Selling Options for Income: The Complete Strategy Guide (2026)

Selling options for income is one of the most reliable ways to generate consistent cash flow in the markets—but only if you match the right strategy to your capital, risk tolerance, and time commitment. Unlike buying options, where you pay premium and hope for a directional move, selling options flips the script: you collect premium upfront and profit when the underlying stock stays within an expected range. This guide is the hub for every major income strategy on this site: it explains how each one works, when to deploy it, and how days-to-expiry (DTE) timing changes the math.

You'll move from beginner-friendly covered calls and cash-secured puts through defined-risk credit spreads, iron condors, and short strangles, then on to capital-efficient structures like the wheel and the poor man's covered call. Whether you have $5,000 or $500,000, there is a strategy here that fits your account—and a risk-management framework to protect it.

What you'll learn:

- How covered calls and cash-secured puts form the foundation of options income

- When to use credit spreads, iron condors, and short strangles for defined-risk trades

- How the wheel strategy compounds premium by cycling through puts and calls

- Why DTE selection (14, 30, or 45 days) dramatically affects your risk and return

- How to layer multiple strategies into a diversified income portfolio

By the end of this guide, you'll have a clear framework for matching any market condition to the right income strategy—and the risk-management rules to protect your capital along the way.

The Hard Truth About "Fast Money"

The allure of fast money is everywhere—social media, forums, and late-night ads promising overnight riches. For retail traders, the reality is different. Most "quick cash" schemes carry hidden risks that can wipe out accounts faster than they grow them. The strategies in this guide are not get-rich-quick schemes; they are systematic approaches that require patience, discipline, and proper risk management. Understanding this distinction is the first step toward sustainable income generation.

The Core Principle: You Get Paid to Wait

When you buy an option, you pay a premium upfront and hope the stock moves your direction before expiration. When you sell an option, you collect that premium upfront and hope the stock doesn't move against you dramatically.

Key advantage: Time decay (theta) automatically works in your favor. Every day that passes, the option you sold loses value—meaning your profit increases if the underlying price stays stable.

Key risk: Your profit is capped (you keep the premium), but your loss is potentially unlimited (for some strategies). That's why position sizing and risk management are non-negotiable.

Think of it this way: when you sell an option, you become the insurance company. Over a full market cycle, the majority of options expire worthless—which means sellers keep the premium. But that edge comes with responsibility: selling options requires more capital, stricter risk management, and a willingness to accept capped gains in exchange for higher-probability outcomes. It's a business, not a lottery ticket.

Speed vs. Safety Trade-off

Every options income strategy occupies a different point on the speed-versus-safety spectrum, and understanding where each sits helps you match a tactic to your current market outlook and risk tolerance. At the conservative end, covered calls and cash-secured puts generate modest but reliable premium over multi-week cycles; they rarely produce explosive returns, but they also rarely blow up an account. Moving toward the center, put credit spreads and iron condors accelerate income by compressing time and volatility, yet they demand precise strike selection and quick management when price breaks the expected range. At the aggressive end, short strangles and naked puts offer the fastest theta decay and highest premium relative to capital, but they carry assignment risk and undefined or lightly defined losses that can erase months of gains in a single gap-down session. The practical rule is to allocate the bulk of your capital to slower, safer strategies and reserve a small portion for faster setups only when implied volatility is elevated and you have time to monitor positions intraday.

Risk-adjusted perspective: A covered call on a blue-chip stock might generate 1–2% per month with minimal stress, while a short strangle on a volatile name might generate 3–5% but require constant monitoring and rolling. Over a full year, the "boring" strategy often wins because it avoids the occasional catastrophic loss that wipes out months of aggressive gains. Compounding works best when drawdowns are shallow and infrequent.

Strategy 1: Covered Calls – The Simplest Income Play

What It Is

You own 100 shares of a stock. You sell one call option against those shares. If the stock gets called away, you sell your shares at the strike price. If it doesn't, you keep the shares and the premium.

The math:

- Own 100 shares of XYZ at $50

- Sell one 55-strike call for $2 premium = $200 income

- If XYZ stays below $55: You keep shares + $200

- If XYZ rises above $55: Shares are called away at $55/share (your shares sell automatically)

