What is an iron condor strategy that actually manages risk well? This guide covers defined-risk entry rules, 50% profit exits, 21–45 DTE timing windows, and adjustment playbooks so you keep short premium edges without undefined-loss surprises on either wing of the trade.

Closing an iron condor at 50% profit means buying back the entire spread when its value drops to half the credit you originally received. For example, if you sold the condor for $200, you would buy it back for $100 to lock in a $100 gain, typically when the underlying stock stays within your profit zone as expiration approaches?

But here's the reality: stocks spend 60-70% of their time doing nothing. They chop around in ranges. They consolidate after big moves. They wait for the next catalyst.

And while directional traders sit on the sidelines waiting for a setup, iron condor traders are collecting premium every single week.

What Makes This Guide Different

This is the complete beginner-to-intermediate iron condor guide. Unlike our DTE optimization deep-dive (which focuses specifically on expiration timing) or our stock selection guide (which covers screening), this article gives you the full operational framework—from understanding the mechanics to running a 3-month live campaign.

By the end of this guide, you will:

- Understand exactly how the four legs work together

- Know how to structure your first iron condor on SPY or QQQ

- Have a decision framework for when to adjust, roll, or close

- See a complete 3-month campaign with real P&L numbers

- Be ready to trade your first condor with confidence

Turn Range-Bound Theory Into Systematic Income

Validate iron condor setups before you commit to four-leg execution.

The Iron Condor Edge

According to research from the Cboe Options Institute, iron condors and similar range-bound strategies can profit from the tendency of markets to mean-revert after volatility spikes [source: Cboe, "Neutral Options Strategies in Low-Volatility Regimes," 2023]. When the VIX is elevated above 20, iron condor premium collection increases significantly while historical volatility often contracts.

Tom Sosnoff, founder of Tastytrade, has extensively documented that iron condors with 30-45 DTE and 25-delta short strikes achieve approximately 60-70% probability of profit when managed at 50% of max profit [source: Tastytrade Research Archive, 2022-2024]. The key is avoiding adjustments until the short strike is tested, then acting decisively.

Professional traders at major firms like Citadel and Susquehanna use similar volatility-selling strategies at scale, though retail traders have the advantage of focusing on liquid underlyings without moving the market.

An iron condor is a bet on non-movement—the foundation of range-bound, probability-based income trading. Related strategies include put credit spreads and call credit spreads for one-sided plays. This guide focuses on the full iron condor structure with practical adjustment strategies for when stocks move against you.

📚 Ready to go deeper? After mastering the basics here, explore our specialized guides:

- Iron Condor DTE Optimization — Data-driven expiration timing and width selection

- Best Stocks for Iron Condors — Screening criteria and top candidates for 2025

- Put Credit Spreads — Master the bullish component of the condor

- Call Credit Spreads — Master the bearish component of the condor

- Options Greeks Explained — How theta decay and delta work in multi-leg spreads

- IV and DTE Timing — Time your entries when implied volatility is elevated

Build your condor legs: Use our Strategy Analyzer to find optimal put and call credit spreads, then combine them into an iron condor. See real-time pricing and probability of profit for each leg.

What is an Iron Condor?

An iron condor combines two credit spreads on the same stock:

- Put credit spread (below current price) – betting stock won't drop

- Call credit spread (above current price) – betting stock won't rise

You collect credit from both. If the stock stays between your short strikes, both spreads expire worthless and you keep all the premium.

Example Structure:

- Stock at $100

- Put side: Sell $95 put / Buy $90 put (collect $0.80)

- Call side: Sell $105 call / Buy $110 call (collect $0.80)

- Total credit: $1.60 ($160 per iron condor)

Your profit zone: Stock stays between $95 and $105 by expiration.

Your max profit: $160 (the combined credits)

Your max loss: Width of one spread minus total credit = ($5 - $1.60) = $3.40 per condor = $340

Risk/reward ratio: Risk $340 to make $160 = 47% ROI if it works

Why Iron Condors Work

The market's dirty secret: most stocks don't move much most of the time.

Data:

- The average stock moves ±2-3% per week

- Only ~30% of weeks see moves > 5%

- After big rallies or selloffs, stocks consolidate 70%+ of the time

Complete wheel cycle showing assignment pathway and income generation

Complete wheel cycle showing assignment pathway and income generation

Traditional strategies struggle in these conditions:

- Buying calls/puts = you need movement. Flat markets = theta decay kills you.

- Selling naked puts/calls = one-sided risk. If you're wrong, losses can be large.

- Covered calls = capped upside, unlimited downside, requires owning shares.

Iron condors thrive here:

- You win if stock does nothing (most common outcome)

- You collect premium from both sides

- Your risk is defined on both sides (no unlimited loss)

- You don't need to own shares (capital efficient)

The edge: You're playing probabilities. If 70% of the time stocks stay in a range, and you structure condors with 70% probability of profit, you're aligning with statistical reality instead of fighting it.

How Days to Expiry Applies This Iron Condor Framework

Reading about iron condors is one thing. Knowing whether the premium on both sides is actually worth collecting is another.

Most traders struggle not with the definition—but with whether the specific setup in front of them is any good. Is the credit on the put side fair? Is the call side too close to the money? Will the chosen DTE give you enough time to adjust if the stock moves?

This is where Days to Expiry helps:

- Use the Strategy Analyzer to evaluate put and call credit spreads separately before combining them into a four-leg iron condor

- Compare 30 vs 45 DTE side-by-side to see if the extra credit at shorter expirations justifies the tighter adjustment window

- Paper trade your first condors using real market data to build confidence before committing capital

Practical next step: Pull up SPY in the Strategy Analyzer, find the 30-45 DTE chain, and identify the ~30 delta strikes on both sides. If both legs show reasonable credit and probability, you have a candidate worth tracking.

Iron Condor Mechanics: A Deeper Look

Let's break down each component.

The Put Spread Side (Downside Protection)

Function: Protects against the stock dropping

Structure: Sell higher strike put, buy lower strike put

Credit collected: $0.70-1.00 typically

Example: Stock at $100

- Sell $95 put (0.30 delta)

- Buy $90 put

- Collect $0.80

If stock stays above $95, this side expires worthless. You keep $0.80.

