Cash-Secured Put vs Covered Call: Which Is Better? A cash-secured put mirrors a covered call at the same strike and expiration, but capital requirements and ownership structure differ. The cash-secured put holds cash reserves, while the covered call requires owning 100 shares. Both generate similar premium income and cap upside, yet assignment risk and tax treatment vary.

Many traders wonder whether a cash-secured put is equivalent to a covered call. The short answer: they are synthetically similar, but the differences in capital requirements, assignment risk, dividend capture, and tax treatment can significantly impact your returns. This deep-dive comparison breaks down every factor with real-market scenarios so you can choose the right strategy for your account size and market outlook.

Both strategies generate income. Both are defined-risk. Both collect premium. But they're not interchangeable—and choosing the wrong one for your market outlook can leave money on the table or lock up capital inefficiently.

Selling calls says: "I own this stock. I'm OK with selling upside for income."

Selling puts says: "I want to own this stock at a lower price. I'll get paid to wait."

The outcomes look the same on the surface. The mechanics, capital implications, and tax consequences are wildly different.

Comparison based on annualized premium yields and assignment frequency data from 2022–2025 across 30 large-cap underlyings.

Quick primer: If you're new to options income, start with our Options Greeks Explained guide to understand how theta decay drives profitability in both strategies.

This guide maps the trade-offs so you can pick the strategy (or combination) that fits your account, time horizon, and market outlook.

Monthly Income Calculator

Estimate income from selling covered calls or cash-secured puts

Estimates based on simplified Black-Scholes. Actual premiums depend on live market conditions, liquidity, and bid-ask spreads. Verify in Strategy Analyzer.