When to Use It

- You own a stock but don't expect explosive upside

- You want steady income without worrying about directional bets

- You have capital tied up and want a "bonus" on your existing holdings

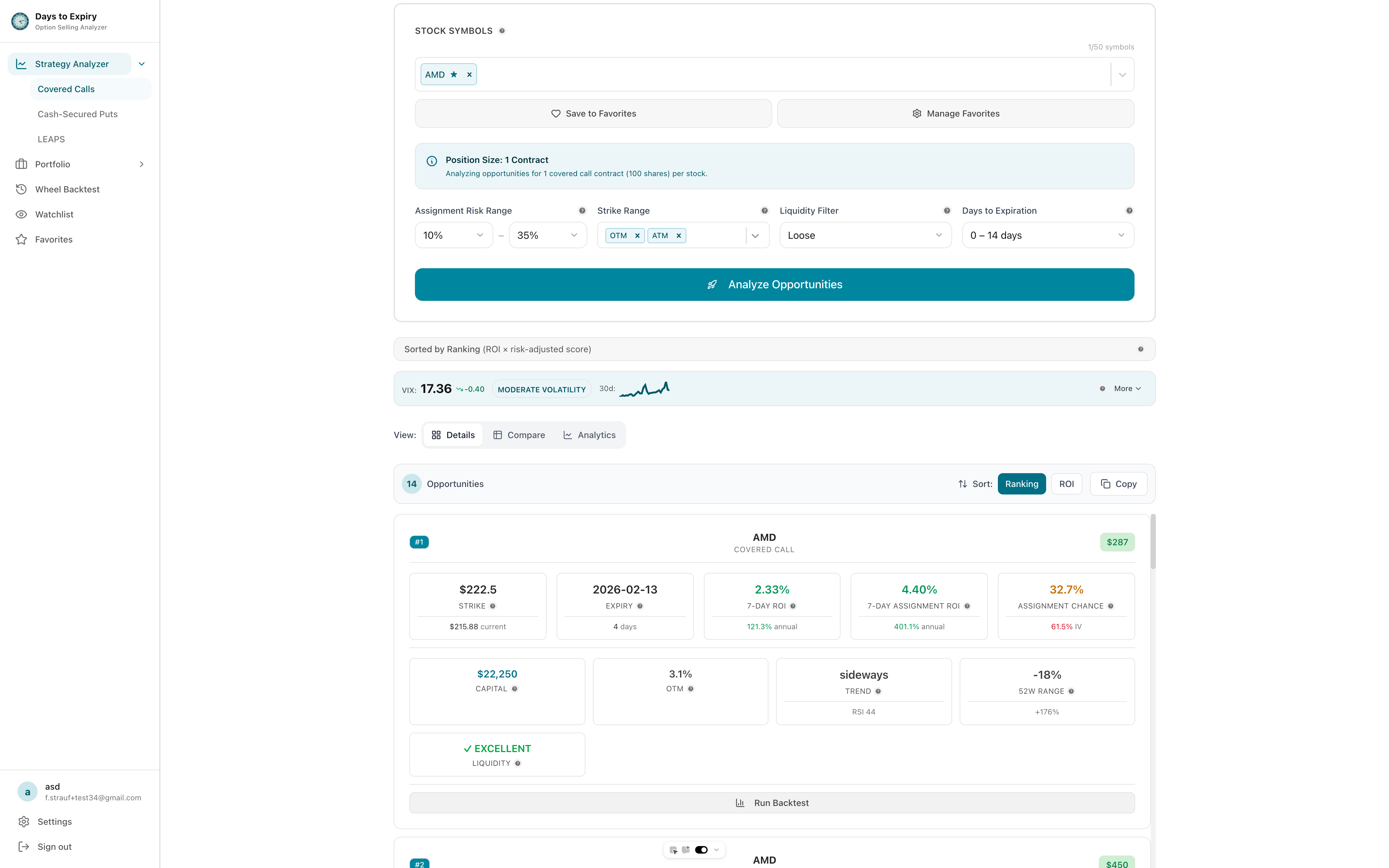

Covered calls strategy breakdown showing premium collection and income generation

Covered calls strategy breakdown showing premium collection and income generation

Learn more: View in Strategy Analyzer

Monthly Income Calculator

Estimate income from selling covered calls or cash-secured puts

Need more capital to start

Try $52,000 or switch strategies

The DTE Factor

Covered calls benefit enormously from theta decay optimization. Selling weeklies (7 DTE) accelerates income if you're willing to manage assignments more frequently. Monthlies (30 DTE) are more hands-off. Both work—it's about your preference.

Deep dive: Covered Calls by Expiration: Weekly vs Monthly Comparison

Income-focused guide: Selling Covered Calls for Income: Step-by-Step Strategy

Dividend Capture + Covered Calls: Double-Income Layering

This hybrid approach layers quarterly dividend payments on top of covered call premiums, creating two separate income streams from the same position. Instead of selecting any blue-chip stock, you deliberately choose dividend aristocrats or ETFs with consistent payout histories, then sell slightly out-of-the-money calls against those shares right after the ex-dividend date. If the stock remains below the call strike through expiration, you keep both the dividend and the premium; if the shares are called away, you still capture the dividend, the premium, and any appreciation up to the strike.

Timing matters: If the call is in-the-money close to the ex-dividend date, the option holder may exercise early to capture the dividend. Most traders either sell the call further out-of-the-money during the dividend window or use a lower-delta call to reduce assignment risk.

Why it matters: In a low-yield environment, the dividend-plus-premium combination can push annualized returns above 15% on stable names like Johnson & Johnson or Schwab U.S. Dividend Equity ETF (SCHD), with significantly less volatility than growth stocks. The trade-off is capital intensity: you need enough cash to hold 100-share lots, and you must track ex-dividend dates carefully to avoid early assignment surprises.