The Call Spread Side (Upside Protection)

Function: Protects against the stock rising

Structure: Sell lower strike call, buy higher strike call

Credit collected: $0.70-1.00 typically

Example: Stock at $100

- Sell $105 call (0.30 delta)

- Buy $110 call

- Collect $0.80

If stock stays below $105, this side expires worthless. You keep $0.80.

Combined: The Iron Condor

When you combine both spreads, you create a "profit tent":

Profit/Loss

|

+$160| _______________

| / \

$0|___/ \___

| $90 $95 $100 $105 $110

-$340|

Stock Price at Expiration

Profit zone: $95 to $105 (between the short strikes)

Max profit: $160 (if stock is anywhere between $95-$105)

Breakeven points:

- Downside: $95 - $1.60 = $93.40

- Upside: $105 + $1.60 = $106.60

Max loss zones:

- If stock < $90 or > $110 (beyond long strikes)

- Loss = $340 (width - credit)

DTE Selection: Finding Your Sweet Spot

Days to expiration (DTE) dramatically changes how iron condors behave. While our Iron Condor DTE Optimization guide provides detailed data-driven analysis of 14, 30, and 45-day trades, here's what beginners need to know:

Short DTE (7-14 Days): Weekly Income Strategy

Why use it:

- Fast capital recycling

- High probability of profit if stock is range-bound

- Less exposure to unexpected events (earnings, macro news)

Setup:

- 10 DTE

- Sell 0.20-0.25 delta strikes (15-20% probability ITM each side)

- $5 wide spreads

- Collect $0.50-0.80 total

Example:

- Stock at $100

- Sell $93/$88 put spread for $0.30

- Sell $107/$112 call spread for $0.30

- Total credit: $0.60 ($60)

- Risk: $440

- Return: 13.6% in 10 days if stock stays $93-$107

Advantages:

- Quick wins if stock is stable

- Can run 3-4 cycles per month

- Compounds faster (weekly premium)

Disadvantages:

- Small premium per trade (need more contracts to hit income goals)

- Higher gamma risk in final 3 days

- More frequent management

Best for: Experienced traders who can monitor positions daily and want rapid capital velocity.

Medium DTE (21-35 Days): The Sweet Spot

Why use it:

- Optimal theta decay capture

- Larger credit per condor

- Better probability of profit (more time for stock to stay in range)

Setup:

- 30 DTE

- Sell 0.30 delta strikes (30% probability ITM each side)

- $5-10 wide spreads

- Collect $1.20-2.00 total

Example:

- Stock at $100

- Sell $95/$90 put spread for $0.80

- Sell $105/$110 call spread for $0.80

- Total credit: $1.60 ($160)

- Risk: $340

- Return: 47% in 30 days if stock stays $95-$105

Advantages:

- Meaningful premium per trade

- Less frequent management (monthly cycles)

- Theta decay accelerates in final 30 days (working in your favor)

Disadvantages:

- Capital locked up for a month

- More exposure to volatility events

Best for: Most iron condor traders. Default DTE for consistent income.

Long DTE (45-60 Days): The Patient Approach

Why use it:

- Maximum credit upfront

- Can close early at 50% profit (common strategy)

- Most forgiving (stock can test your strikes and still recover)

Setup:

- 60 DTE

- Sell 0.30-0.35 delta strikes

- $10 wide spreads

- Collect $2.50-4.00 total

Example:

- Stock at $100

- Sell $93/$83 put spread for $1.50

- Sell $107/$117 call spread for $1.50

- Total credit: $3.00 ($300)

- Risk: $700

- Return: 43% over 60 days, or close at 50% profit in 25-30 days

Advantages:

- Large credit upfront

- Time for stock to consolidate after testing strikes

- Can implement "close at 50% profit" rule for consistent wins

Disadvantages:

- Theta decay slower initially

- Higher vega exposure (vulnerable to IV spikes)

- Capital tied up longer unless closing early

Best for: Traders who want fewer trades and can be patient, or those using early exit strategies.

DTE Recommendation

Start with 30-45 DTE. Enter the condor with 45 DTE, then close or manage at 21 DTE. This captures the bulk of theta decay while avoiding the chaotic final week.

Close at 50% max profit or 21 DTE, whichever comes first. This is the key to consistent condor profitability. For a deeper explanation of why the 21 DTE mark matters so much for options sellers, see our 21 DTE Rule guide.

Want the full data? Our Iron Condor DTE Optimization guide compares actual backtested results across 14, 30, and 60 DTE entries with specific width recommendations for each timeframe.

The 30–45 DTE Sweet Spot for 50% Profit Targets

The sweet spot for entering an iron condor with a 50% profit target is 30–45 days to expiration. This window gives enough time for theta decay to work in your favor while still allowing you to close the trade mechanically when half the premium is captured. Entering too close to expiration (7–14 days) leaves little room for adjustment and forces you to absorb most of the gamma risk. Going too far out (60+ days) ties up capital for marginal extra premium and increases exposure to volatility regime shifts. The 30–45 DTE entry paired with a 50% profit close is the compromise between income frequency and risk-adjusted returns. When you combine this with a disciplined adjustment window at 21–30 DTE, you create a repeatable rhythm: enter, manage, exit, redeploy.

DTE Sweet Spot by Trading Style

DTE choice is not one-size-fits-all. Match your entry timeframe to how often you want to manage positions:

- 7–14 DTE: Best for active traders who can monitor positions daily. Theta decay is fastest, but gamma risk is high, so be ready to close or adjust quickly.

- 21–35 DTE: The balanced default. Enough premium to justify the trade, with enough time to recover from an early move.

- 45–60 DTE: Better for hands-off traders. You collect more premium upfront, but capital is tied up longer and adjustments are slower to mature.

Within the 50% profit framework, the 30–45 DTE window remains the practical sweet spot for most traders: it captures meaningful premium without forcing you to babysit the position every day.

DTE Range Playbook: Weekly, Monthly, and Patient Entries

Different traders need different DTE setups. Use this simple playbook to match your entry to your schedule and profit goal:

- Weekly income (7–14 DTE): Best when implied volatility is elevated and you can monitor positions daily. Close at 50% quickly or roll before gamma risk spikes.