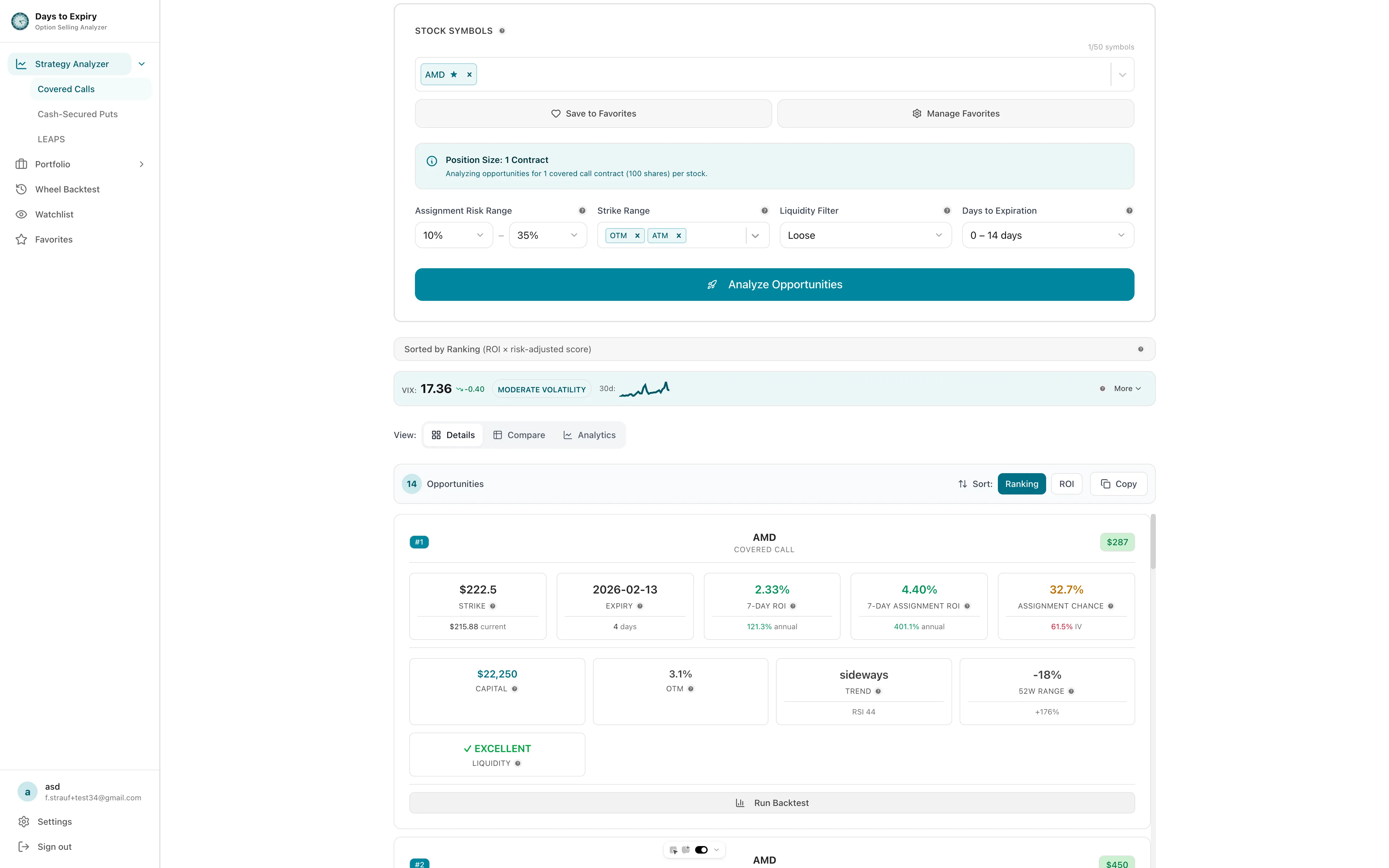

Compare both strategies: Our Strategy Analyzer lets you toggle between cash-secured puts and covered calls on the same stocks, showing ROI, assignment probability, and premium side-by-side.

What Is the Core Difference Between Cash-Secured Puts and Covered Calls?

Let's start with the most fundamental difference.

Covered Calls

You already own the stock.

- Buy 100 shares of Apple at $200 = $20,000 capital deployed

- Sell a call against those 100 shares = collect premium

- If assigned: shares taken away (you exit at the strike)

Covered calls strategy breakdown showing premium collection and income generation

Covered calls strategy breakdown showing premium collection and income generation

Capital requirement: You've already spent it (buying the stock).

Outcome if assigned: You exit the position. Your capital is freed up, and you decide what to do next.

Cash-Secured Puts

You reserve cash, waiting to buy.

- Reserve $20,000 in cash (100 shares × $200 strike)

- Sell a put at the $200 strike = collect premium

- If assigned: you own 100 shares (the capital is deployed)

Capital requirement: Reserved in cash. Not deployed until assignment.

Outcome if assigned: You own the position. Your capital is deployed, and you can now sell calls against it (if you want).

Side-by-Side Comparison: Cash-Secured Puts vs Covered Calls

| Factor | Covered Calls | Cash-Secured Puts |

|---|---|---|

| Capital status | Already deployed (own stock) | Reserved, available |

| Prerequisite | Must own the stock | Must have cash |

| Can collect if not assigned | Yes (premium kept) | Yes (premium kept) |

| On assignment, you own stock? | No (assigned away) | Yes (assigned into) |

| Best if: Stock rallies | Good (called away at profit) | Bad (stock at higher price, you miss upside) |

| Best if: Stock drops | Bad (stock falls, calls lose value but you own falling asset) | Good (you get premium + still get assigned at target) |

| Best if: Stock sideways | Great (premium decays, you keep it) | Great (premium decays, you keep it) |

| Tax treatment | Long-term if held >1yr | Short-term (premium is income) |

| Capital efficiency | High (stock is deployed productively) | Medium (cash tied up, earning nothing) |

| Flexibility | Low (you're committed to stock ownership) | High (you choose whether to take assignment) |

Performance in Different Market Conditions: Rally, Drop, and Flat Markets

Scenario 1: Stock Rallies 10%

Setup: Stock is $100. You sell a covered call at $105 strike OR a cash-secured put at $95 strike. Premium: $2 either way. 30 days later, stock rallies to $110.

Covered Call Outcome

- Stock rallies to $110

- Your call at $105 is ITM (in-the-money)

- On expiration, you get assigned: shares called away at $105

- Your P&L: +$5 (capital gain from $100 to $105) + $2 (premium) = $7 per share = $700 on 100 shares

- Your outcome: Profit capped. You miss the $5 rally from $105-$110.