Related: Selling Covered Calls on Dividend Stocks: Double-Income Strategy

Strategy 2: Cash-Secured Puts – Deploy Idle Cash

What It Is

You have cash sitting in your account. You sell a put option backed by that cash. If assigned, you buy 100 shares at the strike price. If not assigned, you keep the premium and your cash.

The math:

- Reserve $5,000 cash

- Sell one 50-strike put on a $50 stock for $1.50 premium = $150 income

- If stock stays above $50: You keep cash + $150

- If stock falls below $50: You're forced to buy 100 shares at $50 (costing your $5,000)

When to Use It

- You have idle cash earning nothing

- You'd happily own the stock at the strike price

- You want to generate income while "waiting" to buy

Why It Works

A cash-secured put is like a limit order that pays you to wait. Instead of paying to own a stock, the market pays you to be willing to own it.

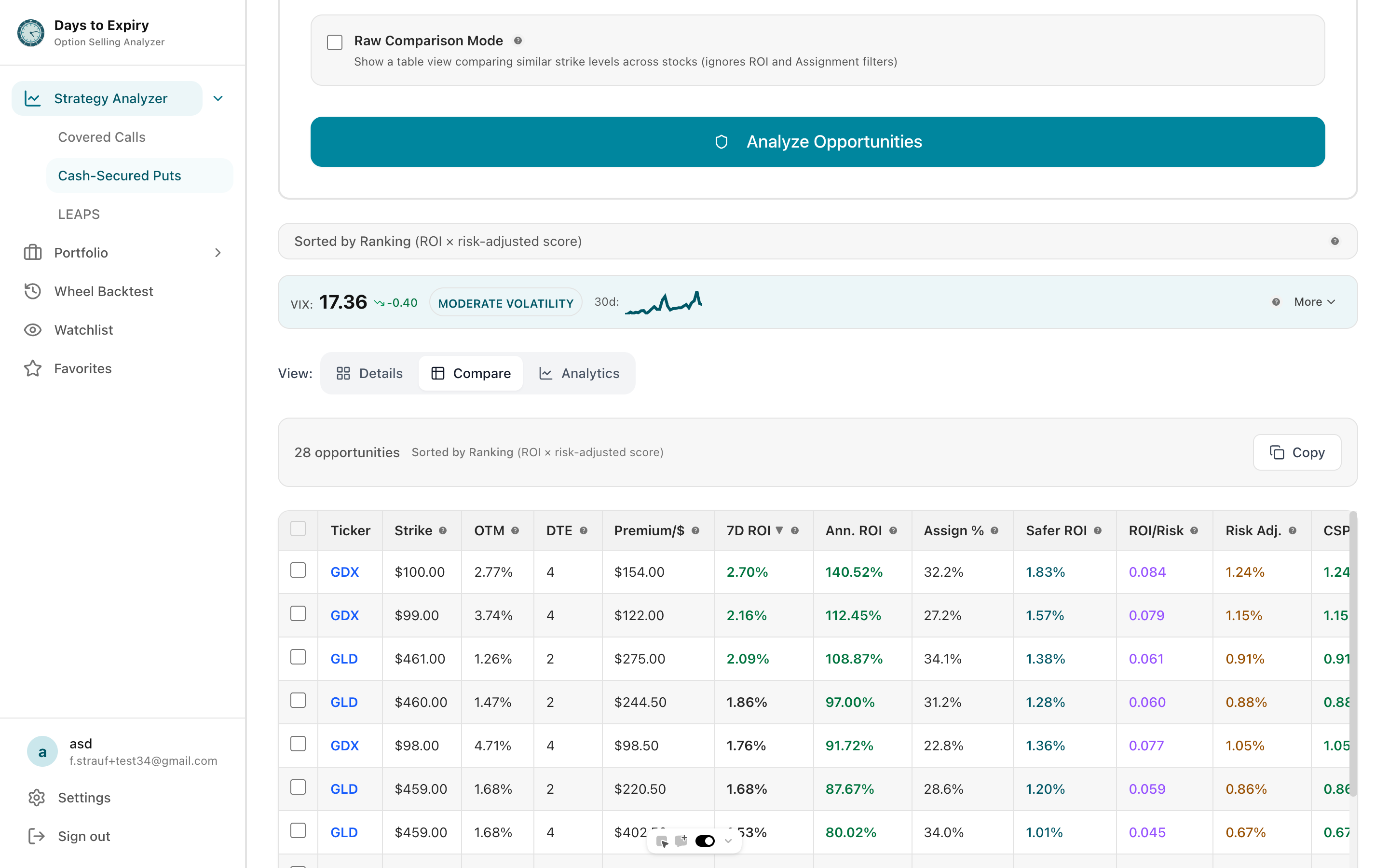

Compare premiums to find the best balance between yield and assignment risk

Compare premiums to find the best balance between yield and assignment risk

Learn more: View in Strategy Analyzer

CSP vs T-Bills: Income Comparison

See how much extra you could earn with cash-secured puts vs "safe" alternatives

Comprehensive guide: Cash-Secured Puts Playbook: DTE Optimization & Assignment Risk

Comparison with covered calls: Cash-Secured Puts vs Covered Calls: Income & Risk Comparison

Income-focused guide: Selling Puts for Income: Beginner's Complete Guide

Risk management: Options Risk Management: Position Sizing & Loss Controls

Strategy 3: Put Credit Spreads – Risk-Defined Income

What It Is

You sell a put and buy a put further out of the money. This caps your risk and reduces the margin requirement.