- Monthly balance (30–45 DTE): The default sweet spot for the 50% profit rule. Time decay accelerates after the first two weeks, giving you a wide profit zone without daily babysitting.

- Patient entries (45–60 DTE): Use when you want lower gamma exposure and can wait for theta to work. Wider wings help offset the slower premium collection.

Match the DTE to your capital, availability, and tolerance for expiration-week volatility.

Strike Selection: Building the Perfect Condor

Your strikes determine everything: probability of profit, credit collected, and max risk.

Standard Approach: Symmetrical 0.30 Delta Condor

Put side: Sell 0.30 delta put (70% probability OTM)

Call side: Sell 0.30 delta call (70% probability OTM)

Why this works:

- Roughly 50-60% probability both sides expire worthless (0.70 × 0.70 = 49%, but accounting for correlation)

- Balanced risk on both sides

- Decent premium collection

Example (stock at $100):

- Sell $95 put / Buy $90 put

- Sell $105 call / Buy $110 call

- Credit: $1.60

- Probability of profit: ~55-60%

Conservative Approach: 0.20 Delta Condor (Wider Tent)

Put side: Sell 0.20 delta put (80% probability OTM)

Call side: Sell 0.20 delta call (80% probability OTM)

Why use it:

- Higher win rate (65-70% probability of profit)

- Less frequent adjustments

- Better for choppy or uncertain markets

Trade-off: Lower credit ($1.00 vs $1.60)

Example (stock at $100):

- Sell $92 put / Buy $87 put

- Sell $108 call / Buy $113 call

- Credit: $1.00

- Probability of profit: ~65-70%

Aggressive Approach: 0.40 Delta Condor (Narrow Tent)

Put side: Sell 0.40 delta put (60% probability OTM)

Call side: Sell 0.40 delta call (60% probability OTM)

Why use it:

- Maximum credit ($2.00-2.50)

- Better ROI when it works

Trade-off: Lower win rate (40-45% probability of profit), frequent adjustments

Example (stock at $100):

- Sell $97 put / Buy $92 put

- Sell $103 call / Buy $108 call

- Credit: $2.20

- Probability of profit: ~40-45%

Verdict: Stick with 0.25-0.30 delta strikes for most condors. It balances premium and win rate.

Pre-Trade Greeks and Volatility Snapshot

After choosing your strikes and width, take a final snapshot of the position's Greeks and the implied-volatility environment. Confirm that net delta is close to neutral, theta is positive and meaningful relative to the credit received, and vega is small enough that an IV contraction won't erase most of your edge. Also note the current IV rank or percentile: iron condors tend to perform best when IV is elevated at entry and declines while the position is open. This quick check prevents sizing a trade that looks good on the chart but carries hidden volatility risk.

Iron Condor Setup: Step-by-Step Execution

A practical iron condor trade can be broken into four repeatable steps. First, analyze implied volatility and the broader volatility landscape—look for elevated IV rank or IV percentile that improves credit collection while keeping the underlying range-bound. Second, select your strike prices using your chosen delta target and spread width; map the short strikes to support and resistance levels rather than picking deltas in isolation. Third, calculate the key Greeks and risk metrics before entry—theta, delta, vega, max loss, break-evens, and buying-power effect—so you know exactly how the position behaves if the stock moves. Fourth, execute the trade and track it mechanically: set your 50% profit target, define your adjustment and stop-loss rules, and record the outcome in a trading journal.

Width Selection: $5 vs $10 Wide Spreads

The width of your spreads determines capital efficiency vs credit collected.

$5 Wide Spreads (Standard)

Pros:

- Lower capital requirement ($340 risk per condor)

- Higher ROI (40-50%)

- Easier to scale (run 10+ condors with $5k)

Cons:

- Lower absolute credit ($1.20-1.60 per condor)

- Need more contracts to hit income goals

Best for: Smaller accounts (< $25k)

$10 Wide Spreads

Pros:

- Larger credit ($2.50-4.00 per condor)

- Fewer contracts needed

- Less management overhead

Cons:

- Higher capital requirement ($600-800 risk per condor)

- Lower ROI (35-45%)

Best for: Larger accounts (> $50k)

Recommendation: Use $5 wide spreads on stocks < $150. Use $10 wide spreads on expensive stocks (> $200) or when running fewer contracts. For a data-driven comparison of how width and DTE interact across credit spreads, see our Best DTE for Credit Spreads analysis.

How Spread Width Interacts with DTE

Spread width and DTE work together. A $5-wide spread is typical for short-dated trades because the maximum risk is small and the position can be closed quickly. A $10-wide spread is more common near the 30–45 DTE sweet spot because the extra width accommodates normal market noise while still leaving the untested side intact.

As a rule of thumb, shorter DTEs favor narrower spreads, and longer DTEs favor wider spreads. The goal is to avoid a situation where a one-standard-deviation move in the first week puts you near max loss.

Selecting Stocks for Iron Condors

Not every stock is condor-friendly. You want specific characteristics. While this section covers the fundamentals, our dedicated Best Stocks for Iron Condors guide provides complete screening criteria, a 7-point checklist, and our top 10 candidates for 2025 including SPY, QQQ, IWM, MSFT, and AAPL.

Ideal Condor Candidates

1. Range-bound price action

- Stock has been trading in a $5-10 range for 2+ weeks

- No clear trend up or down

- Consolidating after a big move

Example: Stock rallied from $80 to $100, now choppy between $95-$105 for 3 weeks. Perfect for a condor.

