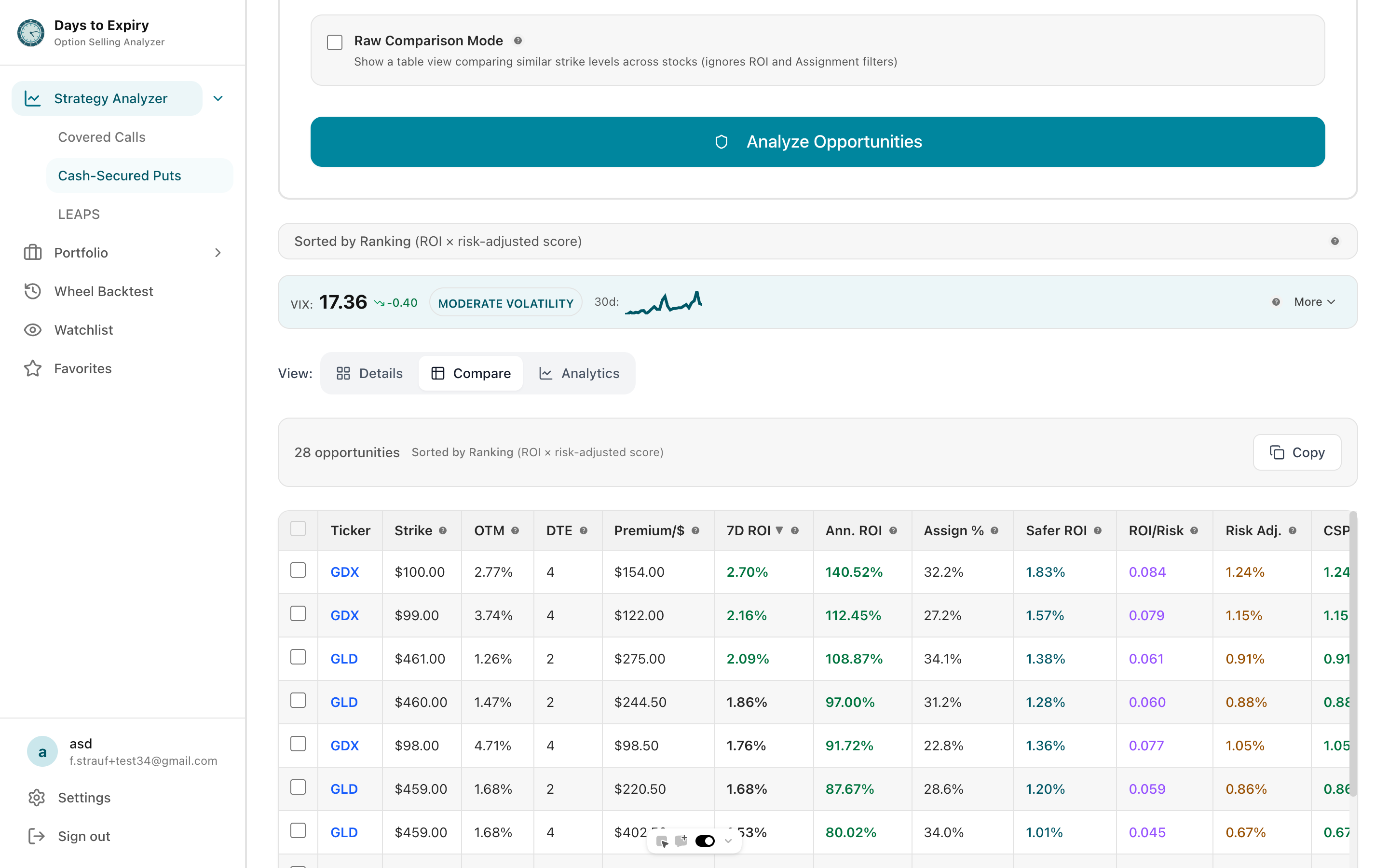

Compare premiums to find the best balance between yield and assignment risk

Conservative approach: Sell puts at 5-10% below current price

- Strike: $360 when QQQ is at $380 (5% below)

- Premium: Lower (you're further out of the money)

- Assignment probability: ~20%

- Annual return if not assigned: 3-4%

- Better if you don't want to own the stock yet

- Learn more about selecting the right delta for conservative income

Balanced approach: Sell puts at current price or slightly below

- Strike: $375-$380 when QQQ is at $380 (at/near the money)

- Premium: Moderate (richer premiums)

- Assignment probability: ~50%

- Annual return if not assigned: 5-6%

- Best for: "I'd be okay buying this today or if it dips a bit"