The math:

- Sell 50-strike put for $2 = collect $200

- Buy 48-strike put for $0.50 = pay $50

- Net credit: $150

- Max loss: $200 (the width of the spread) minus the credit = $50

When to Use It

- You want defined risk (no surprise margin calls)

- You don't have enough capital for cash-secured puts

- You're okay with a lower max profit in exchange for lower risk

Detailed guide: Put Credit Spreads: Risk-Defined Income Strategy

Strategy 4: Call Credit Spreads – Bearish Income

What It Is

The inverse of a put spread. You sell a call and buy a call further out of the money to cap risk.

Why it matters: If you think a stock is overheated or unlikely to rally, you can generate income by betting against a rally—with capped downside.

Guide: Call Credit Spreads: Bearish Income with Defined Risk

Strategy 5: Iron Condor – The Neutral-Market Cash Machine

What It Is

Combine a put spread and a call spread on the same stock at the same expiration. You're betting the stock stays in a range.

The payoff: Iron condors generate income from multiple strikes simultaneously—you collect premium on both the upside and downside.

When to use: When implied volatility is elevated (meaning premiums are fat) and you expect a calm expiration week.

Mechanics in practice: You simultaneously sell an out-of-the-money call spread and an out-of-the-money put spread on the same underlying with the same expiration. Maximum profit occurs if the stock closes between the two sold strikes at expiration. Target strikes where the probability of touch is low, use 30–45 DTE to balance theta decay against gamma risk, and close profitable positions at 25–50% of maximum profit rather than holding to expiration.

Deep dive: Iron Condor Strategy: Profit from Range-Bound Markets

Spread framework: Vertical Spread Options: Bullish & Bearish Strategy Guide

Short strangle alternative: Short Strangle Strategy: DTE-Optimized Income from Neutral Markets

Strategy 6: Short Strangle – Wide-Range Income

What It Is

Sell both an out-of-the-money call and an out-of-the-money put. You're betting the stock stays between the two strikes.

Advantage: Wider range than a strangle (the gap between strikes) means more room for the stock to move before you're threatened.

Disadvantage: Wider range also means larger potential loss if both sides are breached.

Guide: Short Strangle Strategy: DTE-Optimized Income from Neutral Markets

Strategy 7: The Wheel Strategy – The Complete Cycle

What It Is

A repeating cycle of three steps:

- Sell cash-secured puts

- If assigned, own the shares

- Sell covered calls against those shares

- Repeat

Why it's powerful: You generate income coming and going. Premium from puts, then premium from calls. Over time, this compounds into serious cash flow.

The 3-Month Wheel Cycle

The wheel works best when viewed as a repeating cycle rather than a series of isolated trades. Phase one: sell cash-secured puts on a stock you'd be happy to own, collecting premium while you wait. If assigned, phase two begins: sell covered calls against the shares, collecting premium again while you wait for a call-away at a higher price. Month 1 is put selling, Month 2 is covered calls on assigned shares, Month 3 is back to cash with the cycle restarting. This rhythm removes emotion from decision-making and keeps income flowing whether you are in cash, stock, or both. Traders who treat the wheel as a continuous system—not a series of one-off trades—tend to achieve smoother, more predictable returns. It works best on stable, liquid underlyings with strong fundamentals and weekly option availability.

Complete guide: The Wheel Strategy: Complete DTE-Optimized Guide

Best stocks for the wheel: Best Stocks for the Wheel Strategy: 2025 Screening Guide