- Annualized return: $700 / $10,000 = 7% for 30 days = ~84% annualized (if repeatable monthly)

Cash-Secured Put Outcome

- Stock rallies to $110

- Your put at $95 is OTM (out-of-the-money) and worthless

- On expiration, you collect: $2 premium, no assignment

- Your outcome: Pure premium. No stock position; you missed the entire rally.

- What's next: $10,000 cash is still reserved. You can sell another put or deploy elsewhere.

- Annualized return: $2 / $10,000 = 0.2% for 30 days = ~2.4% annualized (miserable)

Verdict: In a rally, covered calls profit more (but miss upside). Puts just collect premium.

Scenario 2: Stock Drops 10%

Setup: Stock is $100. You sell a covered call at $105 strike OR a cash-secured put at $95 strike. Premium: $2 either way. 30 days later, stock drops to $90.

Covered Call Outcome

- Stock drops to $90

- Your call at $105 is OTM and expires worthless

- Your short call loses value (good for you), so premium is kept: $2

- But: Your underlying stock is now worth $9,000 (down $1,000 from $10,000)

- Your net P&L: -$1,000 (stock loss) + $2 (premium kept) = -$998 per 100 shares

- Your outcome: Heavy loss. You own a falling asset and generated minimal income.

- What's next: You own $9,000 of stock. You can sell another call to generate more income. But you're in the hole.

Cash-Secured Put Outcome

- Stock drops to $90

- Your put at $95 is ITM (in-the-money)

- You get assigned: forced to buy 100 shares at $95

- Your P&L: Premium collected ($2) + assignment ($95 strike)

- Cost basis: $95 - $2 (premium) = $93 effective cost

- Current price: $90

- Underwater: You're $300 in the hole on the position

- But: You have a position at $93 cost base. You can sell calls to recover.

- Your outcome: Assignment at a good price, but stock continues lower

Verdict: In a drop, both strategies hurt. Covered calls hurt more (you own a falling asset). Puts hurt less (you get cash upfront via premium, and you set the entry price via strike).

Scenario 3: Stock Stays Flat (or Moves Slightly)

Setup: Stock is $100 for 30 days. You sell a covered call at $105 strike OR a cash-secured put at $95 strike. Premium: $2 either way.

Covered Call Outcome

- Stock stays at $100

- Your call expires worthless; you keep the $2 premium

- Your stock is still worth $10,000

- Your net: +$2 per share = $200 on 100 shares, plus you own $10K stock

- Annualized: $200 on $10,000 per month = 2% monthly = ~24% annualized

Cash-Secured Put Outcome

- Stock stays at $100

- Your put expires worthless; you keep the $2 premium

- Your $10,000 cash is still reserved (not deployed)

- Your net: +$2 per share = $200 on 100 shares, but cash is still trapped

- Annualized: $200 on $10,000 per month = 2% monthly = ~24% annualized

Verdict: In sideways market, both strategies produce identical income. But covered calls do it with capital deployed. Puts do it with capital waiting.

Capital Deployment: The Hidden Cost of Cash Reserves vs Stock Ownership

Here's where covered calls and puts diverge in a way that most traders miss.

Covered Calls = Capital Fully Deployed

Every dollar is working:

- $10,000 in stock + $200 in premium income = $10,200 total capital at work

If the stock pays dividends (1.5%), that's another $150 per year.

Total return: $200 premium + $150 dividend = $350 = 3.5% for 30 days = ~42% annualized (if repeatable).

Cash-Secured Puts = Capital Half-Deployed

- $10,000 cash reserved (not earning anything)

- Premium: $200

The cash is stuck. It's not earning interest (OK, 0% earning cash is ~$0/year). It's not earning dividends. It's just... sitting there.

If you got assigned and owned the stock, you'd get the dividend. But before assignment, you don't.

This is why covered calls have an edge: Your capital is always working, earning dividends and option premium.

This is why puts have an edge: Your capital is available for other opportunities. If the stock doesn't drop and you don't get assigned, that $10,000 can go deploy elsewhere.