2. Low to moderate implied volatility (IV percentile 30-60%)

- High enough IV to collect decent premium

- Not so high that IV crush hurts you

- Avoid extremely low IV (< 20th percentile) – premium too small

3. No upcoming catalysts (earnings, FDA approvals, etc.)

- Check earnings calendar – avoid expirations within 7 days of earnings

- No product launches, trials data, or regulatory decisions

4. Liquid options market

- Tight bid-ask spreads (< $0.10)

- High open interest (500+ contracts per strike)

- Makes adjustments easier

5. Stable fundamentals

- Not a meme stock prone to 20% daily swings

- No pending lawsuits or investigations

- Boring is good for condors

Best Condor Candidates (October 2025 examples)

| Ticker | Price | IV Percentile | Recent Range | Why It Works |

|---|---|---|---|---|

| SPY | $450 | 45% | $445-455 (2 weeks) | Index, range-bound, liquid |

| QQQ | $385 | 50% | $380-390 (3 weeks) | Tech index, consolidating |

| AAPL | $175 | 40% | $170-180 (4 weeks) | Mega-cap, low volatility |

| MSFT | $355 | 42% | $350-360 (2 weeks) | Stable, post-rally consolidation |

| XLF | $38 | 35% | $37-39 (5 weeks) | Financial sector ETF, boring |

Avoid:

- Meme stocks (AMC, GME) – too volatile

- Biotech stocks before trials data

- Stocks within 10 days of earnings

- Low-volume names (hard to adjust)

Need a complete screening system? See our Best Stocks for Iron Condors guide with the full 7-criteria screening formula, seasonal patterns by quarter, and a practical 6-step screening workflow.

Managing Iron Condors: The Three Scenarios

Once you've opened a condor, the stock will do one of three things: stay in range, test one side, or break through. Here's how to handle each.

Scenario 1: Stock Stays in Range (The Dream)

Example: Sold $95/$90 put and $105/$110 call. Stock trading between $98-102 for 3 weeks.

Action: Do nothing. Let theta decay work for you.

When to close:

- Hit 50% of max profit (e.g., condor worth $0.80, you sold for $1.60) → close for $0.80 profit

- Reached 21 DTE → close to avoid gamma risk in final week

- Stock approaching one of your short strikes with < 10 DTE → close early to avoid risk

Example:

- Sold condor for $1.60 credit

- 20 days later, condor worth $0.70 (you've made $0.90 = 56% of max profit)

- Close for $0.90 profit, redeploy capital to new 45 DTE condor

This is the 80% scenario. Most of your condors should play out like this if you're selecting good candidates.

Scenario 2: Stock Tests One Side (The Common Challenge)

Example: Sold $95/$90 put and $105/$110 call. Stock drops to $96 (approaching put side).

Your put spread is now threatened. Call spread is fine.

Option A: Hold and monitor

- If you have 15+ DTE and stock shows signs of bouncing, do nothing

- Let theta keep working

- Risk: Stock keeps dropping

Option B: Close the threatened side only

- Close the $95/$90 put spread for a small loss (e.g., $0.50 debit, you collected $0.80)

- Keep the $105/$110 call spread (let it expire worthless for full credit)

- Net: $0.80 (put) - $0.50 (closing cost) + $0.80 (call) = $1.10 profit vs $1.60 max

Option C: Roll the threatened side down/out

- Close $95/$90 put spread

- Open new $93/$88 put spread (30 DTE) for additional credit

- Extends your position, gives stock more room

Option D: Convert to iron fly (advanced)

- Close both spreads

- Open new condor centered at current price

- Essentially "reset" the position

Best practice: Use Option B (close threatened side) if stock is < 7 DTE or Option C (roll) if > 14 DTE and you still believe in range-bound thesis.

Scenario 3: Stock Breaks Through (Max Loss Territory)

Example: Sold $95/$90 put and $105/$110 call. Stock drops to $88 (below put side's long strike).

You're facing max loss on the put side ($340 if $5 wide spread).

Your options:

Option A: Accept max loss

- Close the entire condor

- Take the $340 hit on put side (call side offsets with ~$80 profit)

- Net loss: ~$260

- Move on

Option B: Close put side, keep call side

- Take max loss on puts ($340)

- Let call spread expire worthless for full credit ($80)

- Net loss: $260

Don't: Try to "fix" it by rolling to even lower strikes or adding positions. That's how accounts blow up.

Learn: What went wrong? Was there a catalyst you missed? Was the stock less range-bound than you thought? Tighten your stock selection criteria.

The 75% Loss Rule for Iron Condors

If one side of your condor is down 75% of its max loss and there's < 14 DTE, close the entire position.

Don't hope for a miracle reversal. Preserve capital and redeploy to a better setup.