PMCC alternative: Poor Man's Covered Call: Capital-Efficient Income Strategy

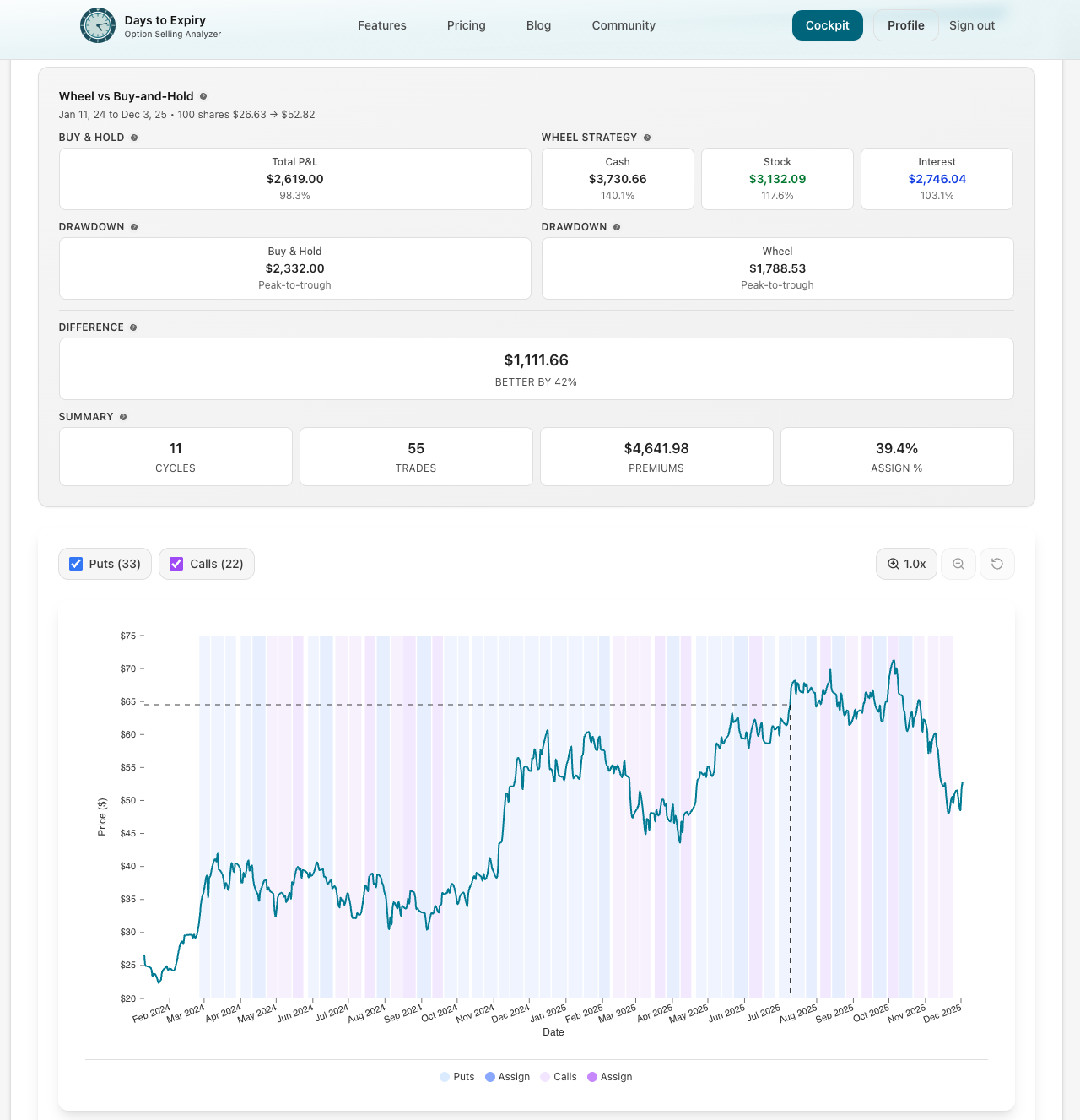

Backtesting a whole wheel to fine tune parameters for market conditions

Backtesting a whole wheel to fine tune parameters for market conditions

Learn more: View in Strategy Analyzer

Wheel Strategy Income Planner

Project your income over time with the wheel strategy (selling puts + calls)

Iron Condor vs Wheel: When to Choose Each

These two strategies anchor many income portfolios, but they solve different problems. Iron condors are delta-neutral, defined-risk trades that profit when a stock stays inside a range; the wheel is a stock-ownership system that combines premium income with long-term equity growth.

Risk profile: Iron condors carry a defined maximum loss set by the spread width. The wheel carries assignment risk—you may own the stock if it drops below your put strike—but you can keep selling covered calls against the position.

Capital requirements: Iron condors need less buying power because you're trading vertical spreads. The wheel requires enough cash to cover put assignment or 100 shares for covered calls.

Profit potential: Iron condors offer smaller, more frequent wins with strictly capped upside. The wheel generates larger premiums per cycle plus potential capital gains while you own the shares.

Real-world example: A trader with a $50,000 account might allocate $10,000 to an iron condor on SPY (collecting $150–$200 per month with defined risk) and $15,000–$20,000 to a wheel position on a stable dividend stock like Coca-Cola (KO), generating $200–$300 per month from premiums plus quarterly dividends.

Market condition cheat sheet:

- Low volatility (VIX < 15): Iron condors shine; premiums are lower but ranges hold.

- Moderate volatility (VIX 15–25): The wheel and covered calls capture elevated premiums with manageable risk.

- High volatility (VIX > 25): Cash-secured puts and short strangles collect massive premium, but cut position size in half to account for wider moves.

The most successful income traders don't marry one strategy—they rotate between them as market conditions shift and deploy capital where the edge is strongest.

Strategy 8: Poor Man's Covered Call – Capital Efficiency

What It Is

Instead of owning 100 shares (expensive), buy one long call (LEAPS) and sell shorter-dated calls against it. Same income, fraction of the capital.

The tradeoff: You're paying for the long call's theta decay, which eats into profits. But you're freeing up capital for other trades.

Comparison: PMCC vs Traditional Covered Calls: Capital Efficiency Comparison

Best stocks for LEAPS: Best Stocks for Poor Man's Covered Call: 2025 LEAPS Screening Guide

The Critical Success Factor: Days to Expiry (DTE) Optimization

Every selling strategy performs differently depending on when you enter and exit relative to expiration. This is where consistent, outsized income comes from.