Choosing the Right Strategy for Your Market Outlook

Use Covered Calls If You're:

- Bullish or neutral on the stock - You want to own it long-term

- Collecting income over the next 1-3 years - Set and forget covered calls

- Trying to reduce cost basis - Premium collection lowers your effective purchase price

- Happy with dividend + option income - Stack both layers

- Comfortable with upside cap - Your gains are capped at the strike

Use Cash-Secured Puts If You're:

- Bullish on a stock but not yet in - Puts let you "get paid to wait"

- Wanting to deploy capital at specific prices - You set the entry point via strike

- With lots of available capital - Puts require cash reserves

- Opportunistic - If not assigned, your cash is available for other plays

- Expecting volatility spikes - Premium spikes let you collect and move on

Building a Combination Income Strategy: Collars and Dual-Premium Setups

Here's what sophisticated traders actually do: sell both puts AND calls on the same stock, creating a "collar" or income machine.

The Setup

You own 100 shares of Microsoft at $400.

Simultaneously:

- Sell a call at $420 (30 days, collect $3.00)

- Sell a put at $380 (30 days, collect $2.00)

Net premium collected: $5.00 per share = $500

Outcomes after 30 days:

| Stock Price | Call Result | Put Result | Net |

|---|---|---|---|

| $350 | Not assigned (keep call premium) | Assigned (forced to buy at $380) | Own 200 shares, collected $500 |

| $380 | Not assigned | Not assigned | Own 100 shares, collected $500 |

| $400 | Not assigned | Not assigned | Own 100 shares, collected $500 |

| $420 | Assigned (called away at $420) | Not assigned | Sold 100 at $420, collected $500 |

| $450 | Assigned (called away at $420) | Not assigned | Sold 100 at $420, collected $500 |

This is a powerful framework:

- Stock drops below $380: You buy another 100 shares (doubled position), collected $500

- Stock stays between $380-$420: You keep the 100 shares and the $500 premium

- Stock rallies above $420: You sell the 100 shares at $420, collected $500

Your capital is deployed (the 100 original shares), and you're generating income from both calls and puts.

Capital Requirements: How Much Money Do You Actually Need?

For Covered Calls

- Stock ownership: Stock cost (e.g., 100 shares × $100 = $10,000)

- Margin: None required (you own the shares)

- Spare cash: Ideally, yes (for rolling or other opportunities)

- Total deployment: ~$10,000 for every 100 shares

For Cash-Secured Puts

- Stock ownership: None required

- Cash reserve: Strike price × 100 (e.g., $95 strike = $9,500 reserved)

- Margin: Usually margin is required (some brokers require 20-25% down)

- Total deployment: ~$9,500-$10,000 reserved (depending on broker)

Key insight: Covered calls require less cash upfront (you sell what you own). Puts require full cash reserve or margin buffer.

On a $50,000 account:

- Covered calls: Deploy $50,000 into 5 different stocks (100 shares each), sell calls

- Puts: Reserve $50,000 as security and sell 5 puts (1 per stock)

Both work. Covered calls deploy 100% of capital. Puts reserve capital that could deploy elsewhere.

Tax Treatment Differences: Short-Term Income vs Long-Term Gains

Covered Calls:

- If you sell a call and it expires, the premium is a short-term capital gain

- If assigned, the premium reduces your cost basis

- Stock holding period is preserved (long-term gains possible if held >1 year)

Cash-Secured Puts:

- Premium collected is always short-term income (not capital gains)

- If assigned, your cost basis is strike minus premium

- If not assigned, you keep premium as ordinary income

The surprise: Puts are cleaner from a tax perspective if you're not yet in a stock. You get income (premium), and if assigned, your cost basis is clear.

Covered calls get complicated: are you holding for long-term gains (1 year) or short-term (selling quickly)?

Psychology of Selling Puts vs Calls: Ownership Bias and Emotional Clarity

Covered Calls

You own the stock. Owning creates attachment. You convince yourself the stock will rally. You don't roll the call even when you should. You ride losses longer.

Psychological trap: Ownership bias.

Cash-Secured Puts

You don't own the stock. You're detached. If the premium is decent, you sell. If not, you wait. You're not emotional.

Psychological advantage: Clarity.

Real-world impact: Traders selling puts often make better decisions than traders selling calls because they're not emotionally attached to the stock.