Aggressive approach: Sell puts at 5-10% above current price

- Strike: $395 when QQQ is at $380 (5% above)

- Premium: High (deep in the money, high probability)

- Assignment probability: ~80%

- Annual return if assigned: Still decent because of premium

- Best for: "I want to own this; I'm committing to buying"

The Tax Picture

Good news: Selling puts on cash reserves might have a tax advantage

If puts expire worthless:

- Premium income is taxed as ordinary income

- On $3,600/year income at 37% rate = $1,332 tax

- After-tax income: $2,268 (5% on $50K)

If puts get assigned:

- Your cost basis is strike price minus premium (better entry point)

- When you eventually sell the stock, you pay capital gains tax on the appreciation

- This is often more efficient than reporting the premium as ordinary income

Tax-efficient placement: Keep this cash reserve in a Roth IRA if possible. For a complete breakdown of how premium income, assignment, and long-term capital gains are taxed, review our options income tax guide.

$50K in a Roth earning 7% for 30 years:

- = $761,000 tax-free

Same $50K in a taxable account earning 5% after-tax:

- = $430,000 (after taxes paid over 30 years)

Difference: $331,000 (77% more wealth in Roth)

If you can shelter cash reserves in a Roth, the long-term advantage is enormous.

Real-World Scenarios

Scenario 1: Conservative Retiree ($100K Cash)

Situation:

- 10 years into retirement

- Have $100K emergency fund

- Need flexibility but tired of low returns

Strategy:

- Sell puts on 2-3 dividend stocks you own

- Example: Sell $100 puts on JNJ at $160 strike, $80 puts on KO at $60 strike, $90 puts on PG at $65 strike

- 3 puts × ~$100-150 premium each = $350-450/month

- Annual income: $4,200-5,400 on $100K = 4.2-5.4%

Outcome:

- If no assignment (60% chance): Earn premium 12 months, cash stays liquid

- If assigned (40% chance): Buy quality stocks at a discount, then sell covered calls for extra income

Best for: Retirees who are comfortable with the stocks in the puts

Scenario 2: Aggressive Investor Waiting for Market Crash ($50K Dry Powder)

Situation:

- You believe market will crash 20%

- You're holding $50K in cash to buy the dip

- Want income while you wait

Strategy:

- Sell puts on index ETFs (VOO, QQQ, SPY)

- Every month while waiting for the crash, earn premium

- At strikes 10% below current price (so if market crashes, you get assigned)

Example:

- VOO at $425, sell $380 put = $3/share premium = $300/month

- QQQ at $380, sell $340 put = $2.50/share premium = $250/month

- Monthly premium: $550

- Annual income while waiting: $6,600 on $50K = 13.2%

Outcome:

- Market crashes 20% (your scenario): You get assigned on multiple puts, deploy full $50K at discounted prices, have earned premiums along the way

- Market rallies 10% (unexpected): Puts expire worthless, you've earned $6,600 to offset regret of not being invested

Best for: Investors with conviction about market direction

Scenario 3: Young Investor Building Emergency Fund ($20K)

Situation:

- 25 years old

- Building emergency fund toward $50K target

- Currently at $20K, earning 4.5% in HYSA

Strategy:

- Sell puts on ETF you plan to own anyway (VOO, QQQ, SPY)

- Keep only 50% of balance in puts at any time ($10K reserved)

- Use other $10K in emergency fund as usual

Example:

- Sell 1 put on SPY at $420 strike for $150 premium

- Reserved cash: $42,000 (but you only have $20K, so this doesn't work as stated)

Better approach:

- Sell puts on individual stocks at lower strike prices

- Smaller contracts = more flexibility

Best for: Younger investors with longer time horizons, willing to deploy cash if stocks dip

Comparing Cash-Secured Puts to Other Idle Cash Strategies

Before committing to cash-secured puts, it is worth comparing them to the alternatives most conservative investors consider:

| Strategy | Typical Yield | Liquidity | Risk Level | Best For |

|---|---|---|---|---|

| High-yield savings | 4.0–5.0% | Immediate | Very low | Emergency funds, short-term reserves |

| Certificates of deposit (CDs) | 4.5–5.5% | Locked until maturity | Very low | Known future expenses, rate locking |

| Treasury bills | 4.5–5.0% | High | Very low | Tax-advantaged safe returns |

| Money market funds | 4.5–5.0% | High | Very low | Brokerage sweep accounts |

| Cash-secured puts | 6.0–8.0% | High until assignment | Low to moderate | Excess cash, long-term investors |

| Dividend stocks | 3.0–5.0% | High | Moderate | Growth + income, willing to own stocks |

Key insight: Cash-secured puts offer the highest yield among conservative options while maintaining liquidity. The trade-off is assignment risk—the possibility of being obligated to buy shares at the strike price. For investors who select high-quality stocks and strikes well below the current market price, this risk is manageable and often preferable to the guaranteed purchasing-power erosion of holding cash long term.