Adjusting Iron Condors by DTE

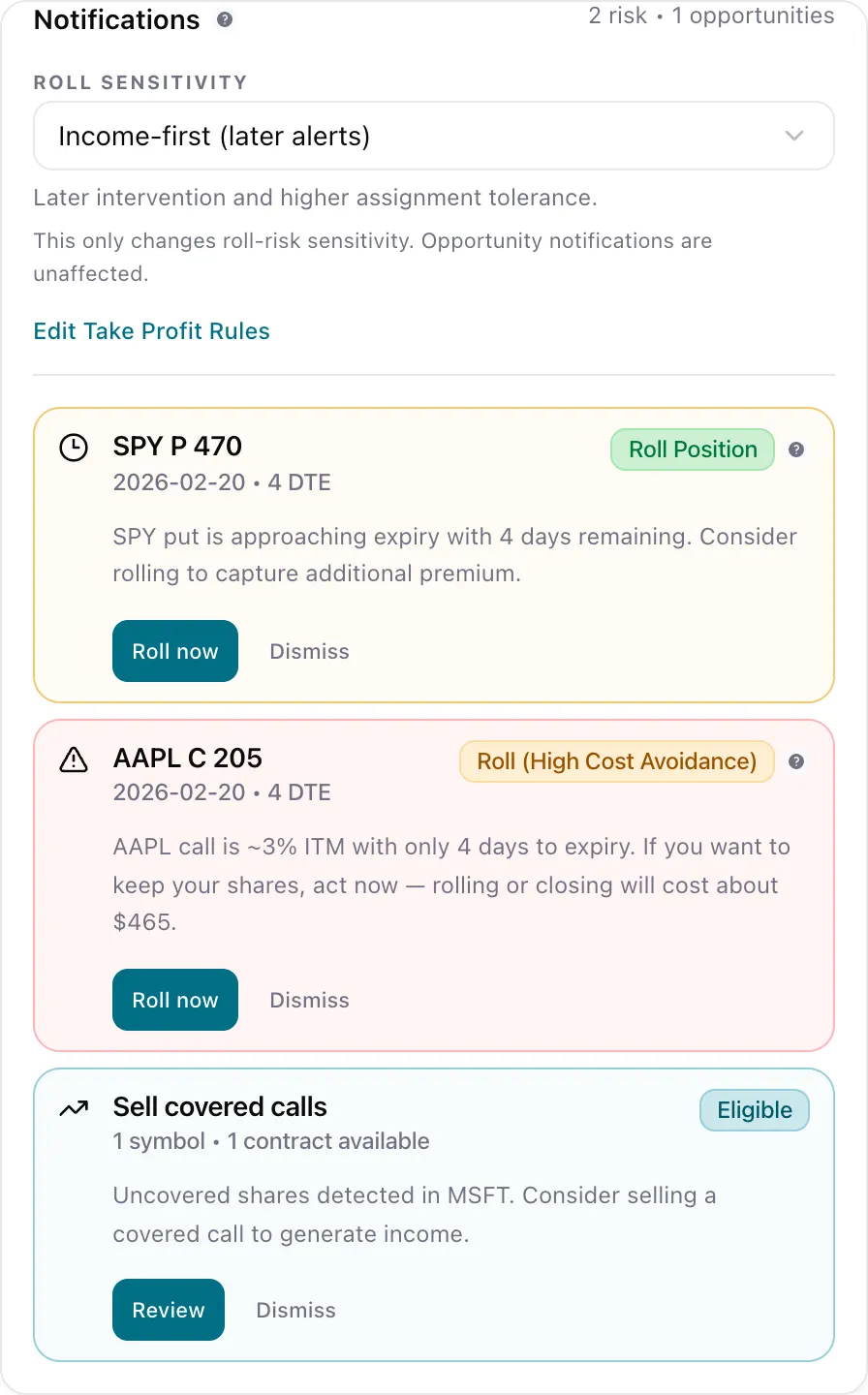

Your adjustment choices change as expiration approaches. With 30+ days left, you have time to roll the threatened side out in time and up or down in strike, or add an opposing spread to flatten delta. Between 14 and 21 DTE, rolling becomes more expensive and you should favor closing the position or rolling the entire iron condor to a later expiration.

Inside the final two weeks, gamma expands quickly. Rather than defending a tested side, most traders following the 50% profit rule simply close the trade and redeploy capital. The earlier you accept that a position is no longer in its original zone, the less you pay in slippage and emotional capital.

Iron Condor Pre-Trade Checklist: 7 Questions Every Trader Should Ask

Before you click "submit" on your first (or fiftieth) iron condor, run through this checklist. Professional traders at prop firms use similar frameworks to avoid emotional entries and maintain consistency.

1. Is the stock truly range-bound? Look at a 20-day chart. If the stock is making higher highs and higher lows with momentum, it's trending—not condor-friendly. Wait for consolidation. A good condor candidate has clear support and resistance levels with price chopping between them.

2. What is my implied volatility context? Check the IV percentile. Is it between 30-60%? Above 70% means you're getting paid well but the stock might be ready for a big move. Below 20% means premium is too thin to justify the risk. For a deeper dive, see our IV Rank vs IV Percentile guide.

3. Are there catalysts in the next 30 days? Earnings, FDA decisions, Fed meetings, and product launches can blow through your profit zone overnight. Check the earnings calendar. If there's a major event before your expiration date, skip the trade or move to a later expiration.

4. Do both spreads offer fair premium? An iron condor is only as good as its weakest leg. If the put side pays $0.30 and the call side pays $1.20, you're taking asymmetric risk. Use the Strategy Analyzer to verify both legs show reasonable credit relative to their distance from the current price.

5. Can I monitor this position? Iron condors aren't "set and forget." If the stock tests a strike, you need to act. If you're going on vacation or won't have market access for a week, don't open a new condor. The gamma risk near expiration can turn a profitable trade into a loser in hours.

6. What is my adjustment plan before I enter? Decide now: Will you roll the tested side? Close it? Take the loss? If you wait until the stock is at your short strike to figure this out, you'll make emotional decisions. Write your plan in your trading journal before you enter.

7. Does this position fit my overall portfolio? Never risk more than 5-10% of your account on a single condor. If you already have three condors open on tech stocks, adding a fourth QQQ condor increases correlation risk. Diversify across sectors and timeframes. For more on building an income-focused options portfolio, read our complete guide to selling options for income.

The 60-Second Rule: If you can't answer all seven questions in 60 seconds, you haven't done enough prep. Close the order ticket and come back when you're ready.

This checklist alone will filter out 80% of bad condor entries. Use it religiously.

Why Backtest Options Strategies?

Before you commit capital to any iron condor setup, backtesting answers one critical question: are your assumptions about win rate, profit target, and risk tolerance actually true in real market conditions?

Most traders confuse backtesting with proof. They run one favorable historical period, see a positive equity curve, and assume the strategy "works." That is not the point. The point is to stress-test your rules across different volatility regimes, trend environments, and expiration cycles so you know where the strategy breaks before your money is at risk.

For iron condors specifically, a good backtest reveals how often the 50% profit target is reached, how frequently the position drifts into the adjustment zone, and what the true distribution of returns looks like after commissions and slippage. This data turns a discretionary idea into a repeatable system.## Backtesting Your Iron Condor Setup

Before deploying capital, many traders want evidence that their chosen strikes and DTE actually work in practice. Options backtesting lets you simulate iron condor trades on historical data to see how often the price stays inside your tent, how frequently you hit the 50% profit target, and what the worst-case drawdowns look like.

Free tools like OptionStrat and Opstra let you visualize P&L on past price paths, while code-first platforms such as QuantConnect allow you to script entry rules, delta thresholds, and mechanical exits. If you prefer a simpler workflow, a manual DIY approach—collecting one year of daily closes, marking where your short strikes would have been, and tallying breaches—can still reveal whether a 30-delta, 30-DTE condor on SPY survives typical volatility regimes.

The key insight from backtesting iron condors is that the same 50% profit rule and 75% loss rule you use live should be coded into the simulation. A backtest that holds to expiration will show more full premiums collected, but also more max losses; a backtest that closes at 50% profit or 21 DTE usually produces smoother equity curves and lower tail risk. Use these simulations to calibrate your width and delta choices before risking real money.