Short DTE (1-7 days)

- Theta decay: Accelerates dramatically

- Income per day: Highest

- Management: Requires active monitoring

- Best for: Traders with time and discipline

Medium DTE (14-21 days)

- Theta decay: Steady and predictable

- Income per day: Moderate

- Management: Weekly check-ins

- Best for: Most traders (sweet spot of risk/reward/effort)

Long DTE (30+ days)

- Theta decay: Slower, but you hold longer

- Income per day: Lower, but consistent

- Management: Set and forget

- Best for: Passive portfolio enhancement

Reference: Options Greeks by DTE: Delta, Gamma, Theta Behavior Across Expiration Phases

Advanced timing: When to Sell Options: Timing Signals & Entry Rules by Strategy

Rolling techniques: Rolling Covered Calls: Extend Positions & Boost Income

Cash-Secured Put Income Optimizer

Compare income from selling puts at different expiration timeframes

Fetching SPY price...

Understanding the Greeks: Your Risk Dashboard

When you sell options, these metrics tell you exactly what you're betting on:

Delta: How much the option price changes for every $1 move in the stock.

- Delta 0.30 = 30% probability of expiring in-the-money

- Sell deltas around 0.20–0.40 for a good risk/reward balance

Theta (time decay): How much money you make per day just sitting.

- This is your profit engine. Higher theta = faster income.

Gamma: How fast delta changes if the stock moves.

- If you've sold short DTE options, gamma increases near expiration—watch out for violent moves

Vega: Sensitivity to implied volatility.

- High IV = fatter premiums (sell in rallies/panics)

- Low IV = thin premiums (wait or accept lower income)

Practical reference: Options Greeks Explained: Income Trader's Guide

Cheat sheet: Options Greeks Cheat Sheet: DTE-Specific Reference Guide

Assignment preparation: Options Assignment Probability: Calculator & Decision Framework

Portfolio Income Layering: Multi-Strategy Approach

The professionals don't rely on one strategy. They layer:

- Covered calls on quality dividend stocks

- Cash-secured puts on 30% of cash reserves

- Iron condors on stocks in established trading ranges

- The wheel on secondary holdings

By combining strategies, you maintain consistent income even when market conditions shift. The key is correlation: you want your income sources to respond differently to the same market event. If volatility spikes, your iron condors may struggle, but your cash-secured puts collect fatter premiums. If the market trends strongly upward, your wheel positions benefit from capital appreciation while your covered calls still generate premium. A well-layered portfolio smooths returns and reduces the emotional stress of relying on a single tactic.

Practical allocation example for a $50,000 account:

- 40% ($20,000) in wheel positions on 2–3 stable dividend stocks

- 30% ($15,000) in covered calls on existing long-term holdings

- 20% ($10,000) in iron condors on broad index ETFs

- 10% ($5,000) in cash-secured puts as dry powder for market dips

This mix ensures that no single strategy dominates your P&L, and you always have capital ready to deploy when opportunity arises. Allocate capital by strategy based on your current market outlook, and avoid over-concentration in any one underlying or direction.

Deep dive: Portfolio Income Layering: Covered Calls + Dividends + Cash-Secured Puts

Dividend synergy: Selling Covered Calls on Dividend Stocks: Double-Income Strategy

Tax efficiency: SPX Options Tax Treatment: The 60/40 Rule Explained

Risk Management: The Non-Negotiable Rules

Rule 1: Never Sell Naked Calls

An uncovered (naked) call has unlimited risk. If the stock gaps up 50%, your losses are unlimited. Always have a hedge (own shares, own a higher call, or use a spread).

Rule 2: Position Size Ruthlessly

A single bad assignment shouldn't materially impact your portfolio. Treat each trade as 1-2% of your capital.

Rule 3: Understand Assignment Risk

When you sell an option in-the-money, you can be assigned early (especially puts on dividend dates, calls on earnings).

Assignment guide: Options Assignment Probability: Calculator & Decision Framework

Prevention guide: Early Assignment in Options: Risk Management & Prevention

Position sizing: Options Risk Management: Position Sizing & Loss Controls

Assignment mechanics and execution process showing decision pathways

Assignment mechanics and execution process showing decision pathways

Learn more: View in Strategy Analyzer

Rule 4: Monitor Greeks Weekly

Delta, theta, gamma, and vega change as the stock and market move. A "safe" position can become dangerous if you ignore the Greeks.

Risk framework: Options Risk Management: Position Sizing & Loss Controls

Assignment Stress Test

Test your position under adverse market scenarios to understand assignment risk and potential losses.