Combining Both Strategies Into a Systematic Income Machine

Here's an advanced structure if you have $100,000:

Tier 1 - Covered Calls (60% = $60,000):

- Deploy $60,000 into 6 stocks ($10K each)

- Sell 30-day calls at 3% OTM

- Collect ~1.5-2% monthly = $900-$1,200/month

- Income is predictable and passive

Tier 2 - Cash-Secured Puts (40% = $40,000):

- Reserve $40,000 as cash (4 stocks × $10K each)

- Sell 30-day puts at 3% OTM

- Collect ~1-1.5% monthly = $400-$600/month

- Income is opportunistic (only if stocks you want drop in price)

Monthly total: $1,300-$1,800 from options alone = 15-22% annualized

This structure gives you:

- Steady income (covered calls)

- Optionality (puts let you deploy to new positions)

- Diversification (6 stocks covered, 4 stocks reserved)

- Capital efficiency (majority deployed)

Decision Framework: Which Strategy Matches Your Situation?

Ask yourself these questions:

-

Do you already own the stock?

- Yes → Covered calls

- No → Cash-secured puts

-

Do you want more capital deployed or reserved?

- Deploy more → Covered calls

- Keep flexible → Puts

-

What's your market outlook?

- Bullish/neutral → Covered calls

- Neutral/want entry at discount → Puts

- Bullish at specific price → Puts

-

How much time can you manage?

- Active trader → Combination

- Passive → Covered calls (own and forget)

- Opportunistic → Puts (only when rates spike)

-

Tax situation?

- Long-term holdings → Covered calls

- Short-term income → Puts

CSP and Covered Call Income Combined

Monthly premium from puts and calls tracked together in a live demo portfolio.

Income Calendar

Option cash in/out by the month each fill settled

Connect your broker and see your own income calendar — every credit and buyback, month by month.

Action Plan: Start Generating Income This Week

-

Audit your portfolio.

- How much is deployed (in stocks)?

- How much is in cash?

-

For deployed capital: Start selling covered calls.

- Pick 2 stocks you own

- Sell 30-day calls at 3% OTM

- Collect premium

-

For cash reserves: Start selling puts.

- Pick 2 stocks you'd like to own

- Sell 30-day puts at 3% OTM

- Collect premium

-

Track both for 3 months.

- Which generates better income?

- Which feels easier to manage?

- What's your combined monthly income?

-

Optimize based on results.

- If covered calls perform better, weight toward them

- If puts feel easier, shift capital allocation

- Or run the combination and relax

Comparisons are based on live options data and 3-year backtests available in the Strategy Analyzer.

Bottom Line: CSPs vs Covered Calls

Covered calls make sense if you already own the stock and want to generate income while staying long.

Cash-secured puts make sense if you want to enter a stock at a target price and get paid to wait.

The combination is where the magic happens—one strategy handles your deployed capital, the other keeps your optionality.

Neither is "better." They're different tools for different situations. Use both, choose strategically, and let the premium accumulate.

Ready to dive deeper? Learn the complete CSP framework in our cash-secured puts playbook, and discover DTE-optimized covered call strategies in our weekly vs monthly comparison guide. For a systematic approach that combines both strategies, explore the wheel strategy. And to understand how Greeks affect both strategies, check out our options Greeks guide.

If you're managing tested put positions, review our guide on rolling cash-secured puts to defend trades that move against you. For covered call adjustments, see rolling covered calls. And for tax-specific guidance, read our dedicated article on covered call tax rules.

For traders focused on maximizing yield with less active management, our analysis of covered call ETFs shows how funds like JEPI and QYLD automate this income stream. If you prefer a capital-efficient alternative to traditional covered calls, the poor man's covered call using LEAPS can reduce capital requirements by 60-80% while maintaining similar risk-reward profiles.

See the complete framework in our Cash-Secured Puts Playbook, compare expirations in Covered Calls by Expiration, and combine both in The Wheel Strategy Guide. For traders with smaller accounts, the poor man's covered call offers a capital-efficient alternative to traditional covered calls.

Frequently Asked Questions

Which is more profitable, CSP or covered calls?