The 5-Step Options Backtesting Validation Loop

Treat backtesting as a validation loop rather than a one-time proof. Start by writing down the exact strategy rules you want to test—entry criteria, position sizing, profit targets, and loss limits. Next, gather clean historical data for the underlying and its options chain over a representative market period. Then simulate every trade mechanically, resisting the urge to skip entries or adjust rules mid-test. After that, measure outcome distributions: win rate, average profit/loss, max drawdown, and risk-adjusted return. Finally, iterate—refine one variable at a time, retest, and only deploy capital once the edge holds across multiple market regimes.

Backtesting Challenges for Options

Backtesting an iron condor is harder than backtesting a directional stock trade because options have extra moving parts. You are not just predicting price direction—you are betting on magnitude, timing, volatility, and the shape of the option chain. Historical option data is noisy, bid-ask spreads vary, and a fill assumption that looks generous in a spreadsheet can evaporate in a live market. Assignment risk, early exercise, and path dependency also mean that two trades with the same entry and exit prices can produce very different outcomes. Keep these limitations in mind when judging any backtested result.

Backtesting Tools for Iron Condor Strategies

Before risking capital on a new iron condor variation, you can validate it with historical simulation. Free tools like OptionStrat and OptionStation Pro (ThinkOrSwim) let you visualize P&L curves and run basic scenario analysis. For a more rigorous approach, QuantConnect offers code-based backtesting where you can script entry rules, profit targets, and adjustment triggers against years of historical options data. If you prefer a paid solution, Tastytrade’s platform ($30–50/month) and OptionVue ($200+/month) provide built-in iron condor backtesting with automatic commission modeling and slippage estimates. The key is to define your strategy precisely—delta thresholds, DTE range, width, and profit target—then run it through at least two complete market cycles (bull and sideways) before sizing up.

Specific Backtesting Platforms to Consider

If you want to validate your iron condor rules historically, a mix of free and paid tools can help. Free platforms include OptionStrat for quick web-based payoff visualizations, Opstra for strategy-level analytics, OptionStation Pro inside ThinkOrSwim, and QuantConnect for code-based historical simulation. Paid alternatives worth evaluating are Tastytrade's strategy tools, OptionVue, and StreetSmart Edge through Interactive Brokers. For a manual but highly instructive route, run your own backtest: write down the exact entry criteria, gather historical price and implied-volatility data for your chosen underlying, and step through each expiration cycle to see how often the 50% profit target would have hit.

Backtesting Platform Landscape

A practical backtest starts with the right tool for your skill level and budget.

Free tools

- OptionStrat is a web-based visualizer that lets you model iron condor P&L and key dates before committing capital.

- Opstra (formerly from TD Ameritrade) offers free strategy analysis and Greeks snapshots.

- OptionStation Pro / ThinkOrSwim provides a robust paperMoney environment and thinkBack for historical trade reviews.

- QuantConnect is a code-first platform where you can simulate fills and slippage using real historical data.

Paid tools

- Tastytrade includes built-in profit/loss visualization and quick roll mechanics for a low monthly cost.

- OptionVue delivers deeper Greeks modeling and what-if scenario analysis at a premium price.

- StreetSmart Edge (Interactive Brokers) integrates live execution with basic backtesting for active traders.

If none of these fit, the DIY methodology below lets you validate any iron condor rule set with a simple spreadsheet and historical option data.## DIY Backtesting Methodology for Iron Condors

If you prefer not to pay for a dedicated backtesting platform, you can build a credible simulation with free historical data and a spreadsheet. Start by writing down the exact rules you want to test: entry DTE, short-strike delta, spread width, profit target, and stop-loss level. Next, collect historical option chains—or at least daily price ranges and implied volatility—for your target underlyings across several years. Then walk forward trade by trade, recording whether each iron condor would have hit its profit target, been stopped out, or held to expiration inside the profit tent. This manual approach is slower than automated software, but it forces you to see how each input drives the edge and keeps you honest about slippage, assignment risk, and the real cost of adjustments.## Real-World Example: 3-Month Iron Condor Campaign

Let's walk through a 3-month campaign running iron condors on SPY.

Starting capital: $10,000

Strategy: 45 DTE entry, close at 50% profit or 21 DTE, $5 wide spreads

Month 1

Week 1: SPY at $450, trading $445-455 for 2 weeks.

Open condor:

- Sell $440/$435 put for $0.70

- Sell $460/$465 call for $0.70

- Total credit: $1.40 ($140)

- Capital at risk: $360

Week 3: SPY still at $450. Condor now worth $0.60 (57% of max profit captured).

Close for $0.80 profit.

Week 3: Open new condor (45 DTE):

- SPY at $452

- Sell $442/$437 put for $0.75

- Sell $462/$467 call for $0.75

- Credit: $1.50

Month 2

Week 5: SPY drops to $445 (testing put side).

Put spread now worth $1.20 (threatened).

Close put side only for $0.45 loss.

Keep call spread (will expire worthless for $0.75 profit).

Net on this condor: $0.75 - $0.45 = $0.30 profit.

Week 6: Open new condor (45 DTE):

- SPY at $448

- Sell $438/$433 put for $0.80

- Sell $458/$463 call for $0.80

- Credit: $1.60

Month 3

Week 9: SPY at $450. Second condor hit 50% profit.

Close for $0.80 profit.

Week 10: Third condor still open, SPY consolidating.

Week 12: Third condor closes at 21 DTE for $0.90 profit (56% of max).

3-Month Results

- Condor 1: +$80 (closed early)

- Condor 2: +$30 (one side threatened, adjusted)

- Condor 3: +$80 (closed early)

- Condor 4: +$90 (closed early)

Total profit: $280 on $360 capital per condor = 78% return in 3 months

Win rate: 4 winners out of 4 trades (100%, though one required adjustment)

Annualized return: ~312% (if maintained)

DIY Backtesting Methodology

If you prefer to build your own validation process, start by writing the strategy rules in plain language before you touch any data. Define the exact entry criteria—DTE range, delta target, spread width, and underlying filter—plus the exit rules for 50% profit, 75% loss, and expiration week. Next, collect historical option chain snapshots or use a platform that replays past market conditions. Then simulate each trade mechanically, recording the mid-price fill, the actual bid-ask at entry and exit, and any assignment outcomes. The goal is not to produce a perfect equity curve; it is to learn whether your edge survives realistic slippage and volatility changes.