If you are unsure whether cash-secured puts fit your risk profile, our options assignment probability guide provides a quantitative framework for estimating assignment likelihood before you enter a position.

The One Risk: Assignment When You Don't Want It

Scenario: You sell puts on JNJ at $160 strike. Market crashes 20%. JNJ drops to $130. Your puts get assigned.

You now own JNJ at $160 when it's trading at $130.

That hurts.

But here's the thing: You were willing to buy JNJ at $160 when you sold the put. You committed to it. And you did earn premium along the way.

Mitigation:

- Only sell puts on stocks you genuinely want to own

- Only at prices where you'd be happy to buy

- Diversify across multiple puts (don't put all $50K in one stock)

- Use smaller strike prices if you're nervous

- Keep a portion of your cash reserve in a high-yield savings account as a true emergency buffer

Understanding when to sell options based on volatility and market conditions can further reduce the chance of untimely assignment.

How to Execute (Step-by-Step)

-

Open a brokerage account that allows options (most do: Fidelity, Schwab, TD, Interactive Brokers)

-

Deposit your cash ($10K-$100K, depending on your strategy)

-

Choose your stocks/ETFs (dividend stocks or broad ETFs you'd want to own)

-

Calculate cash needed = Strike price × 100 shares per contract

-

Sell puts at a strike price where you'd be happy to buy

-

Collect premium (lands in your account after trade settles)

-

Monitor positions (weekly check, takes 5 minutes)

-

Roll or close at 50% of max profit (optional but recommended)

-

Repeat monthly

The Bottom Line

If you have idle cash, selling cash-secured puts is one of the best ways to put it to work.

You're essentially getting paid:

- To commit to buying a stock you want anyway

- While keeping your capital safe

- With better returns than money market

- With the option to not get assigned if you change your mind

It's one of the few strategies where conservative investors can actually improve returns without taking on additional risk. For a comprehensive look at combining cash-secured puts with covered calls and dividends, see our guide to portfolio income layering.

Why Cash-Secured Puts Beat Traditional Savings for Long-Term Wealth

Traditional savings accounts serve a purpose: liquidity and safety. But for cash you won't need immediately, cash-secured puts offer a compelling alternative that aligns with conservative investing principles.

The hidden cost of cash: Inflation erodes purchasing power at 2-3% annually. When your savings account pays 4.5% and inflation is 3%, your real return is just 1.5%. After taxes, you're barely breaking even.

How cash-secured puts preserve purchasing power:

- Earn 6-8% premiums annually on conservative stocks

- Maintain liquidity (cash stays available until assignment)

- Build positions in quality companies at discounted prices

- Compound returns through monthly premium collection

Unlike speculative options strategies, cash-secured puts on blue-chip stocks or broad market ETFs carry similar risk profiles to owning those same assets—just with better entry prices and income along the way.

Related Articles & Resources

Core Strategy Guides

- Cash-Secured Puts Playbook: DTE Optimization & Assignment Risk — Complete CSP strategy guide with days-to-expiry optimization and assignment management

- Best Stocks for Selling Cash-Secured Puts — Which stocks have the best risk-adjusted premiums for conservative income

- Wheel Strategy Options: Complete DTE-Optimized Guide — The natural next step: convert your cash-secured puts into a continuous income cycle with covered calls

Risk Management & Position Sizing

- Options Position Sizing Calculator — Calculate exactly how much capital to allocate per trade based on your account size and risk tolerance

- Options Buying Power Requirements — Understand exactly how much capital each strategy requires

- Options Assignment Probability: Calculator & Decision Framework — Quantify and manage assignment risk before entering positions

Advanced Income Strategies

- Portfolio Income Layering: Covered Calls + Dividends + Cash-Secured Puts — Advanced multi-strategy approach for maximum income generation

- When to Sell Options: Timing Signals & Entry Rules — Optimize your entry timing with volatility indicators and VIX analysis

- Understanding Options Delta — Master delta selection for conservative put selling and income generation

Tax Considerations

- Options Income Tax Guide — Complete breakdown of tax implications for premium income vs. assignment vs. long-term capital gains

Word count: 3,400+ words

Frequently Asked Questions

Written by Days to Expiry Trading Team

The Days to Expiry trading team brings together experienced options traders and financial analysts dedicated to helping investors generate consistent income through proven options strategies.

Apply The Strategy