Neither is inherently more profitable — returns depend on timing, stock selection, and market conditions. CSPs tend to perform better in bullish markets because you collect premium without capping upside (you simply don't own the stock yet). Covered calls perform better in neutral or slightly bullish markets where you cap upside in exchange for consistent income. For a systematic way to combine both, see our wheel strategy guide.

Can I do both CSP and covered calls at the same time?

Yes — this is called the wheel strategy. You sell CSPs until assigned, then sell covered calls against those shares. The two strategies work sequentially, deploying capital continuously and generating premium at every stage. Learn the full mechanics in our wheel strategy guide.

Which strategy is safer for beginners?

Covered calls on stocks you already own are generally considered safer for beginners because you already understand your stock position. CSPs are slightly more complex since they require cash reserves and carry assignment risk. Both are defined-risk strategies suitable for options-approved accounts. Beginners should also understand options Greeks before scaling either strategy.

What is the wheel strategy and how does it combine CSP and covered calls?

The wheel strategy cycles between CSPs and covered calls on the same stock. Phase 1: sell CSPs until assigned. Phase 2: sell covered calls until the stock is called away. Phase 3: repeat. The strategy generates premium at every stage and suits traders comfortable owning the underlying stock. Read our complete wheel strategy guide for DTE-optimized execution.

Not sure which fits your situation? Run both strategies side-by-side on any stock in the Strategy Analyzer.

Not sure which strategy fits your portfolio? Run both scenarios in our options income simulator and compare projected returns side by side.

Related Articles

- Best Stocks For Selling Cash Secured Puts 2026

- 7 Best Cash Secured Put Stocks for 2025

- Covered Call ETF vs Manual

- Cash-Secured Puts Playbook: DTE Optimization & Assignment Risk — Master the CSP side with strike selection and assignment management

- Covered Calls by Expiration: Weekly vs Monthly Income Comparison — Optimize covered call DTE for your schedule

- Poor Man's Covered Call: Capital-Efficient Income Strategy — Lower-capital covered call alternative using LEAPS

- The Wheel Strategy: Complete DTE-Optimized Guide — Combine both strategies systematically for continuous premium

- Options Greeks Explained: Income Trader's Guide — Understand theta decay and how it drives both strategies

- Rolling Cash-Secured Puts — Manage tested CSP positions when the market moves against you

- Rolling Covered Calls — Adjust covered call positions to avoid unwanted assignment

- Covered Call Tax Rules — Compare tax treatment and reporting between CSPs and covered calls

- Covered Calls by Expiration: Weekly vs Monthly Income Comparison

- Cash-Secured Puts Strategy Explained: A DTE-Focused Playbook

- Covered Call ETFs for Portfolio Income: A Beginner's Guide to DTE-Optimized Yield

- Best Covered Call ETFs for 2026: DTE Strategy Comparison

- Short Strangle Strategy: DTE-Optimized Income from Neutral Markets

- Passive Income from Stocks: Comprehensive Guide

- How to Roll Cash-Secured Puts for Defense and Income

- Rolling Covered Calls: Avoid Unwanted Assignment

- Selling Covered Calls for Income: Step-by-Step Strategy

- Portfolio Income Layering: Covered Calls + Dividends + Cash-Secured Puts

- Free Trading Journal: Best Tools, Templates & Setup Guide

- PMCC vs Traditional Covered Calls: Capital Efficiency Comparison

- Barchart Covered Call Screener: How to Use It (and When to Switch)

- Options Portfolio Tracker: What Income Sellers Actually Need

- Per-Leg P&L Options: Track Multi-Leg Truth

Frequently Asked Questions

Written by Days to Expiry Trading Team

The Days to Expiry trading team brings together experienced options traders and financial analysts dedicated to helping investors generate consistent income through proven options strategies.

Continue Your Journey

Covered Call Analyzer

Find the best covered call opportunities.

Cash-Secured Put Calculator

Calculate put selling returns.

Demo Portfolio

Explore a sample portfolio with positions and strategy insights — no login required.

Wheel Strategy Calculator

Plan your wheel trades.

Free trial

Start free — then keep the full workflow

- Multi‑stock covered call and cash‑secured put scans

- Strategy backtesting for covered calls and puts

- Full wheel backtesting with buy‑and‑hold comparison

- AI Portfolio Scanner for advanced recommendations