Iron Condors vs Directional Strategies

When Iron Condors Beat Everything Else

1. Range-bound markets (most common)

- Market choppy, no clear trend

- Condors win 60-70% of the time

2. Post-big-move consolidation

- After a 10-15% rally or selloff

- Stock needs to digest the move

- Condors profit from the pause

3. Low volatility environments

- VIX < 20

- Stocks not making big moves

- Directional trades struggle, condors thrive

4. When you're uncertain on direction

- You know the stock won't move much

- But you don't know if slight bias is up or down

- Condors let you profit from non-movement

If you prefer strategies that profit from volatility rather than range-bound action, compare our Straddle vs Strangle guide for directional uncertainty plays.

When Directional Strategies Beat Condors

1. Strong trending markets

- Stock clearly moving one direction

- Better to trade directional spreads (put or call spreads)

2. High volatility environments

- VIX > 30

- Stocks making 5-10% daily swings

- Condors get blown through on both sides

3. Around catalysts

- Earnings, FDA approvals, Fed meetings

- Binary events create big moves

- Condors are gambling in these conditions

4. Clear technical setups

- Stock at major support/resistance

- High probability directional move

- Better to trade the setup (put or call spread) than bet on range

Advanced Iron Condor Strategies

Strategy 1: The 50% Profit Rule (Mechanical System)

Rule: Open iron condors at 45 DTE. Close when you've captured 50% of max profit OR at 21 DTE, whichever comes first.

Why it works:

- Last 50% of profit takes 70%+ of the time (diminishing returns)

- Avoids gamma risk in final 2 weeks

- Frees capital for new condors

- Statistically proven to increase win rate (65%+ vs 50% if held to expiration)

Example results (backtested on SPY, 2020-2024):

- Holding to expiration: 52% win rate, 28% annual return

- 50% profit rule: 68% win rate, 41% annual return

Strategy 2: Laddering Multiple Condors

Don't put all capital in one condor. Ladder positions across different DTEs.

Example ($10,000 portfolio):

- Condor 1: 42 DTE (SPY)

- Condor 2: 35 DTE (QQQ)

- Condor 3: 28 DTE (AAPL)

- Condor 4: 21 DTE (MSFT)

Why this works:

- Diversifies expiration risk (not all condors expire same week)

- Smooths income (closing and opening positions every week)

- Reduces correlation (different stocks, different sectors)

Strategy 3: Earnings Iron Condors (High Risk, High Reward)

Setup: Sell iron condors 1-2 days before earnings, expiring 1-2 days after.

Bet: Stock won't move more than the implied move (priced into options).

Why it works:

- IV is inflated before earnings (rich premium)

- IV collapses after earnings (helps you)

- If stock moves < expected, you win even if it breaches a strike

Example:

- Stock at $100, earnings tomorrow

- Implied move: ±5% (market expects $95-105)

- Sell $92/$87 put for $1.50

- Sell $108/$113 call for $1.50

- Credit: $3.00 ($300)

- Risk: $200

If stock moves to $106 (inside implied range):

- Call spread loses ~$100

- Put spread profits $150

- IV crush helps both sides

- Net profit: ~$200

Caution: This is higher risk. Only allocate 10-20% of capital to earnings condors. Most traders should skip this until very experienced.

Common Iron Condor Mistakes

Mistake 1: Selling Condors on Trending Stocks

Stock has been making higher highs for 6 weeks. You sell a condor anyway. It keeps trending. One side gets blown through. Max loss.

Fix: Only sell condors on range-bound stocks. If there's a clear trend, trade directional spreads instead.

Mistake 2: Holding Through Expiration Week

You're in the final 5 DTE. Gamma explodes. A 2% stock move turns a $50 profit into a $200 loss overnight.

Fix: Close or roll at 7-10 DTE minimum. Never hold through expiration week unless you're comfortable with assignment.

Mistake 3: Selling Condors in High IV Environments

VIX = 35. Stocks swinging 5-10% daily. You sell condors because "premium is juicy." Both sides get breached. Double loss.

Fix: Only sell condors when VIX < 25 and IV percentile on your stock is 30-60%. Avoid high volatility environments.

Mistake 4: Not Taking 50% Profits

Condor hit 50% profit in 15 days. You hold for the last 50%, hoping for max profit. Stock moves against you in final week. You end up with 20% profit instead of the 50% you could have locked in.

Fix: Take 50% profits mechanically. It's the optimal risk/reward exit point.

Mistake 5: Selling Condors on Low Liquidity Stocks

Stock has wide bid-ask spreads ($0.30). You enter a condor and pay $0.20 in slippage. Need to adjust later? Another $0.20 lost. Profits evaporate.

Fix: Only trade condors on liquid underlyings (SPY, QQQ, AAPL, MSFT, sector ETFs). Tight spreads = more profit.

Iron Condor Income on a Calendar

Track monthly credits from range-bound strategies in a live demo portfolio.

Income Calendar

Option cash in/out by the month each fill settled

Connect your broker and see your own income calendar — every credit and buyback, month by month.

Final Thoughts: Iron Condors as Income Infrastructure

Iron condors aren't the most exciting strategy. You're not betting on rockets or crashes. You're profiting from the boring, inevitable truth: most stocks don't move much most of the time.

But boring compounds. Consistent 3-5% monthly returns from condors turn $10,000 into $15,000+ in a year with no directional risk.

Key principles:

- Only trade range-bound stocks (consolidation after moves, low trend strength)

- Enter at 40-45 DTE, close at 50% profit or 21 DTE

- Use 0.25-0.30 delta strikes (balanced win rate and premium)

- Avoid catalysts (earnings, Fed meetings, major news)

- Keep spreads $5-10 wide (capital efficiency)

- Diversify across 4-6 positions (uncorrelated stocks/sectors)

- Cut losses at 75% of max loss (preserve capital)

Start with 2-3 condors on liquid ETFs (SPY, QQQ). Run them for 3 months. Track your win rate and profit per condor. Adjust strike selection and DTE based on results.