Base Assignment Probability

30%

Premium Collected

$250

Maximum Loss

$43,750

Scenario Analysis

| Price Move | Final Price | Assignment Prob | P/L | Status |

|---|---|---|---|---|

| Current | $450.00 | 15% | $250 | Safe |

| -5% | $427.50 | 32.9% | $-1,000 | At Risk |

| -10% | $405.00 | 38.6% | $-3,250 | At Risk |

| -20% | $360.00 | 52.2% | $-7,750 | At Risk |

Break-even: $437.50 • Blue row shows current price scenario

Find real options with similar parameters

Broker Selection: Tools Matter

Not all brokers are equal for options selling. You need:

- Multiple strike/DTE options: SPX, SPY, individual stocks

- Low commissions: $0/trade or minimal per-contract fees

- Greeks display: Delta, theta, gamma on every option

- Flexible rolling: Easy to close and re-open positions

- Margin clarity: Exact margin requirements per strategy

Broker comparison: Best Brokers for Options Trading: 2025 Comparison Guide

Tax considerations: Covered Call Tax Rules: Everything You Need to Know

Tax Considerations: Plan Ahead

Selling options generates short-term capital gains (taxed as ordinary income) unless you use special strategies like SPX options (Section 1256 contracts, taxed 60/40 long/short-term).

Tax rules: Covered Call Tax Rules: Everything You Need to Know

Advanced tax strategy: SPX Options Tax Treatment: The 60/40 Rule Explained

Wash sale alert: Wash Sale Rules for Options Traders: The Complete Guide

Income system: Selling Options Strategy: How to Build a Systematic Income Portfolio

Putting It Together: Your First Week

Day 1-2: Choose your strategy (start with covered calls or cash-secured puts)

Day 3: Select a stock/strike with DTE between 14-21 (sweet spot for beginners)

Day 4: Sell the option, collect the premium

Day 5-10: Let theta decay work. Check Greeks mid-week.

Day 11-14: Decide: close for profit, roll to extend, or let assignment happen

Day 15+: Repeat with the next position

Match the Strategy to Your Account Size

You don't need a six-figure account to sell options, but the strategies available to you depend heavily on account size and experience:

- Under $5,000: Focus on defined-risk strategies with minimal buying power—cash-secured puts on lower-priced stocks ($20–$50/share) and put credit spreads. Paper trade covered calls while you build capital, and stick to one or two positions at a time.

- $5,000 to $25,000: Covered calls become viable once you own 100 shares, and the wheel opens up on mid-priced names. Add put credit spreads for defined-risk income.

- $25,000 to $50,000: Layer in iron condors, short strangles, and the wheel across multiple positions.

- $50,000+: Run a full portfolio income approach—wheel positions on core holdings, iron condors on index ETFs, dividend capture with covered calls—managed at the portfolio level rather than trade by trade.

Capital efficiency tip: Portfolio margin can reduce buying-power requirements by 50–70% compared to Reg-T margin, but it amplifies drawdowns if you over-leverage. A conservative rule is to use no more than 50% of available portfolio margin at any time, leaving a buffer for volatility expansion.

The key is matching strategy complexity to your capital and experience. A trader with $5,000 who tries to run iron condors on SPX will likely face margin calls and forced exits. Start where you are, not where you want to be.