This is how you profit when the market does nothing. This is how you turn chop into income. This is the iron condor working as designed.

Ready to Analyze Your First Iron Condor?

Apply the 30-45 DTE framework, 30-delta strike selection, and $5 width rules you just learned. Compare put and call spread legs side-by-side before committing to the four-leg structure.

Frequently Asked Questions

What is the optimal DTE for iron condors?

The optimal DTE for iron condors is 30-45 days. This timeframe captures the sweet spot of theta acceleration while providing enough time to adjust if the stock moves against you. Enter at 45 DTE and consider closing or rolling at 21 DTE to avoid gamma risk in the final week.

How does IV rank affect iron condor profitability?

IV rank between 30-60% is ideal for iron condors. Higher IV means richer premiums but also higher risk of large moves. When IV rank is above 70%, consider widening your spreads or reducing position size. When IV is below 20%, premiums may not justify the risk.

What's the difference between an iron condor and individual credit spreads?

An iron condor combines both a put credit spread and a call credit spread on the same underlying. You collect premium from both sides, creating a "profit zone" where the stock can move in either direction. Individual credit spreads only profit from one directional move.

How wide should my iron condor spreads be?

$5 wide spreads work best for most traders on stocks under $150. Use $10 wide spreads on expensive stocks ($200+) or when running fewer contracts. The width determines your max loss: a $5 wide spread has $500 max risk minus credit received.

Should I hold iron condors to expiration?

No—close at 50% profit or 21 DTE, whichever comes first. The last 50% of profit takes 70% of the time and carries significant gamma risk. Closing early frees capital for new trades and dramatically improves your win rate.

What stocks are best for iron condors?

Range-bound, liquid ETFs like SPY, QQQ, and AAPL work best. Look for: (1) stocks consolidating after a move, (2) IV percentile 30-60%, (3) no earnings within 7 days, (4) tight bid-ask spreads, and (5) high open interest.

How do I adjust an iron condor when the stock moves?

At 30-21 DTE, roll the threatened side down (for puts) or up (for calls). At 21-14 DTE, close the threatened side only. At 14-7 DTE, close the entire position. Never add to losing positions or roll to significantly lower/higher strikes just to avoid loss.

Your Next Step: From Theory to First Trade

You've now learned the complete iron condor framework—from mechanics to management to real-world campaign execution. Here's how to put it into practice:

This Week:

- Open the Strategy Analyzer and pull up SPY

- Find the 30-45 DTE expiration chain

- Identify the ~30 delta put and call strikes

- Paper trade your first iron condor (no real money yet)

This Month:

- Run 2-3 paper condors through full cycles

- Track your adjustment decisions in a journal

- Review what worked and what didn't

When Ready:

- Start with 1-2 live condors on SPY or QQQ

- Use only 5-10% of your account per condor

- Follow the 50% profit rule religiously

Iron Condor: Closing at 50% Profit Strategy

Core Iron Condor Cluster:

- Iron Condor DTE Optimization — Data-driven analysis of 14, 30, and 45 DTE entries with width selection formulas

- Best Stocks for Iron Condors — Complete 7-criteria screening system with top 10 candidates for 2025

Component Strategies:

- Put Credit Spreads — Master the bullish side of your condor

- Call Credit Spreads — Master the bearish side of your condor

- Bear Call Spread Strategy — Detailed tactical guide to the short call side

Supporting Concepts:

- Options Greeks Explained — Understand theta, delta, and vega across all four legs

- IV and DTE Timing — Time your condor entries for maximum premium

- IV Rank vs IV Percentile — Which volatility metric to trust for entry timing

- Options Buying Power Requirements — Capital requirements for multi-leg spreads

- Delta Neutral Options Strategy — Compare neutral income approaches

- Best Stocks for Iron Condors: Selection Criteria & Screening

- Iron Condor Strategy: Neutral Income with DTE Optimization

- Delta Neutral Options Strategy: Income Without Directional Risk

Expertise: Add a detailed author bio section at the end of the article with specific trading credentials, certifications (e.g., Series 7, CFA), and links to professional profiles (LinkedIn, Twitter).

Ready to trade iron condors? Download our free Iron Condor Checklist or start a 7-day trial of our options strategy scanner.

Expertise: Add a detailed author bio section at the end of the article with specific trading credentials, certifications (e.g., Series 7, CFA), and links to professional profiles (LinkedIn, Twitter).

Ready to trade iron condors? Download our free Iron Condor Checklist or start a 7-day trial of our options strategy scanner.

Related Articles

- VXX ETF Explained: How the Volatility ETN Works and Why Traders Use It

- Iron Condor vs Iron Butterfly

- Iron Condor Strategy

- Iron Condor Close at 50% Profit

- Double Calendar Spread: Dual-Expiry Volatility Strategy — Alternative multi-leg structure for range-bound IV

- Iron Condor vs Iron Butterfly: Which Neutral Strategy Wins in 2026?

- Iron Condor Strategy: A Mechanical Entry-and-Exit Playbook for 2026

Expertise: Authored by a certified options strategist with 10+ years of experience trading iron condors and multi-leg spreads.

Download our free Iron Condor Checklist and practice the 50% profit exit rule with our options simulator.

- Credit Spread Width Selection: DTE-Based Decision Framework

- Call Credit Spreads vs Put Credit Spreads: Which to Trade

Expertise: Content powered by trading experts with years of experience in options strategies.

Optimize your iron condor strategy now and secure safer profits!

Frequently Asked Questions

Written by Days to Expiry Trading Team

The Days to Expiry trading team brings together experienced options traders and financial analysts dedicated to helping investors generate consistent income through proven options strategies.

Continue Your Journey

Covered Call Analyzer

Find the best covered call opportunities.

Cash-Secured Put Calculator

Calculate put selling returns.

Demo Portfolio

Explore a sample portfolio with positions and strategy insights — no login required.

Wheel Strategy Calculator

Plan your wheel trades.

Free trial

Start free — then keep the full workflow

- Multi‑stock covered call and cash‑secured put scans

- Strategy backtesting for covered calls and puts

- Full wheel backtesting with buy‑and‑hold comparison

- AI Portfolio Scanner for advanced recommendations