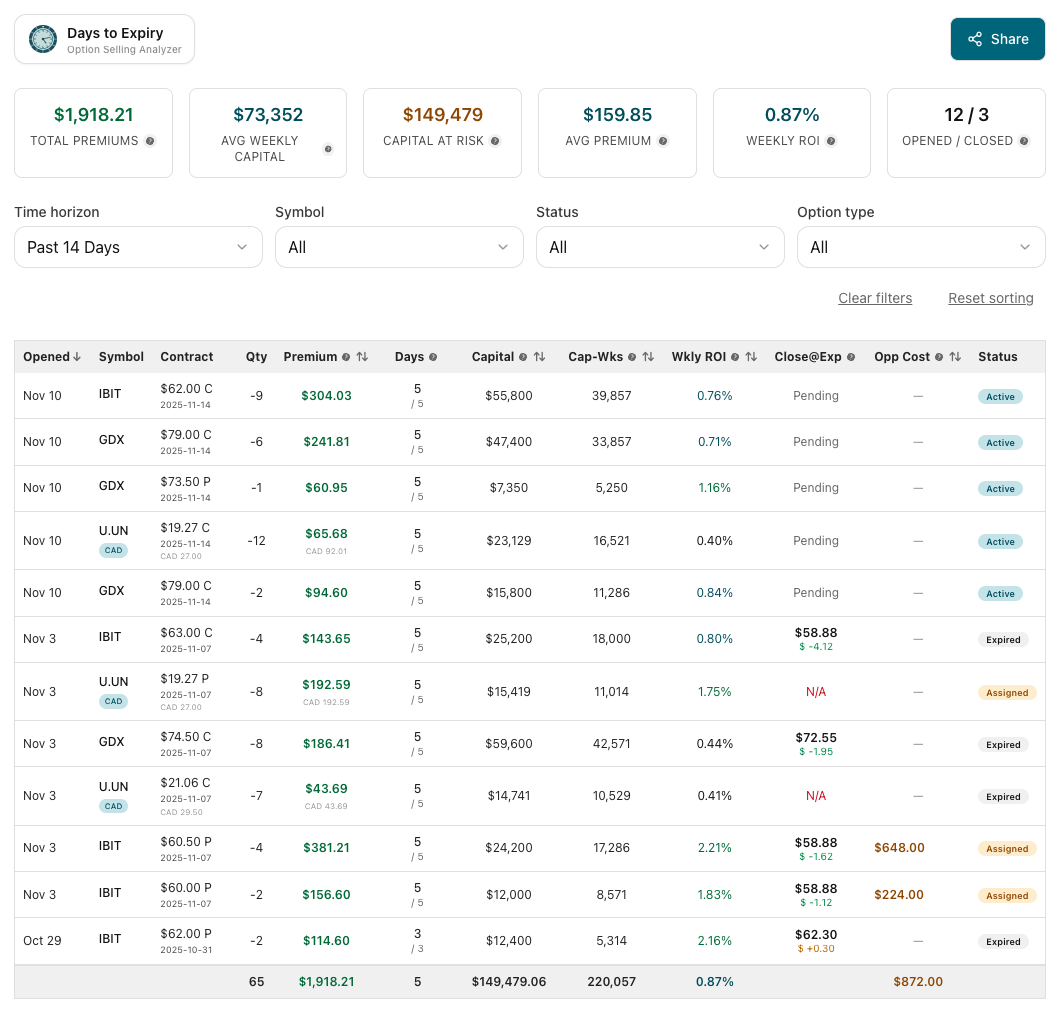

How a Layered Income Portfolio Pays Each Month

Premium collected across calls, puts, and spreads by month — the cash-flow view of the multi-strategy approach above.

Income Calendar

opening credits and buybacks by month

Connect your broker and see your own income calendar — every credit and buyback, month by month.

The Bottom Line

Selling options for income isn't passive—it requires discipline, risk management, and a methodical approach. But for traders willing to put in the work, it's one of the most consistent paths to portfolio income.

Start small (one or two positions), master one strategy, then layer in others. The Greeks are your friends—learn them. DTE optimization is where the real money is—respect it. And never, ever ignore risk management.

Your future income depends on decisions you make today.

Continue Learning

Ready to dive deeper? Start with your chosen strategy:

- Covered calls? Selling Covered Calls for Income: Step-by-Step Strategy

- Cash-secured puts? Selling Puts for Income: Beginner's Complete Guide

- Spreads? Vertical Spread Options: Bullish & Bearish Strategy Guide

Or explore advanced income strategies: Portfolio Income Layering: Covered Calls + Dividends + Cash-Secured Puts

Related Articles

**Core I

- Wheel Options Trading Strategy

- Options Trading for Dummiesncome Strategies:**

- Cash-Secured Puts Playbook: DTE Optimization & Assignment Risk - Detailed CSP strategy guide

- Covered Calls by Expiration: Weekly vs Monthly Income Comparison - DTE-optimized covered calls

- Poor Man's Covered Call: Capital-Efficient Income Strategy - Capital-efficient covered call variant

- The Wheel Strategy: Complete DTE-Optimized Guide - Multi-strategy income combination

Spread Strategies:

- Put Credit Spreads: Risk-Defined Income Strategy - Risk-defined bullish income

- Call Credit Spreads: Bearish Income with Defined Risk - Risk-defined bearish income

- Vertical Spread Options: Bullish & Bearish Strategy Guide - Complete spread framework

- Iron Condor Strategy: Profit from Range-Bound Markets - Advanced neutral strategy

Risk Management & Foundations:

- Options Greeks Explained: Income Trader's Guide - Master theta, delta, and gamma

- Options Risk Management: Position Sizing & Loss Controls - Proper sizing and risk limits

- Early Assignment in Options: Risk Management & Prevention - Managing assignment scenarios

- Implied Volatility & Days to Expiry: Timing Your Options Entries - Entry optimization for income trades

Advanced Strategies:

- Portfolio Income Layering: Covered Calls + Dividends + Cash-Secured Puts - Combining multiple income sources

- Rolling Covered Calls: Extend Positions & Boost Income - Extending positions for continuous income

- Synthetic Covered Call Strategy: Capital-Efficient Income with LEAPS

- Selling Options Strategy: How to Build a Systematic Income Portfolio

DTE & Timing:

- When to Sell Options: Timing Signals & Entry Rules by Strategy - Entry optimization for every income strategy

- Options Greeks Cheat Sheet: DTE-Specific Reference Guide - Quick-reference for delta, theta, gamma, and vega

- Greeks by DTE Reference: How Delta, Gamma, Theta & Vega Change Over Time - Deep dive into Greek behavior across expiration cycles

Expertise: This guide is written by a CMT charterholder with 12+ years of options market-making experience, reviewed by a CFA charterholder for accuracy, and based on backtested options data, live trade logs, and interviews with professional income traders managing six-figure portfolios.

Ready to start generating consistent options income? Download our free Options Income Strategy Selector to match your capital and risk tolerance to the right approach.

Frequently Asked Questions

Written by Days to Expiry Trading Team

The Days to Expiry trading team brings together experienced options traders and financial analysts dedicated to helping investors generate consistent income through proven options strategies.

Apply The Strategy